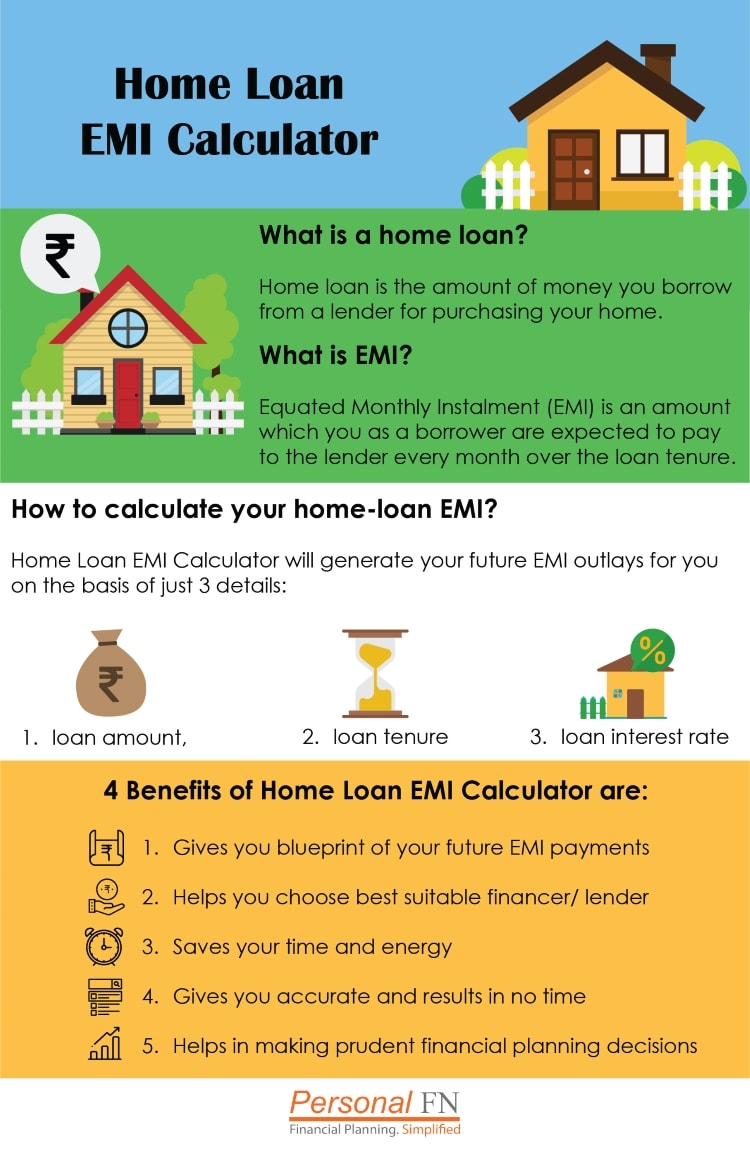

Home loan EMI Calculator is an auto tool which will make your loan planning process easier. Before you head out to the bank you can use this calculator to learn about probable home-loan EMIs.

The interest rate determines your EMI and has a bearing on your budget and long-term financial wellbeing.

Now taking a loan and paying its EMI may sound rational as you can still meet your expenses comfortably. But this is where you need to be cautious. You might be meeting your expenses today, but you also need to make sure that you would be able to do so even in future. As the life stage changes (marriage, children, retirement, etc.) expenditure patterns also change. This is where forecasting comes into picture.

So, make sure you’re availing a loan with a competitive rate of interest. It makes sense to compare interest rates across lenders.

Hence, use our home loan EMI calculator.

Formula for Calculating home loan EMI

The mathematical formula for calculating Home Loan EMI is as follows:

P = Principal loan amount;

R = Rate of interest calculated on monthly basis i.e. (R= Annual rate of interest/12/100).

For instance, if R = 8% per annum, then R= 8/12/100 = 0.0067; and

N = the number of monthly installments.

For example, if you borrow Rs 5,00,000 from a bank at 8% rate of interest for a tenure of 20 years then,

How to use Home Loan EMI Calculator?

Manual computation of EMI for different loan amounts is a little difficult and hence PersonalFN’s Home Loan EMI Calculator comes handy.

Use this simple Home Loan EMI calculator to estimate the monthly instalment payable. You can use this calculator to calculate the EMI of any loan be it—personal loans, car loans, two-wheeler loans, home loans, consumer loans etc.

This calculator generates result in a split second and enable you to understand whether the monthly payment would be affordable for you.

The 3 Step Process

- Home Loan amount (in rupees)

- Rate of interest (percentage)

- Tenure (in Months or years)

You can either use the slider or enter the loan values in the EMI calculator table. As and when you change the input values the calculator will re-calculate and display the new result.

This home loan EMI calculator will not only estimate the Equated Monthly Instalment amount but also gives you an estimate for the total loan interest payable for any particular loan amount.

The graphic and tabular presentation generated by the home loan EMI calculator makes it easier to understand the total principal and interest amount which you are supposed to pay. This will give you a clear picture about the total cash outflow you need to keep in mind before you opt for a loan.

But EMI is not the only cost which adds up while buying a home loan. Thus, we have put down all the possible hidden costs involved while opting for a home-loan.

Eligibility Criteria for a Home Loan

Lenders / banks decide how much home loan you are eligible for based on factors such as your income, repayment capacity, age, continuity of occupation, number of dependents, existing assets and liabilities, savings history, credit history, and so on.

Lenders often have slabs within which they will offer you a Home Loan of 36 / 48 / 54 times your gross monthly salary. But keep in mind, you are expected to shell out some portion of the value of property (based on the purchase agreement/deed) from your own sources of funds.

Documents required for Home Loan are:

- Income statements

- Salary slips and Form 16

- Property documents (Sale deed, agreement of sale with the builder, Land and building tax paid receipts, certified copy of the sanctioned plan of the property, possession certificate, original receipts of the advance paid for purchase, detail of estimate cost of construction, NOC (No Objection Certificate) from the housing society or builder, letter from builder/society/housing board stating their bank account details for remittances)

- Bank statements

- Latest Income-Tax Returns

- Credit report

- Age proof (birth certificate, passport, Aadhaar card, voter id, PAN card etc.)

- Address proof (Aadhaar card, passport, electricity bill, telephone bill, ration card, etc.)

- Photo identification proof (Aadhaar card, voter id, PAN card, passport, driving license, etc.)

These documents need to be submitted with the Home Loan application form along with photographs of the applicant/s. The lender will scrutinise your application, conduct due diligence, and then notify you on the Home Loan eligibility. And the processing of the Home Loan usually takes 1 or 2 weeks. Once the Home Loan is sanctioned, before disbursement, the Home Loan agreement copy will be duly signed, and a standing instruction request / ECS mandate form and security deposit cheques are to be provided.

11 hidden costs associated with a Home Loan

-

Processing Fee

This is the fee charged for processing your Home Loan. It is around 0.5% - 1% of your Home Loan amount. The percentage that is charged depends on your profile, income, and type of loan.

-

Legal Fee

Some banks and financial institutions charge this fee to scrutinise legal property documents. Some lenders might include this cost into the processing fee.

-

Technical Valuation Charges

Your lender will carefully scrutinise the property that you intend to buy. They will send an expert, could be a bank employee or an architect or an engineer, who will visit the site to ensure legality and fair value of the project. They evaluate your property on a number of criteria such as age of the building, quality of construction, etc. The technical valuation charge is an upfront payment, before sanctioning the loan.

-

Documentation Fee

Some lenders also charge documentation fee separately or under the processing fee category. This charge is for maintaining your documents such as Home Loan agreement, ECS mandate, etc. Some lenders may charge around Rs 500- 2000 towards the documentation fee.

-

Franking Fee

Franking is the process of confirming the payment of stamp duty. So, when you pay stamp duty for the sale of agreement or purchase of loan, an authorised bank or a franking agency may stamp your document to certify stamp duty payment. Franking charges differ from state to state and can be in the range of 0.1% – 0.2% of your Home Loan amount.

-

Notary Fee

If you are an NRI, then you and your Power of Attorney’s (POA) KYC details need to be notarised by the Indian Embassy or a local notary available abroad.

-

Cheque/ ECS Dishonour Charges

If at any point of time you dishonour your EMI, the lender will charge you for it. This charge may vary from Rs 250 per instalment or some percentage of your recovery amount. This will not only add to the expenses, but will also affect your credit score.

-

Loan Pre-payment Fee

When you pre-pay your Home Loan, the bank loses out on the opportunity to earn from your interest payment. Hence, to indirectly recover the cost, the bank might charge you a penalty. However, the Reserve Bank of India has abolished this charge for floating-rate Home Loans. Pre-payment charges are still applicable on fixed rate loan or loans availed under special schemes and if the payment is sourced through third party. This charge may vary from lender to lender and the type of loan as well.

-

Document Retrieval Charges

Document retrieval charges are charges levied at the time of Home Loan closure/ pre-closure of Home Loan. This is a cost for transferring your original documents from central repository to the borrower.

Your Home Loan and property documents are kept in safe custody at a central repository. Suppose you availed of a Home Loan at the bank’s branch in Pune and its central repository is at Mumbai, then the loan and property documents are kept at Mumbai. At the time of your Home Loan closure, the bank will transfer your documents from Mumbai back to Pune, and hence this document retrieval cost is charged to you.

-

Charges for Statement of Account

One annual account statement of your Home Loan account is free, but in case you need another statement then the bank might charge you upto Rs 500 for statement generation.

-

Balance Transfer/ Resale Home Loans

If you decide to transfer your balance amount of the Home Loan from one bank to another or from one Home Loan scheme to another, you will be charged with a transfer fee.

Also during the Home Loan application process, say you opted for a floating rate loan and now you want to change it to a fixed rate loan or vice-a- versa, you will be charged this fee.

Is there collateral in home loan?

Yes, Home Loan is a ‘secure loan’. The property will be mortgaged with the lender until all dues are cleared. As an additional security, some lenders also insist that buy a home loan insurance cover , plus they assess if you have an adequate life insurance cover in case of an eventuality i.e. untimely demise, so the loan does not devolve onto your dependents.

Tax benefits of home loans

The interest component of your Home Loan EMI is deductible under Section 24(b) of the Income-Tax Act, 1961, while the principal repayment can be claimed as deduction under Section 80C of the Act, subject to the conditions of the respective Sections being satisfied.

Merits of owning a real estate property

-

Real Asset

Buying a real estate property leads to creation of a physical asset since it is tangible, and it gives a feeling of security. Additionally, you might have an emotional value attached to it which other asset classes may not invoke.

-

Price Appreciation

A real Estate property provides return in the form of price appreciation and it might vary from one place to another. It has no defined rate of price appreciation and varies depending upon the accessibility to necessities of life such as school, hospital, convenience to travel, etc. The price appreciation will also depend upon the future development of the area where you might be buying it.

-

Rental Income

If you buy a house which is ready to move in, then you have an option to give it on rent. Rent can be a second source of income which you can earn from a real estate property which no other asset class can provide. The rental income may vary depending upon accessibility to necessities of life as cited above, but it is generally 2-3% p.a. of the property value. You see, rental Income can be very handy; especially after retirement as it can give you a permanent source of regular income.

-

Hedge against Inflation

Usually real estate property prices increase in line with inflation rate and over the long term, it can be considered as a good hedge against inflation. If you want to protect the real value of your hard-earned money, then you can consider investing in real estate.

-

Diversification

PersonalFN believes that you should never invest all your hard money in one asset class as it is considered risky. Therefore, investing in real estate can provide you diversification benefits, but you need to diversify wisely.

Few points to keep in mind before buying a property

While the aforementioned facets are enthralling, here are a few vital points you should keep in mind:

-

Affordability

While Home Loan schemes are available in plenty, affordability yet remains an issue. You see, as with other asset classes you can't invest small amount every month to buy a real estate property. Hence, although Home Loans are available you need to look into your affordability. After all, EMIs affects an individual's cash flow in a big way, leaving you with fewer amount after regular EMI and expenses for investment purpose for other short and long term financial goals.

-

Risk

Real estate investments are risky. Normally people who buy real estate for investment purpose prefer buying a under construction property, as it generally has higher return potential than a ready to move in property. But extra return comes with extra amount of risk as well, which you have to take in an under-construction property. Risk includes delay or default by builder to complete the project, Government / Court interference if all the construction rules are not followed while property is under construction. Hence, you need to approach real estate studying all angles.

-

Valuations

Valuation of a real estate property is not easy determined as in case of other asset classes, on account of lack of realistic price discovery. Each and every society and area will have different valuations and it will also depend upon the selling and buying power of both the parties involved.

-

Liquidity

If you are buying a property as an investment, liquidity matters. In case of real estate liquidity is very low as it takes long period of time to find a buyer, finalize it and close the deal. Liquidity means how quickly an asset can be sold. PersonalFN believes that if you are buying a house for dwelling, anytime might be a good time to invest (assuming you have assessed the affordability). But if you want to buy a house for the purpose of investment then you should take a holistic view of your portfolio.

Now that you’re aware of all the facets, go ahead and make an informed decision while availing a Home Loan.

PersonalFN believes that one may have EMI-to-income ratio of about 40% of the total household income. And hence you should opt for a home loan which fits well within your budget.