Market Overview

The gains witnessed in the month of January 2013 were completely washed in the month gone by, as the Indian equity markets (i.e. the S&P BSE Sensex) descended by -5.2% (or 1,033.44 points) as edgy disposition gripped the market ahead Union Budget 2013 and worry over twin deficit problem (occurring on account of ballooning fiscal deficit and widening Current Account Deficit (CAD)) prevailed. With the Central Statistical Organisation (CSO) and the RBI projecting India's growth for fiscal year 2012-13 at 5.0% and 5.5% respectively plus Q3FY13 GDP growth reported at 4.5%, the markets seemed concerned over the slowdown in economic growth rate, although the Reserve Bank of India (RBI) has reduced policy rates as well as CRR each by 25 basis points (bps) in a move to address growth risk, while WPI inflation is depicting some signs of moderation. WPI inflation data for January 2013 released on February 14, 2013, mellowed down further to 6.62% in January 2013 (from 7.18% in December 2013), but on that date the Indian equity markets didn't respire and in fact ended the trading day in the red (-110.90 points) eroding the gains (of +147.51 points) made in the immediately preceding two trading sessions. The 'see-saw' movement in Index of Industrial Production (IIP) data (with contraction reported in November 2012 and December 2012) too seemed to be a worrisome picture for the market.

Later as the markets moved forward towards the Budget week, global events also led to Indian equity markets to descend. First the release of minutes of the Fed meeting (on February 20, 2013) got the markets into a tizzy on February 21 2013 (with the markets losing -317.39 points) as the Fed raised doubts about the continuation of its open-ended Quantitative Easing (QE3) programme. Second, the markets roiled on February 26, 2013 as investors were concerned that election results in Europe's fourth largest economy could hinder economic reforms in the zone and drive up borrowing costs. So, there were headwinds from the global economy as well.

The Union Budget 2013 too which was considered as a major event for the market, before the India head for General election next year; failed to cheer the Indian equity market, with no populist moves made in an attempt to walk tight on the path of fiscal consolidation. While in the Union Budget the Government proposed to reduce the Securities Transaction Tax (STT) on equity futures from 0.017% to 0.01%, the move of keeping STT unchanged for cash transaction was a disappointment for the market. We believe, in order to increase retail participation into Indian equities, the Government should have instead reduced STT in the cash segment. Likewise, the increase in excise duty and custom on certain goods and service tax on dinning in air conditioned restaurants was not taken positively by the market. Moreover, a statement in the budget saying, if an FII or a non-resident wants to avail of tax treaty benefits, then a tax residency certificate (TRC) alone would not be sufficient; spooked the Foreign Institutional Investors (FIIs) and led them to net sellers in the Indian equity markets on the date of announcement of the Budget, and gauging the overall budget and its impact, on the Budget day the market ended the trading session in the red. (-290.87 points)

As far as the precious yellow metal - gold is concerned; it too continued with its corrective move (as it did in the last couple of months), and ended the month gone by below Rs 30,000 mark. The descending move was as a reflection of reflection of a sharp correction in the world market occurred on account of overreaction from the Fed meeting minutes released, (on February 20, 2013) which reconsidered scale and duration of QE3 programme. But the fall in prices nudged smart investors to buy into gold with uncertainty looming around in the global economy, intermediate inflationary pressures yet imminent and Indian rupee remaining under pressure due to widening CAD. Thus although import duty on gold was hiked to 6% in an attempt to curb gold imports, it didn't deter demand from investors. In fact we are also of the view that, hike in import duty on gold could lead to illegal activity such as smuggling of gold, thereby keep demand buoyant until global economy shows signs of stability.

Speaking about Brent crude oil, prices eased (by -5.3%) after shooting up in the month of January 2013, with concerns having resurfaced about the global economy and the strength of demand. Moreover, the markets remained cautious ahead of looming U.S. spending cuts.

For the bond markets, although the RBI in its 3rd quarter review of Monetary Policy 2012-13 infused primary liquidity in the system vide a CRR cut of 25 basis points (bps) and reduced repo rate by the same magnitude, liquidity remained tight in the month of February 2013. The average borrowing of banks under the LAF window, stood over Rs 1,00,000 crore in February 2013. Thus short-term CD yields inched-up at the end of the month, with 1-month and 3-month CD yields placed at 9.6% each respectively. However, taking cues from what was enunciated in Budget 2013 - especially the agenda of fiscal consolidation (that would help save the nation from ratings downgrade), RBI's guidance as given in its last monetary policy and moderation in inflation, the 8.15% 2022 (10-Yr) G-Sec yield mellowed by 2 bps to end the month at 7.87%. Going forward, for the fiscal year 2013-14 the government has raised the budget expenditure and will need to borrow Rs 4.84 lakh crore or around 89% of the fiscal deficit from the bond markets. Such high borrowing target may keep the markets under pressure for some time. The Indian debt markets would be watchful over what stance does RBI takes in its next mid-quarter review of Monetary Policy 2012-13 (scheduled on March 19, 2013), liquidity conditions and how the Government achieves the ambitious fiscal deficit target of 4.8%. At present while the efforts taken by RBI and Government have helped bring down the headline WPI inflation to below 7% and core inflation to about 4.2%, the food inflation is still high and intermediate risk to inflation yet persists due to hike in prices of diesel and freight charges.

Monthly Market Roundup

|

As on Feb 28, 2013 |

As on Jan 31, 2013 |

Change |

% Change |

| BSE Sensex |

18,861.54 |

19,894.98 |

(1,033.44) |

-5.2%  |

| S&P CNX Nifty |

5,693.05 |

6,034.75 |

(341.70) |

-5.7% |

| CNX Midcap |

7,540.35 |

8,363.70 |

(823.35) |

-9.8% |

| Gold (Rs/10 gram) |

29,520.00 |

30,335.00 |

(815.00) |

-2.7% |

| Re/US $ |

54.36 |

53.23 |

(1.13) |

-2.1% |

| Crude Oil ($/BBL) |

109.74 |

115.94 |

(6.20) |

-5.3% |

| 8.15% 2022 (10-Yr) G-Sec Yield (%)* |

7.87 |

7.89 |

(0.02) |

2bps |

| 1-Yr FDs |

7.25% - 9.00% |

*The 8.15% 2022 is the new 10-Yr benchmark which was introduced on June 9, 2012

(Monthly change as on February 28, 2013) (Source: ACE MF, PersonalFN Research)

As far as participation of Foreign Institutional Investors (FIIs) in the Indian equity market is concerned, it was quite heartening to see them buy and the ascending trend to continue. Despite India's economic growth forecast being murky and there being lull industrial activity, they net bought to the tune of Rs 24,439 crore, thereby accelerating a little further from their last month's activity, where they net bought to the tune of Rs 22,874 crore. They seemed to have exuded confidence in Indian equities on account of:

- GAAR being deferred until April 2016 and P-Notes excluded therefrom

- Inflationary pressures reducing (WPI inflation at 6.62% for January 2013)

- RBI turning focus to address to growth risk

- Government showing commitment on its path of fiscal consolidation

- Union Budget 2013 being a balancing act

- Weakening Indian Rupee facilitating their flows

- Easy monetary policy adopted by the central bankers in the developed economies

- Better economic growth prospects in the future with reform measures being supportive thereto

BSE Sensex vs. FII inflows

(Source: ACE MF , PersonalFN Research)

Moreover, with their investment focus being on Emerging Market Economies (EMEs) due to better economic growth prospects as compared to developed economies; Indian equity markets benefitted from their participation.

Mutual Fund Overview

Contrary to the roaring participation of Foreign Institutional Investors, domestic mutual funds (MFs) continued to be net sellers in the Indian equity markets yet again. But a noteworthy point is that the magnitude of selling was reduced when compared to last month with Rs 848 crore of equities sold by them, vis-à-vis Rs 4,734 crore being net sold in January 2013.

The fund manager seemed to have evinced confidence on account of:

- Reform measure taken by the Government;

- Commitment shown on the path of fiscal consolidation

- RBI turning focus to address to growth risk

- Union Budget 2013 being a balancing act

- Inflationary pressures reducing (WPI inflation at 6.62% for January 2013)

However concerns over how the Government handles the twin deficit problem and precludes sovereign ratings downgrade for India yet remained, along with Political turbulence ahead of general elections in 2014.

BSE Sensex vs. MF inflows

(Source: ACE MF, PersonalFN Research)

As far as the performance of various categories of mutual funds is concerned, in the diversified equity funds category, losses were evident across market capitalisation bias and investment styles followed; except value style funds which ended the month in green. However, mid cap funds and those betting on emerging businesses fell more with the mid cap index plunging more.

Among the sector funds, those focusing on investing in the technology sector occupied the top position aided by the persistent weakness in the Indian rupee for most part of the month, which helped the underlying stocks in their portfolio (especially the export oriented ones) perform well. The rest of the sector and thematic funds ended the month gone by in red with infrastructure funds taking the maximum hit. As far as ELSS funds are concerned (which follow fluid investment style, they too eroded investors' wealth with the corrective witnessed by the market.

In the Fund of Fund (FoF) category, some of those focusing on investing the world markets - especially in ASEAN (Association of Southeast Asian Nations) equities (by being feeder funds by nature), reported gains; while those structured as financial planning funds or asset allocation funds ended the month gone by in negative. World gold mining funds and other mining funds too reported losses with the underlying equities not depicting a favourable move. Domestic gold saving funds (which invest in gold ETFs) too eroded investors' wealth with the precious yellow metal undergoing a corrective.

Speaking about the hybrid funds; amongst the balanced funds all of them delivered negative returns, treading with downward movement of the Indian equity markets. The debt portion of the Assets Under Management (AUM) too remained under pressure with short-term yields inching-up (due to tight liquidity conditions) and yields of long-term debt papers not falling much. Thus Monthly Income Plans (MIPs), which invest a dominant portion of its assets in debt securities across maturities, also did not see any magnanimous gains. Only 6 funds managed from the complete category managed to end the month gone by in green, while the rest delivered negative returns. The equity portfolio of MIPs too came under stress with the descending move depicted by the Indian equity market in the month gone by.

Monthly top gainers: Open-ended Equity Funds

| Diversified Equity Funds |

1-Mth |

Sector Funds |

1-Mth |

ELSS |

1-Mth |

| Axis Equity Fund (G) |

-2.27% |

Franklin Infotech Fund (G) |

5.62% |

Quantum Tax Saving Fund (G) |

-3.46% |

| Religare Equity Fund (G) |

-2.49% |

SBI Infotech Fund (G) |

4.32% |

Tata Tax Adv Fund-1 |

-3.48% |

| Birla SL India Opportunities Fund (G) |

-3.01% |

ICICI Pru Technology Fund (G) |

2.81% |

Axis LT Equity Fund (G) |

-3.61% |

(1-Mth returns as on February 28, 2013)

(Source: ACE MF, PersonalFN Research)

Monthly top gainers: Open-ended Fund of Funds

| Fund of Funds |

1-Mth |

| JPMorgan JF ASEAN Eq Off-shore Fund (G) |

4.07% |

| ING Global Real Estate Fund (G) |

1.09% |

| ING Active Debt Multi-Mgr FoF (G) |

0.98% |

(1-Mth returns as on February 28, 2013)

(Source: ACE MF, PersonalFN Research)

Monthly top gainers: Open-ended Hybrid Funds

| Balanced Funds |

1-Mth |

Monthly Income Plans |

1-Mth |

| LIC Nomura MF Balanced Fund (G) |

-2.36% |

Sahara Classic (G) |

0.52% |

| ING Balanced Fund (G) |

-3.15% |

Templeton India Low Duration Fund (G) |

0.47% |

| FT India Balanced Fund (G) |

-3.36% |

Principal Debt Savings Fund (G) |

0.34% |

(1-Mth returns as on February 28, 2013)

(Source: ACE MF, PersonalFN Research )

Monthly top gainers: Open-ended debt funds

| Floating Rate Funds |

1-Mth |

Income Funds |

1-Mth |

Gilt funds |

1-Mth |

| Short Term |

|

Short Term |

|

Short Term |

|

| Kotak Floater-ST (G) |

0.60% |

Taurus ST Income (G) |

0.65% |

HSBC Gilt-ST-Reg (G) |

1.04% |

| SBI Mag Income FRP-Sav Plus Bond-Reg (G) |

0.59% |

JPMorgan India ST Income (G) |

0.61% |

Edelweiss Gilt Fund (G) |

0.99% |

| SBI Mag InstaCash-Liquid Floater (G) |

0.57% |

Peerless Short Term Fund - Reg (G) |

0.58% |

IDFC G Sec-STP-Reg (G) |

0.80% |

| Long Term |

|

Long Term |

|

Long Term |

|

| Sundaram Flexible-FIP (G) |

0.80% |

IDFC SSIF-Invest-Reg (G) |

1.24% |

Religare Gilt Fund - LDP (G) |

1.56% |

| SBI Magnum Income FR-LTP-Reg (G) |

0.59% |

IDFC Dynamic Bond-A (G) |

1.24% |

IDFC G Sec-Invest-A (G) |

1.46% |

| HDFC FRIF-Long Term Plan (G) |

0.57% |

Tata Dynamic Bond Fund-Plan A (G) |

1.15% |

IDFC G Sec-PF-Reg (G) |

1.42% |

| Liquid Funds |

1-Mth |

Liquid Plus funds |

1-Mth |

| Escorts Liquid Plan (G) |

0.69% |

PineBridge India Treasury-Ret (G) |

0.96% |

| PineBridge India Liquid Fund (G) |

0.64% |

BOI AXA Treasury Adv Fund-Reg (G) |

0.63% |

| Tata Liquidity Mgmt (G) |

0.61% |

JM Money Mgr-Reg (G) |

0.63% |

(1-Mth returns as on February 28, 2013)

(Source: ACE MF, PersonalFN Research )

As far as performance of debt mutual fund scheme is concerned, since short-term yields inched-up with liquidity condition being tight (as mentioned earlier), the performance of short-term floating rated debt funds, short-term income funds and short-term gilt funds fell short as against that witnessed in the month of January 2013. In the long-term debt funds too (mandated to invest in the longer maturity papers i.e. medium to long), gains seemed to have been restricted with yields of long-term papers not mellowing down much despite inflation showing signs of moderation and RBI hinting that it would address to growth risk. It appeared that the debt market seemed to be worried over the twin deficit problem which has a large impact and puts the country to risk of a rating downgrade.

Going forward, if the country's central bank indeed reduces policy rates in its next mid-quarter review of monetary policy (scheduled on March 19, 2013) thereby addressing to growth risk and fiscal deficit target of 5.2% for the current fiscal year is achieved (and 4.8% for the next fiscal year); we may witness some mellowing in yields. But in the intermediate liquidity is likely to tight with advance tax payments in mid-March 2013.

It is noteworthy that in the Indian debt market, both FIIs and domestic mutual funds continued to be net buyers with FIIs having bought net to the tune of 4,001 crore thereby accelerating from January 2013's net buying worth Rs 3,326 crore. But domestic mutual funds participated in a roaring manner in the Indian debt markets by being net buyers net to the tune of Rs 40,092 crore; although when compared to January 2013, they bought less.

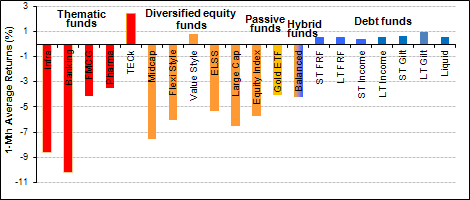

Performance across various categories of mutual funds

(1-Mth average returns of funds in various categories as on February 28, 2013)

(Source: ACE MF, PersonalFN Research)

The graph above depicts how various categories of mutual funds performed in the previous month. Amongst the sector and thematic funds, banking funds followed by infrastructure funds took the maximum beating and even FMCG and pharma which are defensive in nature eroded investors' wealth. Only tech funds managed to create wealth for investors aided by weakening in the Indian rupee, which set to be positive for the sector. From a market capitalisation basis, mid and small cap funds fell more (with the mid cap index plunging more), as compared to large caps; while from a fund management style perspective barring funds following a value style approach to investing, the rest ended the month in red.

Tracing with the marginal descending move in the precious yellow metal - gold, Gold ETFs exhibited marginally negative returns for investors (on average -4.1%).

In the debt mutual fund category, those with a mandate to invest in shorter maturity instruments displayed slightly lower returns as compared to those seen in January 2013, as yields of short-term debt papers inched-up with liquidity conditions remaining tight. Limited gains were seen in the long-term debt funds as yields of long-term papers didn't mellowing down much despite inflation showing signs of moderation and RBI hinting that it would address to growth risk.

Other News and New Fund Offers

- Until recently, some influential investors in debt mutual fund schemes made a quick buck by using a loophole in debt mutual fund investing to their advantage. As per the guidelines, investors investing a sum of money below Rs 2 lakh in a debt mutual scheme, enjoy the NAV of the date of application of the scheme, although the cheque takes couple or more days to clear. This had encouraged rich investors to participate in debt mutual funds for the short-term, where they were induced even to exit their investments even without their application money leaving their bank account. Moreover, those who wanted to invest a lump sum amount over Rs 2 lakh too preferred to split their investment to obtain the benefit of same day benefit.

But now to crack the whip, the Association of Mutual Funds in India (AMFI) vide a circular has told mutual fund houses that, for deciding the Net Asset Value (NAV) for amounts lower than Rs 2 lakh, they should club investments through multiple applications in debt funds by an individual or an entity, on the basis of the Permanent Account Number (PAN) of the investor for aggregation. To know more about this new and to read our view over it, please click here.

- In a move that can be a step ahead in protecting the interest of investors in mutual funds, the capital market regulator - Securities and Exchange Board of India (SEBI) has showed its desire to limit the rights of the asset managers to charge fund management fees, for which they can be eligible only if they are able to perform. This move can stop money losing mutual fund schemes from charging fees to the investors who might have already lost a portion of their money by being invested in underperforming funds. To read more about this news and to know our view over it, please click here.

- Dividend distribution tax on debt oriented mutual funds is set to go up from current 12.5% to 25% for dividend payment by a mutual fund to individuals and HUFs and all other assessee classified under similar head. This action is expected to make growth options of debt oriented funds more attractive especially for those falling under 10% and 20% tax slabs.

We are of the view that, that such a move will discourage investors to invest in hybrid funds such as Monthly Income Plans (MIPs) which is regularly announce dividend. Moreover, such funds are sought after by investors as dividends under MIPs provide them a source of regular income post retirement. These funds may lose their sheen. Also, the liquid plus funds which are near best substitute to liquid funds would also become unattractive. At present, dividend distribution tax on liquid funds is 25%. Similarly, Systematic Transfer plan (STP) would become unattractive than before.

- The Indian mutual fund industry as many of you may be aware, at present offers more than 1,500 schemes facilitating one to invest their hard earned savings in an endeavour to create wealth. But in the maze of so many schemes on offer, the task of selecting mutual fund schemes suiting your risk profile prudently, can be quite daunting when mutual fund advisors too, resort to the practice of pushing products rather than "advising" (taking into account their client needs and risk profiling).

Thus now to crack this whip, a panel constituted by the mutual fund industry lobby - Association of Mutual Funds in India (AMFI) has put forth a proposal to the capital market regulator - the Securities and Exchange Board of India (SEBI), that colour codes be applied to mutual fund products (across equity and debt schemes), which can signal the risk that product carries with it. To read more about this news and to know our view over it, please click here.

- Indiabulls Mutual Fund launched an open-ended debt scheme, named "Indiabulls Income Fund" having a mandate to invest in various debt and money market instruments and also invest in securitised debt (not exceeding 50% of the net assets of the scheme), including repo in corporate debt securities. By investing in various debt and money market securities IIF aims to generate steady returns with a low-risk strategy. As per its offer document the investment objective of the scheme is "to generate a steady stream of income and or medium to long term capital appreciation/gain through investment in fixed income securities." Hence IIF endeavours to maintain a balance between safety, liquidity and profitability aspects of various investments thereby trying to achieve an optimal risk balance while managing its portfolio.

Disclaimer: This note / article is for information purposes and Quantum Information Services Pvt. Limited (PersonalFN) is not providing any professional / investment advice through it. The recommendation service, views, articles and other contents are provided on an "As Is" basis by PersonalFN. The facts mentioned in the note are believed to be true and from a public source. The Service should not be construed to be an advertisement for solicitation for buying or selling of any scheme / financial product. PersonalFN disclaims warrants of any kind, whether express or implied, as to any matter/content contained in this note, including without limitation the implied warranties of merchantability and fitness for a particular purpose. PersonalFN and its subsidiaries / affiliates / sponsors / trustee or their officers, employees, personnel, directors will not be responsible for any direct/indirect loss or liability incurred by the user as a consequence of his or any other person on his behalf taking any investment decisions based on the contents of this note. Use of this note is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. PersonalFN does not warrant completeness or accuracy of any information published in this note. All intellectual property rights emerging from this note are and shall remain with PersonalFN. This note is for your personal use and you shall not resell, copy, or redistribute this note, or use it for any commercial purpose. Please read the terms of use.

Add Comments

| Comments |

6chp5psh@gmail.com

Jan 07, 2015

Never seen a better post! ICOCBW |

1