Every person aims to protect their hard-earned money from taxes but not everyone is able to achieve it due to lack of knowledge about effective tax planning.

Ideally, tax planning should form an integral part of one's wealth creation journey. Doing so enables you to save tax as well as helps you to achieve your set investment objective. Depending upon your financial goals, risk appetite and investment horizon, you can invest in various tax saving instruments such as Public Provident Fund, National Saving Certificate, Tax Saver Bank FD, Equity-linked Saving Scheme, etc.

Image by 8photo - www.freepik.com

Out of the instruments available for tax saving needs, Equity-linked Saving Scheme (ELSS) stands out for its dual advantage as a worthy wealth creation tool and an efficient tax saving instrument. If you invest in a worthy ELSS, you can gain much higher returns than you can probably expect from a tax saver bank fixed deposit, PPF account, NSC, or any other tax-saving schemes.

What is ELSS?

ELSS, also known as tax saving mutual funds, are diversified equity funds that come with the dual advantage of wealth-building potential and tax-saving benefits. As per SEBI's categorisation norms for mutual funds, ELSS are open-ended schemes with a statutory lock-in of 3 years and tax benefit. ELSS invests a minimum of 80% of its assets in equity & equity related instruments.

Investment in ELSS is eligible for a deduction under Section 80C of the Income Tax Act up to Rs 1.5 lakh in a financial year. Unlike other open-ended equity schemes, ELSS comes with a lock-in period of 3 years which is among the lowest as compared to other tax-saving instruments. If you invest via the systematic investment plan (SIP) route, each instalment is subject to a lock-in period of 3 years.

So, if you are looking for tax benefits along with higher return potential, but do not want to commit your money for a very long period, say 5 to 15 years or more, then ELSS is an investment option you must consider.

When compared to other popular tax-saving instruments such as tax saving FD and PPF, ELSS has the potential to reap higher returns for its investors and this is primarily why it is a worthy avenue for tax efficiency and long-term wealth creation.

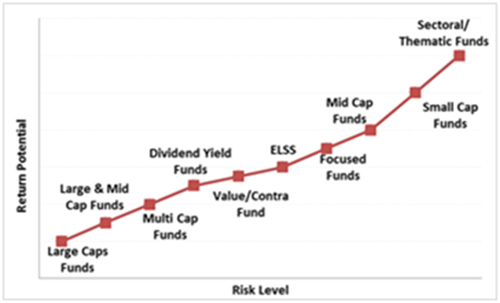

Graph: Placement of ELSS on risk-return spectrum

Note: For illustrative purpose only

(Source: PersonalFN Research)

These funds have the flexibility to invest across market capitalisation. Accordingly, most ELSS hold a diversified portfolio and are usually market cap and sector agnostic. ELSS may follow the growth style or value style of investing or a combination of both.

Since ELSS are equity-oriented scheme, the returns are not fixed and will depend on how the market performs. Therefore, ELSS is suitable for investors who can bear short-term volatility in the equity market, hold a high-risk appetite, and have an investment time horizon of at least 3 years.

Table: Performance scorecard of ELSS

Data as on February 25, 2021

(Source: ACE MF)

*Please note, this table only represents the best performing ELSS based solely on past returns and is NOT a recommendation. Mutual Fund investments are subject to market risks. Read all scheme related documents carefully. Past performance is not an indicator for future returns. The percentage returns shown are only for an indicative purpose. Speak to your investment advisor for further assistance before investing.

As seen in the table above, a number of ELSS have successfully created wealth for investors outperforming their respective benchmark indices and category average across time frames. Now, while past performance is not indicative for future returns, it displays the return potential of investing in ELSS and equity as an asset class, in general.

Best ELSS to invest in 2021:

Some of the best performing scheme based on our analysis and research at PersonalFN are Mirae Asset Tax Saver Fund, CanaraRobeco Equity Tax Saver Fund, Axis Long Term Equity Fund, Invesco India Tax Plan, and Kotak Tax Saver Scheme. These funds have proved its worth in the past on both quantitative and qualitative parameters.

Some of the other decent performers are:

A long-term investment in ELSS is a more prudent choice as compared to other fixed-income products. But as with all market-linked investments, there is a risk.

Often investors tend to give in to their behavioural biases and end up making mistakes. PersonalFN highlights some of the common mistakes made when investing in ELSS.

With a plethora of choices available in the ELSS mutual fund category, you need to analyse the fund's performance carefully before investing. Remember that under ELSS the lock-in is three years. Thus, if you decide on a not-so-worthy fund, you will have to bear the cost of underperformance for the entire period.

The performance of ELSS funds can vary wildly over the years. A top ELSS fund in one period may not necessarily be the best ELSS fund for the next period.

Here are the facets you need to look into to select the best ELSS:

Quantitative Parameters:

Analyse the fund's consistency in performance across various market periods (bull and bear market phases) compared to the benchmark and category peers. While all funds may perform well during the bull phase, an important parameter while selecting an ELSS is to determine its ability to manage the downside risk during tough market conditions.

Then determine whether the fund has rewarded its investors well for the risk they have taken using risk-reward ratios like Sharpe Ratio, Sortino Ratio, and Standard Deviation over a 3-year period.

When short listing funds for your portfolio, give preference to those funds that stand strong on risk-reward parameters.

Qualitative Parameters:

Qualitative parameters are often overlooked though they are a vital aspect in the selection process. It involves determining the quality of the portfolio and the efficiency of fund manager/house.

The fund house should have a significant performance record and must follow robust investment processes with adequate risk management systems in place.

And because the fund's performance is directly dependent on the ability of its fund manager, check the qualification and experience of the fund manager and the track record of the other schemes they manage.

Look at the fund's portfolio for how well diversified it is across stocks/sectors. Remember that a concentrated portfolio can expose you, the investor, to higher risk. Ensure that the scheme is well placed to take advantage of opportunities across market capitalisation and sectors to help it sail through adverse market conditions and reduce the impact of volatility.

Moreover, keep a tab on the churning rate of the securities in the portfolio because a high churning rate can make the portfolio prone to volatility and negatively impact the overall returns of the scheme. Analyse the portfolio's turnover ratio and expense ratio to assess how efficiently the fund controls the churning and limits the expenses.

Yes, we know that the above list is a lot for an average investor to look at. It involves number crunching and much of the data is not easily available in one place. But if you do need to narrow down on the top funds, these factors are of utmost importance.

Watch this short video on selecting mutual fund schemes:

At PersonalFN, we select and recommend mutual funds based on quantitative and qualitative parameters using our S.M.A.R.T Score Matrix:

-

S - Systems and Processes

-

M - Market Cycle Performance

-

A - Asset Management Style

-

R - Risk-Reward Ratios

-

T - Performance Track Record

The outlook for ELSS in 2021:

Tax planning should be seen as a part of financial planning exercise and not a year-end task. If you are looking to invest in ELSS for your tax saving needs, do not wait for the market conditions to turn favourable. You can opt for the SIP route to save your tax saving fund from the impact of volatility and to benefit from the power of compounding.

Bear in mind, investments in equities take time to grow and generate meaningful returns. This means that there can be short-term underperformance. As a result, you may have to hold on to your investment beyond the mandatory lock-in period.And ideally, if the ELSS you have invested in performs well, it would be sensible to stay invested even beyond the lock-in period of three years to maximise the return potential and accomplish the envisioned financial goals.

The Indian equity market seems well poised to generate meaningful returns in the long even though there could be short term fluctuations. Therefore, ELSS investment can fetch you good returns as well as serve your tax saving needs provided you have the appetite to bear market ups and downs.

Editor's note: If you are not sure which mutual fund scheme you should invest in, including the tax-saving schemes, to your investment portfolio; I suggest subscribing to PersonalFN's unbiased premium research service, FundSelect, a credible mutual fund research service with a track record of over 15 years.

As a bonus, you will also get access to PersonalFN's popular debt mutual fund service, DebtSelect.

PersonalFN's FundSelect service provides insightful and practical guidance on which mutual fund schemes to Buy, Hold, and Sell.

If you are serious about investing in a rewarding mutual fund scheme, Subscribe now!

Warm Regards,

Divya Grover

Research Analyst

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds