After discussing

Public Provident fund (PPF) in detail on Tuesday December 19, 2017, today we will extensively talk about EPF – Employees Provident Fund.

What is the Employee Provident Fund (EPF)?

An employee provident fund is created through the contributions made by an employee and employer. Under EPF scheme, both the employee and the employer has to make certain contributions every month towards the EPF scheme. You as an employee will get this money at the time of your retirement or if you discontinue working either temporarily or permanently due to any kind of disability.

The EPF is a tax-free investment instrument for the salaried class having an Exempt-Exempt-Exempt Status. The contributions made by the employee is eligible for tax deductions under Section 80C, the interest earned on the total investments and the withdrawal (including partial withdrawals for specific expenses) are exempt from the purview of taxation.

These contributions are made every month, thereby encouraging employees to save a portion of their salary each month. Investments made by a vast number of employees across India are pooled together and invested by a trust.

The EPF is created by the Employees Provident Fund Organization (EPFO) of India, a statutory body of the Indian Government under the Labour and Employment Ministry.

It states that an organization (irrespective of its structure) having 20 or more permanent employees (across different departments and branches whether located in the same location or otherwise), working in any of 180 plus industries, should mandatorily register with the EPFO.

What is interesting to note here is, the Act defines an “employee” as “any person who is employed for wages in any kind of work, manual or otherwise, in or in connection with the work of an establishment and who gets his wages directly or indirectly from the employer, and includes any person employed by or through a contractor in or in connection with the work of the establishment and engaged as an apprentice, not being an apprentice engaged under the Apprentices Act, 1961 (52 of 1961) or under the standing orders of the establishment”

Where does my monthly EPF contribution go into?

Currently, the following three schemes are in operation under the EPF Act of 1952, and it is into these trusts that your monthly contributions go:

- Employees’ Provident Fund Scheme (EPF) (1952)

- Employees’ Deposit Linked Insurance Scheme (EDLI) (1976)

- Employees’ Pension Scheme (EPS) (1995)

EPF, EPS and EDLIS are calculated on the basis of your Basic + Dearness Allowance (DA) (including cash value of any food concession allowed to the employee) + Retaining Allowance (RA) if any. (Retaining Allowance means allowance payable for the time being to an employee of any factory or other establishment during any period in which the establishment is not working, for retaining his services.)

What is the Employees’ Pension Scheme (EPS)?

The Employees’ Pension Scheme, 1995 (EPS 1995) came into effect from 16th November 1995. It has been designed as a “Benefit Defined Social Insurance Scheme” formulated following “actuarial principles” for ensuring long term financial viability.

The scheme aims at providing economic sustenance during old age and survivorship coverage to the member and his/her family. The EPS 1995 is funded by diversion of 8.33% of monthly wages (subject to the wage ceiling which is presently Rs 15,000/- per month) from the employers’ share of contribution. The Central Government also contributes 1.16% of monthly wages.

This part of your monthly contribution is targeted towards offering pension on:

- Member Pension upon retirement /superannuation

- Member Pension upon disablement while in service

- Withdrawal Benefit upon leaving service after putting in less than 10 years but more than six months of service

- Spouse Pension upon death of member

- Spouse Pension upon death of member as pensioner

- Children Pension along with spouse pension (up to age 25) for two children at a time

- Orphan Pension upon death or remarriage of spouse (up to age 25)

- Disabled Child Pension to children/orphan (life-long)

- Nominee Pension to the Nominee when no family exists

- Dependent Parent Pension when no family and nominee exist

The formula for calculating member pension under EPS’95 is as follows:

What is the Employees’ Deposit Linked Insurance Scheme (EDLIS)?

EDLIS is a social security scheme with an objective to provide a helping hand to the beneficiaries of the deceased employee. Most individuals in India are ignorant on the importance of owning a life insurance policy and would prefer not to buy one if given a choice to opt out. Hence in order to maintain the economic wealth of the family (and the society) the government has introduced the EDLI scheme.

The scheme gives life cover to the employees of the organized sector. It is a group term insurance plan which gets activated on the bereavement of the employee paying a maximum sum assured of Rs 6,00,000 to the nominee. The cost of the scheme is borne by the employer.

However, most employers opt out for the EDLI and choose to have a group life insurance cover for their employees; this works out better for the employees and does not increase any cost to the employer.

What is the contribution percent of the employee and the employer?

The breakup of the contribution is different for the employee and employer.

An employee’s contribution goes directly into the EPF, while the employer’s contribution goes into the EPF, the EPS and the EDLIS.

Here is how it is broken up:

Employee:

- 12% into EPF (This comes out of the employees’ salary).

Employer:

- 3.67% into EPF

- 8.33% into EPS

- 0.5% into EDLIS

- 0.85% for EPF Administrative Charges

- 0.01% for EDLIS Administrative Charges

As you can see, you as an employee do not contribute to the life insurance premium charges. It is borne by your employer. Also, the administrative charges for both the EPF and the EDLIS are borne by the employer too While your contribution goes solely towards your EPF and your Pension.

Let’s look at some calculations so that you can understand how it works:

Consider the below two situations:

- A Basic Salary below Rs 15,000 and

- A Basic of Rs 15,000 or above.

Let’s look at a Basic Salary below Rs 15,000 first.

Employee A draws a Basic of Rs 3,500. Here’s how the contribution works out:

| EPF |

Employee Contribution |

12% of Rs 3,500 |

Rs 420 |

| EPS |

Employer Contribution |

8.33% of Rs 3,500 |

Rs292 |

| EPF |

Employer Contribution |

3.67% of Rs 3,500 |

Rs 128 |

(Note: The above table is for illustration purpose only)

(Source: PersonalFN Research)

Now let’s consider another example wherein Employee B draws a Basic of Rs 20,000. There are two ways of allocating the contribution.

Situation 1:

The employer and employee decide to contribute towards EPF based on the Basic salary of Rs 20,000, which is above the fixed limit of Rs15,000.

| EPF |

Employee Contribution |

12% of Rs20,000 |

Rs2,400 |

| EPS |

Employer Contribution |

8.33% of Rs15,000 |

Rs1,250 |

| EPF |

Employer Contribution |

Balancing Figure (2,400 – 1,250) |

Rs1,150 |

(Note: The above table is for illustration purpose only)

(Source: PersonalFN Research)

In the above example the employee contributed a higher share towards the EPF account (i.e. Rs 20,000 x 12% = Rs 2,400) but the maximum contribution by an employer towards EPS was calculated based on the maximum ceiling limit (i.e. Rs 15,000) and not Rs 20,000.

Situation 2:

The employer and employee decide to contribute towards EPF based on the Basic salary of Rs 15,000.

| EPF |

Employee Contribution |

12% of Rs15,000 |

Rs1,800 |

| EPS |

Employer Contribution |

8.33% of Rs 15,000 |

Rs 1,250 |

| EPF |

Employer Contribution |

Balancing Figure (i.e. 3.67% of Rs 15,000) (1,800 – 1,250) |

Rs550 |

(Note: The above table is for illustration purpose only)

(Source: PersonalFN Research)

Under the above calculation, the contributions to the EPF are payable on a maximum ceiling of Rs 15,000 by employee and employer. However, an employee has a liberty to contribute at a higher rate to the EPF but the same liberty cannot be called for from the employer, who will contribute his share with a maximum ceiling of Rs 15,000.

However, if both the employee and the employer want to contribute on the higher rate, then a joint request needs to be submitted by them. In which case, employer has to pay administrative charges on the higher wages (wages above 15000/-)

Historic Rate of Interests earned on EPF contributions

Historically, EPF interest rates have moved as follows:

| Year |

Rate of Interest Announced |

Increase / Decrease / Constant |

% Change |

| 1981-82 |

8.50% |

- |

- |

| 1982-83 |

8.75% |

Increase |

0.25% |

| 1983-84 |

9.15% |

Increase |

0.40% |

| 1984-85 |

9.90% |

Increase |

0.75% |

| 1985-86 |

10.15% |

Increase |

0.25% |

| 1986-87 |

11% |

Increase |

0.85% |

| 1987-88 |

11.50% |

Increase |

0.50% |

| 1988-89 |

11.80% |

Increase |

0.30% |

| 1989-90 |

12% |

Increase |

0.20% |

| 1990-91 |

12% |

Constant |

0% |

| 1991-92 |

12% |

Constant |

0% |

| 1992-93 |

12% |

Constant |

0% |

| 1993-94 |

12% |

Constant |

0% |

| 1994-95 |

12% |

Constant |

0% |

| 1995-96 |

12% |

Constant |

0% |

| 1996-97 |

12% |

Constant |

0% |

| 1997-98 |

12% |

Constant |

0% |

| 1998-99 |

12% |

Constant |

0% |

| 1999-2000 |

12% |

Constant |

0% |

| 2000-01 |

11% |

Decrease |

-1.00% |

| 2001-02 |

9.50% |

Decrease |

-1.50% |

| 2002-03 |

9.50% |

Constant |

0% |

| 2003-04 |

9.50% |

Constant |

0% |

| 2004-05 |

9.50% |

Constant |

0% |

| 2005-06 |

8.50% |

Decrease |

-1.00% |

| 2006-07 |

8.50% |

Constant |

0% |

| 2007-08 |

8.50% |

Constant |

0% |

| 2008-09 |

8.50% |

Constant |

0% |

| 2009-10 |

8.50% |

Constant |

0% |

| 2010-11 |

9.50% |

Increase |

1.00% |

| 2011-12 |

8.25% |

Decrease |

-1.25% |

| 2012-13 |

8.50% |

Increase |

0.25% |

| 2013-14 |

8.75% |

Increase |

0.25% |

| 2014-15 |

8.75% |

Constant |

0% |

| 2015-16 |

8.80% |

Increase |

0.05% |

| 2016-17 |

8.65% |

Decrease |

-0.15% |

(Note: The above table is for illustration purpose only)

(Source: PersonalFN Research)

The Central Government revises the interest rate given on the EPF, every year in the month of March/April depending upon the revenues in the EPFO made from its earlier years’ deposits. This year Labour Minister Bandaru Dattatreya announced to keep the rate constant against market expectations to increase it to 8.90%. Earlier, the Union Finance Minister, Mr. Arun Jaitley, in his Budget speech had suggested changing the Exempt-Exempt-Exempt status of EPF to EET. However, amidst the protest from the common man, the suggestion was later retracted.

Additionally, you can use PersonalFN EPF Calculator to calculate the returns on your EPF contributions.

You just need to enter the current balance of your EPF account or Pension fund account and your Employer’s contribution towards your EPF account. Further, enter an expected growth rate in your salary until your retirement, which will help you to increase EPF contribution every year.

What is the Universal Account Number (UAN)?

UAN stands for Universal Account Number, which is a unique 12-digit number for all individuals enrolled under the EPF scheme. The best part is, UAN is a unique number assigned to each employee and remains permanent even when you switch your employment.

UAN can be generated by logging in to the EPFO website. Once you have registered your UAN, you will receive details like EPF balance and other such information on your mobile phone via SMS.

(Source: EPFO Newsletter)

How can I activate my UAN with SMS service?

The members can also activate their UAN account by sending an SMS to 07738299899 from the comfort of their mobile phones which would enable them to avail all UAN related facilities. The format of the SMS is:

EPFOHO<UAN>LAN.

Here, LAN stands for the first three character of the preferred language in which the member desires to get the details.

This facility is available in ten different languages namely English, Hindi, Punjabi, Gujarati, Marathi, Kannada, Telugu, Tamil, Malayalam and Bengali. A missed call service has been launched for those members who have activated their UAN. Such members can give a missed call to 011-22901406 to fetch the details about their accounts.

How to link Aadhaar with UAN?

The Employees’ Provident Fund Organisation (EPFO) in January 2017 made it mandatory for its pensioners and subscribers to submit their Aadhaar numbers. The deadline had been revised time and again in view of the slow progress over the UID number submission by members. The new deadline is set as June 30, 2017. The important benefit of linking Aadhaar with the provident fund Unique Account Number (UAN) is that it increases transparency and makes the verification process easier.

Before linking your Aadhaar card, you need to activate your UAN. Once done, you can update your UID number online through the process outlined below:

- Visit - https://unifiedportal-mem.epfindia.gov.in/memberinterface

- Login with your UAN and password

- Under the ‘Manage’ tab, select ‘KYC’

- Under this, you have the option to update details of several identification proofs, including Aadhaar

- Enter your Aadhaar number and name as per Aadhaar and click “Save’

Your Aadhaar should get linked within a couple of weeks if all personal details match.

How can I check EPF balance online?

5 steps to check the EPF balance/ Passbook using an UAN:

Step 1: Open the web page https://passbook.epfindia.gov.in/MemberPassBook/Login.jsp

Step 2: Enter your Universal Account Number of UAN.

Step 3: Enter your password set for the UAN portal & fill in the captcha code

Step 4: Once logged in, select your EPF account number from the list.

Step 5: The passbook with updated balances will be loaded on the page.

How to check EPF balance via SMS or Missed Call?

Employees can now check their EPF balance through SMS or by giving a missed call. One such way which comes in handy at times when you do not have an active online connection is via SMS or missed calls. For this you will need to have an activated UAN number. In case you have a valid UAN, your mobile number too will be registered with the EPF department. Giving a simple missed call to 011-22901406 will ensure that you receive a SMS that lists down your PF number, age and name as per the EPF records. However, you will require your UAN along with Aadhaar Number or PAN Number in order to know your EPF balance.

KYC details along with UAN are mandatory for knowing your EPF balance. Once your UAN is integrated with your KYC, every time you give a missed call to the Employee’s Provident Fund department, you will receive SMS with your EPF details including the EPF balance.

How to check EPF balance EPFO mobile app

EPFO recently launched a mobile app for PF balance tracking riding on the mobile application trend in the Indian market. The mobile app helps to check the EPF balance and generate an account statement. The mobile app currently in the market is only available for the android version. EPFO will soon be launching mobile app versions for both blackberry and iOS devices.

Steps for using the EPF mobile app:

- Step 1: Open the mobile app – Umang (https://web.umang.gov.in/web/#/) - on your phone and click EPFO

- Step 2: Under the Employee Services option, click passbook and then input your 12-digit UAN number. The system will send an OTP to the mobile number registered with the EPFO

- Step 3: Once verified, you will be shown a screen which displays your updated EPF balance information along with personal details like your name, date of birth, Aadhaar number; PAN for tax deduction, last month EPF contribution etc.

The Mobile App is a good and handy way to check your EPF balance and that too on the go.

All that you need to know about EPF e-Passbook

With the help of EPF e-passbook you can actually check the contribution you make to your EPF account every month. You can even double check and be aware of your latest EPF balance as well.

We have laid down few steps as below:

Step 1: Visit this website http://members.epfoservices.in/ and click on “Click here to register”

Step 2: After clicking on the link, you will be asked to enter the following data as shown in the image below:

- Mobile number

- Date of Birth

- Select a document (Pan / Aadhaar / Voter’s ID / License / Bank Account Number / NPR / Passport / Ration Card

- Enter the number as on the document. This may be alphanumeric, enter the number exactly as it is on the document

- Enter the Name as on the document

- Enter your Email ID, and click GET PIN

- Don’t close the web page. The PIN will be sent to your mobile number.

Step 3: Once you have the PIN, you have to enter it in the box on the same web page, so don’t close the webpage. Select “I Agree” if you agree to the terms and enter the Pin and submit. You will see the following message: Registration successful. Your username and password has been sent to your mobile number. Please login to the EPFO portal with the same.

Step 4: Login with your ID. Click on “Download E Passbook”. You will be asked to Select the state where your establishment is covered and choose the EPFO Office. Then you will be directed to a screen such as this one:

When you generate the PIN, it will be sent to your mobile number and your mail ID. Enter the PIN on the space for Enter Authorization PIN (see the screen shot above) and click Get Detail. You will then be able to download a PDF file which contains your EPF Balance and other details.

How to read my EPF e-Passbook

Now, as we’ve covered before, the employee contribution is a straight 12% into the EPF.

But the employer’s contribution is allocated across the EPF and the EPS. The employer also bears 3 additional costs i.e. the EDLIS, the EPF admin charges and the EDLIS admin charges.

Your EPF passbook will tell you your contribution, and also the interest earned and accrued in your EPF account. You should clearly understand the entries in this slip to ensure you are able to track your account correctly.

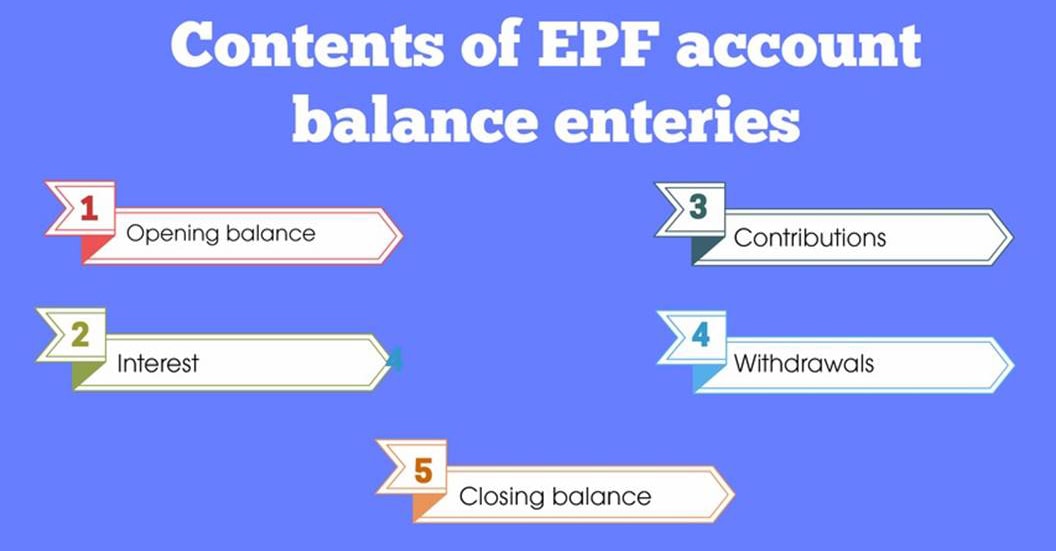

How do I read the EPF account balance

Your account balance will usually have the following entries.

-

Opening balance:

This is the amount you have accumulated till the beginning of a financial year. In the example above, the opening balance will indicate the fund balance at the start of the corresponding financial year (FY). This amount is further divided into two heads—employee’s contribution (the amount contributed by you plus interest) and employer’s contribution (the amount contributed by the employer plus interest)

-

Interest:

This entry indicates the interest that has been credited to your account for the corresponding FY

-

Contributions:

This shows the payments made by you and your employer in the corresponding FY

-

Withdrawals:

Any partial withdrawals or advances that you may have taken

-

Closing balance:

This is the sum of all the entries—the opening balance plus interest accrued on the opening balance and on the contributions made in the corresponding FY, plus the contributions made in the financial year. Advances you may have taken would be deducted from this kitty. This closing balance will become the opening balance for the next financial year

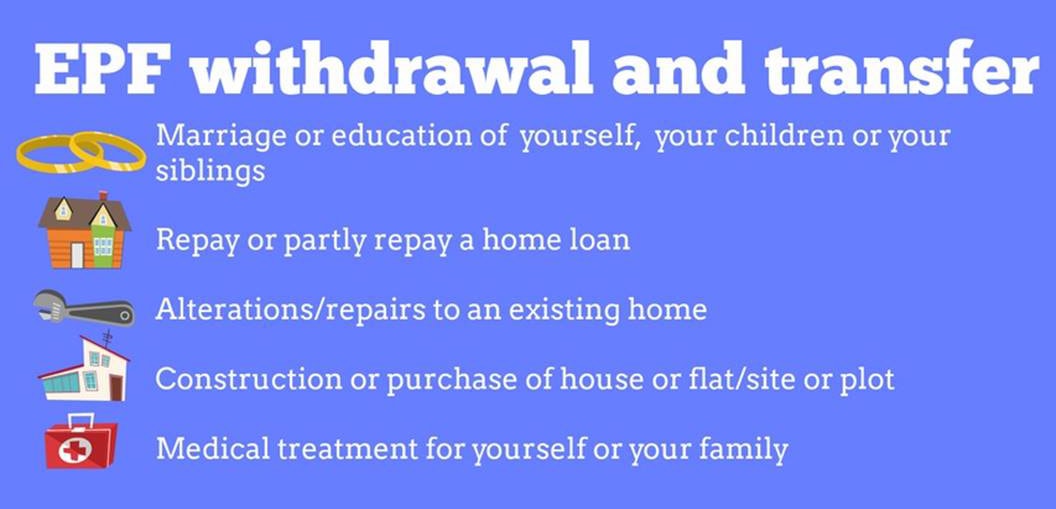

All about EPF withdrawal and transfer

Under what circumstances can I withdraw my EPF money?

Technically, the EPF is not withdrawable while you are still working, but there is some leeway here. The EPF balance can be withdrawn on certain occasions or to meet certain specific expenses, under certain conditions, such as:

- Marriage or education of your children, yourself or your siblings

- Minimum 7 years of service should be completed

- Maximum amount that can be drawn is 50% of the till-date contribution- This can be availed 3 times only

- Proof of the wedding or education is required i.e. wedding invite or certified copy of fee payable

- To repay or partly repay a home loan in your name, your spouse’s name, or jointly owned by you both

- For this the rules are a little stricter. You need to have completed at least 10 years of service

- The amount is also correspondingly larger, you can draw up to 36 times your basic salary

- Alterations/repairs to an existing home for house in the name of self, spouse or jointly

- You need a minimum service of five years (10 years for repairs) after the house was built/bought

- You can draw up to 12 times the wages, only once

- Construction or purchase of house or flat/site or plot for self or spouse or joint ownership

- You should have completed at least five years of service

- The maximum amount you can avail of is 36 times your wages. To buy a site or plot, the amount is 24 times your salary

- You can avail of this once during your entire working life

- Medical treatment for yourself or your family (spouse, children, dependent parents)

- If you are going to undergo a major surgery such as for leprosy, cancer, heart illness, mental ailments, or even TB, you can apply to withdraw your EPF

- The maximum amount you can draw is 6 times your basic salary

They will require proof of hospitalization for one month or more, along with a leave certificate for the corresponding period from your place of work.

Now let us look at EPF transfer options.

Is it illegal to withdraw the PF in between jobs?

This is a little-known fact about the EPF that is often flouted. But yes, it is illegal to withdraw your PF between jobs. Withdrawal of the complete PF is allowed only under above circumstances only.

Then, how do I transfer my EPF account when changing jobs?

The UAN number makes it simple to track your funds even while you move from one organisation to another at any point of time.

You, too, can follow these steps and complete the hassle-free transfer procedure:

Step 1: Check Your Eligibility

To transfer your EPF money online from one account to another, you need to first be eligible to do so. You can check your eligibility at the Online Transfer Claim Portal (OTCP) under the category “FOR EMPLOYEES” on the home-page of EPFO website – www.epfindia.gov.in .

If you are eligible for the online transfer, then register as a member on the portal. If you are already a registered member, you can directly log-in into Online Transfer Claim Application. Click on “Request for Transfer of account” to file online Transfer Claim. If not, you need to register yourself on the portal.

You need to be sure either your current employer or previous employer has digital signature. Besides, keep handy the previous and the current employers’ PF details.

Step 2: Fill in the Application Form

Once you’ve followed the above procedure, fill in the application form. This is divided into Part A, B, and C.

Part A consist of filling all your personal details

such as name, mobile number, e-mail id, bank account number, and bank’s IFSC Code.

Part B pertains to details of your previous employer.

You need to enter your PF account number and go to

“click here to get details”. The details regarding your employer will appear. Further, the details such as joining date, date of leaving, father/ spouse’s name will appear. But, if there are any missing details such as date of birth etc., it is mandatory for you to fill in these.

Part C is about your current employee PF account.

On entering your PF account number, the employer details will appear, and if some details are missing, you need to enter these.

The important point at this step is to claim attestation. You have an option to either get it attested through the previous employer or present employer. The employer gets the notification via email and on the EPF portal. Your application will be verified by the employer and will be forwarded to the EPFO.

Once your application has been completed, a preview of your form can be seen. In case you require to change any details, look for “TO change application data, click here”.

Step 3: Submit the form

At this step, a Captcha code will appear; type that into the field and click on “GET PIN” button. But before you go ahead, don’t forget to signify your assent by selecting the button, “I Agree”.

Soon, you will receive the PIN on your registered mobile number. Submitting the PIN you’ve received will complete your online application transfer process.

Step 4: Track your transfer status

A tracking ID will be generated once the application is over. With this, you can track your online application. And don’t forget to save the Printable Transfer Claim Form (Form 13) generated on your machine (desktop, laptop, tablet, phablet, smartphone or any other gadget you’re using), take a print-out, sign and send it across to the employer (current or previous) you’ve chosen to complete the claim process.

Online transfer claim has simplified the whole process and is hassle free. It takes 30-60 days to complete the claim settlement process and for the transfer to be done. Even your employer can view, verify or correct, and submit your details online through this portal.

Conclusion: From a Financial Planning perspective…

For a salaried person, contributions to the EPF offer a lot of benefits:

a) Safe returns: This is one of the safest debt instruments available in the country. It is government backed and guarantees safety of principal and interest earned. It can help you accumulate a significant corpus for your retirement, as the contributions happen month on month for your entire working life. This makes it suitable for very long term financial goals.

b) Friendly tax treatment: This is an E-E-E instrument – meaning your contributions are deductible under Section 80C, interest earned is tax free and maturity proceeds are also tax free, provided contributions to the fund have been for more than 5 years of service.

c) Interest earned on EPF is the equivalent of a high pre-tax rate: Considering that the EPF is paying 8.75% this year, this is the equivalent of a 12.50% rate of interest (for somebody in the 30% tax bracket). This interest rate is guaranteed and risk-free.

Apart from the main features, it also allows withdrawals as detailed in an earlier question and you can also avail a loan against your EPF, using it as security.

However, keep in mind; this is a very long-term instrument. If you have short term financial goals, don’t try to fund it by withdrawals from your EPF. If your goals are in fact primarily short term, as is the case with young couples, or parents funding their children’s educations in a few years, you might want to consider only investing the minimum amount in your EPF, and channelizing your remaining funds towards a more liquid instrument, keeping your risk appetite and goal time horizon in mind.

Download the free EPF guide:

The Complete Guide to Public Provident Fund (PPF) - Edition 2017