What is STP?

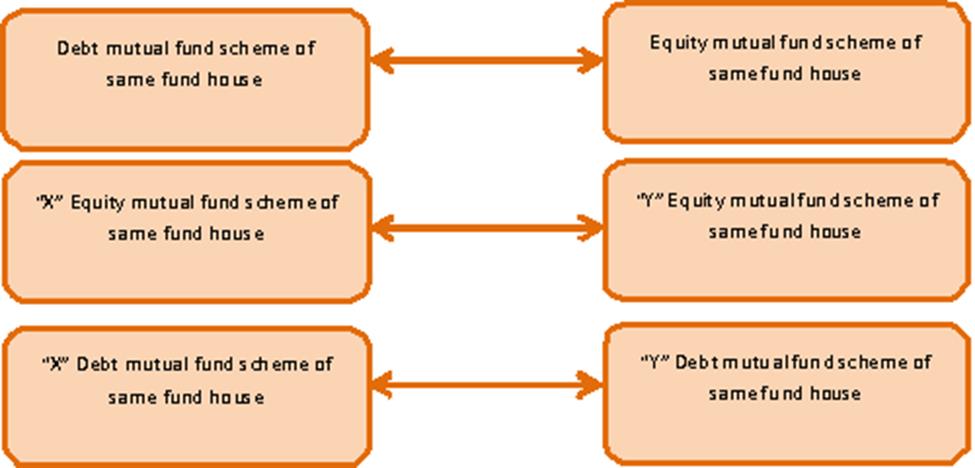

If you have a lump sum amount and want to transfer that amount over a period of time to Equity Funds, Systematic Transfer Plan (STP) is the most suitable option for you. Under a mutual fund Systematic Transfer Plan (STP), a lump sum amount you invested in one scheme can be transferred at regular intervals systematically in a piecemeal manner into another mutual fund scheme (as desired by you) of the same mutual fund house. Most fund houses have a daily, monthly, weekly, and quarterly option to transfer money. But not all offer the weekly option – only a handful of them do. Moreover, different fund houses have different requirements for the minimum amount invested through STP.

How does STP work?

To gain the maximum benefit of a STP and market volatility, a lumpsum amount can be initially invested in an ultra-short term debt fund and/or a liquid fund. This amount can be systematically transferred –monthly or quarterly – to an equity-oriented fund of your choice (but ideally which can prove worthy for long-term wealth creation) over a period.

If you would prefer to stay invested in liquid funds today, but going forward you also want to take a gradual exposure towards equity (as you perceive them to do well), you can certainly opt for the STP option offered by mutual funds. Likewise, if you expect the markets to undergo a corrective phase, and thus as a smart move you prefer gradually disinvesting from equity mutual funds, then you can opt for an STP from your equity fund and transfer into a liquid fund

Also, while you plan some of your important financial goals such as buying your dream home, getting married, children’s education, their marriage, your retirement, etc.; STP can be of great utility because it can help you to shift gradually from equity to debt as you are near to your financial goals.

Under STP, a lump sum amount earlier invested by you can be transferred at regular intervals in a piecemeal manner systematically into another mutual scheme (as desired by you) of the same fund house. Typically, 6 such transfers are allowed by the fund houses. Also, most funds houses generally allow an STP from a debt mutual fund scheme to an equity mutual fund scheme, and only handful of them allow it vice versa. Likewise, most fund houses allow a monthly or a quarterly option, while a handful of them allow even a weekly or a quarterly option. Moreover, different fund houses have different requirements for the minimum amount to be invested through STP.

STP Calculator

But do you know how much is your total return on your investment? PersonalFN STP calculator will help you to find out total value of your investment when you opt for STP from a Liquid Fund to Equity Fund.

Our STP calculator is easy to use. Just enter the lumpsum amount you wish to invest, the STP tenure, STP amount and the rate of return of the source liquid or debt mutual fund scheme and the equity mutual fund scheme. The calculator will calculate the STP returns instantly.

This STP Calculator, a simple tool will help you make smart decision and utilisation of your money. It will calculate returns you will earn from Equity as well as Debt Fund.

STP Calculator will calculate complex calculations which you individually might dread of doing. And hence might guide you in making informed decision

Why STP

We all know that mutual funds are the most efficient way to take exposure to the equity markets. In today’s market scenario, while one may aim to take advantage of both equity and debt markets, there is an inherent risk involved. Thus, when taking exposure to these respective asset classes, it is important to adopt a cautious approach, and proceed smartly and prudently.

The STP facility is best suited for investors who seek stable returns with some exposure to equity funds with an objective of wealth creation. Debt funds are ideal for capital protection and equity funds are suitable for investors looking for capital growth. Hence, a blend of different types of funds always helps to strike the balance between both asset classes.

Very often while reallocating assets within categories of mutual fund schemes, investors tend to give redemption request forms, and then invest into another mutual fund scheme as they deem fit. However, one can use an STP to transfer the money systematically in such cases. A STP can work as an alternative to SIP as well if you have a substantial amount lying in your savings account. The debt scheme you choose has the potential to earn a higher return that your bank savings account.

When to opt for STP

Say you earned a promotion and received a hefty bonus of Rs 5 lakh, and you decide to invest this sum into equity mutual funds. But as the markets are currently at an all time high, you realise it wouldn’t be wise to invest all your winnings in one go. The entire sum can be initially invested in an ultra-short term debt fund and/or a liquid fund taking cognisance of the fact that markets are at a high. Then, systematically a certain sum of money lying in the liquid fund and/or ultra-short-term fund can be transferred –monthly or quarterly – to an equity-oriented fund of your choice (but which ideally can prove worthy for long-term wealth creation) over a period of time.

Alternatively, same Rs 5 lakh bonus earned can be used smartly under SWP as well. Instead of saving it in your savings account and withdrawing Rs 10,000 every month, you can withdraw smartly under SWP and reap the benefits of compounding.

| Month |

Cashflows |

NAV |

Fund Units |

Value |

| Jan |

5,00,000 |

100 |

5,000 |

5,00,000 |

| Feb |

-10,000 |

103 |

4,903 |

5,05,000 |

| Mar |

-10,000 |

102 |

4,805 |

4,90,097 |

| Apr |

-10,000 |

105 |

4,710 |

4,94,511 |

| May |

-10,000 |

108 |

4,617 |

4,98,641 |

| June |

-10,000 |

106 |

4,523 |

4,79,407 |

Note: The above table is for illustration purpose only

(Source: PersonalFN Research)

If you withdraw Rs 10,000 under SWP, your holdings will decline to 4900 units (i.e. Rs10000 / Rs100 NAV = 100 units are reduced from his initial holdings) in the first month.

In next month, NAV of the fund has appreciated to Rs 101 due to market dynamics. The number of units equivalent to Rs 10,000 i.e. only 99 units will be sold (i.e. Rs 10000/ Rs 101 NAV = 99 units).

In five months, when you withdraw a total of Rs 50,000, your effective portfolio would value at Rs 4,50,000. However, the total value is now Rs 4,79,407; effectively proving to be a better earning instrument due to the market dynamics vis-à-vis parking money in a savings account, and/or other traditional instruments such as fixed deposits.

For example, you invest Rs 5,00,000 in Fund A. If the net asset value (NAV) of the fund is Rs 100, then you will hold a total of 5,000 units.

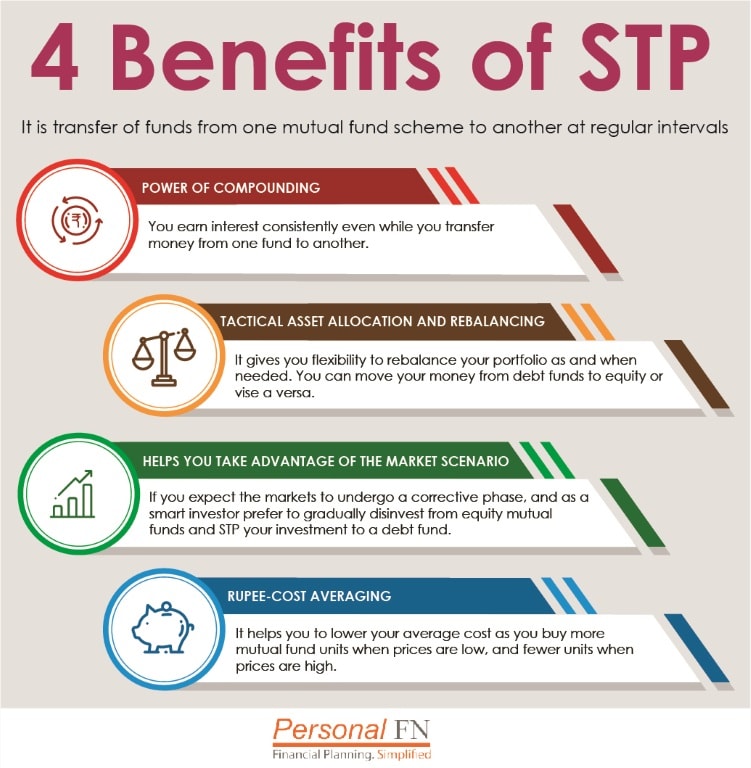

Benefits of STP

-

Power of Compounding

Like SIP, Systematic Transfer Plans too facilitates power of compounding.

-

Tactical asset allocation and rebalancing

Say you prefer to stay invested in liquid funds today, but going forward you also want to take a gradual exposure towards equity (as you perceive them to do well), you can certainly opt for the STP option offered by mutual funds. Likewise, if you expect the markets to undergo a corrective phase, and as a smart investor prefer to gradually disinvest from equity mutual funds, STP to a liquid fund or an ultra-short term fund can be potent tool.

Thus, STP enables you to actively…

- Rebalance your portfolio; and

- Take advantage of the market scenario

-

Help in financial planning

When you’re planning for any important long-term financial goals, STPs can be of great utility because it can help you to shift gradually from equity to debt when you are nearer to your financial goal deadline.

-

Rupee-cost averaging

With the strategic advantages that STPs bring, even rupee-cost averaging can facilitate reducing the risk to your portfolio.

But while you opt for an STP, for benefits it offers, you also got to be cognisant about the cost and tax implications.

Cost and tax implication of STP

-

Loads

While you exit (i.e. withdraw) from one scheme into another, the exit loads would be applicable if your transaction falls under the criteria which enforces you to pay the same. Thus, the exit load of the scheme from where you are transferring will be levied and thereby an impact of the same in the form of number of units would be noticed in target scheme, if you are transferring during the period when exit load is applicable.

-

Taxation

While you transfer your investments from a mutual fund scheme to another, the Income Tax Act, 1961 construes it to be sale transaction, and thus the provisions of the Act apply as well. Likewise, a Securities Transaction Tax (STT) will be levied at the time of exit i.e. from one equity oriented fund to a debt scheme, or even another equity mutual fund scheme (of the same fund house). However, for transfer from debt mutual fund schemes to equity oriented mutual fund scheme, STT is not levied.

3 Types of STPs

There are broadly 3 types of STP options:

-

Fixed STP

Under this, the amount to be transferred via the STP is fixed (predetermined at the time of investment). The specified amount is transferred to the desired (i.e. target) mutual fund scheme.

-

Capital Appreciation or Profit generated

Under this STP option, the capital appreciation or the profit generated on you’re the invested amount is transferred to the target scheme, leaving the principal intact. Hence, this option works well if one intends to book regular profits and plough them into debt mutual fund schemes from the same fund house.

-

Flexi or Variable STP

Under Flexi STP you have a choice to transfer variable amount. The minimum amount under this STP option is fixed, but subject to volatility in the market the variable amount is decided. If the NAV of the target fund falls, investment can be increased to take benefit of falling prices and likewise if the market moves up, the minimum amount of transfer is invested to take advantage of increasing prices. Transfer facility is available on a daily, weekly, monthly and quarterly interval.

Thus, from an asset allocation point of view also if we assess it is indeed a useful option/tool which enables one to gradually shift between debt and equity. Thus, say if you would prefer to stay invested in liquid funds today, but going forward you also want to take a gradual exposure towards equity (as you perceive them to do well), you can certainly opt for the STP option offered by mutual funds. Likewise, if you expect the markets to undergo a corrective phase, and thus as a smart move you prefer gradually disinvesting from equity mutual funds, then you can opt for an STP from your equity fund and transfer into a liquid fund. Hence this convenience offered by STP enables you to:

- Rebalance your portfolio; and

- Take advantage of the market scenario

Also, while you plan some of your important financial goals such as buying your dream home, getting married, children’s education, their marriage, your retirement, etc.; STP can be of great utility because it can help you to shift gradually from equity to debt as you are near to your financial goals.

STP is a smart way of gaining the best of your money.

The STP facility is best suited for investors who wish to completely stay invested, while they transfer funds from one mutual fund scheme to another, from a portfolio review standpoint or for the purpose of systematic asset allocation in the objective of wealth creation. Debt funds are ideal for capital protection and equity funds are suitable for investors looking for capital growth. Hence, a blend of different types of funds always helps to strike the balance between both asset classes.

Thus, the next time you wish to transfer your funds from one mutual fund scheme to another or wish to withdraw small amounts regularly keep in mind this simple, yet effective option provided by mutual funds.

To learn more about various modes of mutual fund investing watch the below video.

Happy Investing!