Home >

guide > Mutual Fund Direct Plans - Everything You Need To Know

Mutual Fund Direct Plans - Everything You Need To Know

While you shop, you may always be on the look-out for discounts. After all everybody wants to save costs. But when it comes to mutual fund investing, retail investors seem to be reluctant to do so. Lower participation in direct plans offered by mutual funds, especially in the equity category, suggests that investors still prefer the conventional route of "going through distributors" to invest in mutual funds.

For your information, today, when you invest in mutual funds you have two plans: Mutual Fund Regular Plan and Mutual Fund Direct Plan.

In this guide we cover everything that you need to know about direct mutual fund. Let's get started:

#1 What Is A Mutual Fund Direct Plan?

Direct mutual fund plans were introduced by the Securities and Exchange Board of India (SEBI) in January 2013. It made mandatory for all mutual fund houses to launch ‘Direct Plans’ for all schemes.

With direct mutual fund you eliminate the middle man. And directly route your money into mutual funds. There is no guidance of the advisor/ agent. You do your own research or bank on external research reports.

The transactions can be performed online or even physically by visiting the registrar’s or the asset management company’s office. And since, transactions are routed directly; no commissions are paid by the fund house on the money you invest. Hence, the expense ratio for a Direct Plan is lower as compared to Regular Plan.

Regular Plan on the other hand is the conventional kind of plan, where you invest/transact through a mutual fund distributor / agent / relationship manager. You are guided by this middleman and he performs all the operational tasks for you.

Fund house pays commission on the money you invest to distributors / relationship managers. Due to this distribution cost you incur a higher expenses ratio in a regular plan.

Fund house pays commission on the money you invest to distributors / relationship managers. Due to this distribution cost you incur a higher expenses ratio in a regular plan.

Rationale behind direct mutual fund

Well, the idea was to cut off the long chain of distributors and agents which always adds to the cost structure of the fund houses.

In return, the mutual fund houses would pass on these cost savings to the investors in the form of the lower expense ratio.

The expense ratio tells you how much as a percentage of the scheme's corpus the total expenditures are. This in turn was considered to enhance the returns for the investors.

But why do investors hesitate to invest in direct plans?

Strongest reason is the lack of awareness and inadequate investor education. Further many prefer a broker to execute their transactions and render advice. Hence, many are still away from mutual fund direct plans.

While many ignore the small difference of expense ratio between regular and direct plan. In the long run this gap cannot be ignored.

Really, does it make a difference?

Ye, it does!

We at PersonalFN studied expense structure of diversified mutual fund schemes whereby it found that, on an average, direct plans save about 0.60% of cost per year. This may not sound good enough for you to switch from standard plans to direct ones. But if one has a long-time horizon in mind, say 10 years, it may save you good deal of money.

For example, if you invest Rs 10,000 per month through Systematic Investment Plan (SIP)in a mutual fund for 10 years through direct plans and assuming mutual funds generate 15% returns on compounded annualised basis, you may save about Rs 70,000. Those opting for lump-sum investments may save around Rs 2, 50,000 over 10 years.

Use PersonalFN's Mutual Fund Calculator and SIP Calculator before you make any investment decision.

Now let's dig in deeper to understand the difference between direct and regular mutual fund plan.

#2 Direct v/s Regular Mutual Fund

Direct v/s. Regular Mutual Fund

Direct v/s. Regular Mutual Fund

|

Regular Plan

|

Direct Plan

|

|

You transact through mutual fund distributor/ investment advisor/ relationship manager

|

You directly invest either physically or online visiting registrar's or mutual fund company's office

|

|

The recommendation is guided by the mutual fund distributor/ investment advisor/ relationship manager, and there is after sales support service

|

There’s no guidance. You do your own research to invest or rely on independent research reports

|

|

Indirectly commission is paid by the fund house on the money you invest

|

Since you invest directly, no commission is paid by the fund house on the money you invest

|

|

You incur a higher expenses ratio (due to the distributional cost involved)

|

The expense ratio is lower as there is no commission to be paid to the distributor

|

Hence, the biggest difference between direct and regular plan is measured in terms of cost.

One of the advantages of a Direct Plan is you circumvent the rampant mis-selling that goes on to earn commissions. You will agree that today the scenario is at odds. It’s rare to find a ‘financial guardian’ whom you can trust for sound advice on investing and wealth creation.

There are only a few who render a financial advice diligently and ethically. This is precisely why inflows under Direct Plans are witnessing a steady rise, especially from cities such as Delhi, Mumbai, Chennai, Bangalore, Pune, and Chandigarh.

Although direct mutual funds remain popular among genuine investment advisors, individual investors have found little merit in them so far, at least going by numbers. Some investors are unaware of benefits while others tend to be ignoring resolutely.

It has been observed that, equity oriented funds, which have highest participation of retail investors, have low proportion of total assets (around 12%) in direct plans.

Whereas in debt funds the proportion of direct plans of the total assets is upto 53%. This means retail investors have been hesitant to take up the direct route in equity-oriented funds.

While investing in direct mutual fund you must do all the documentation and research tasks by yourself. Here you forgo the facility of doorstep service that many middlemen offer which you might find inconvenient while opting for direct mutual fund plans.

But do you know that, if you plan to invest in mutual funds through the direct route, you can complete your C-KYC through five simple steps.

KYC is a prerequisite for investing in mutual funds(and almost all financial instruments). It is vital compliance on the part of financial product manufacturers, to know their investors better.

Also read: 5 Easy Steps To Become KYC Compliant

#3 Why Invest In Direct Mutual Fund

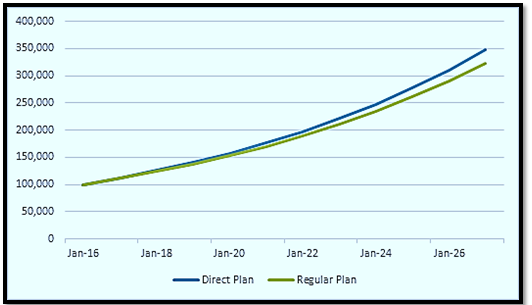

Both the plans have identical underlying portfolio, fund manager and follow same investment strategy. But a lower expense ratio for a ‘direct plan’, enables in clocking better returns than a regular plan. You might feel that the difference in their expense ratio is mere 1%; but in the long-run the returns generated by ‘direct plans’ are higher. Take a look at the chart here...

In the above illustration, assuming Fund A generates 12% CAGR and you invested Rs 1,00,000 in ‘direct plan’ its value after 10 years would be Rs 3,47,855. Whereas if invested in regular would be Rs 3,23,073.

Regular vs direct plan makes a difference of good +7.7% in the power of compounding. Although the difference in returns may appear small in the near-term, over the long-term the difference is worthy and cannot be ignored.

Hence, direct mutual fund plans make a positive difference to your investments every year. The direct plans generate roughly 0.5% to 1.0% additional returns every year. However, if you sow seeds of these small savings, you may harvest rich rewards over 15- 20 years — thanks to the power of compounding.

(Use PersonalFN’s Mutual Fund Calculator to know the future value of your mutual fund investment.)

Now that you know a lot about direct mutual fund plans let’s head on to know how to invest in direct plans in the next chapter…

#4 How To Invest In Direct Mutual Funds

If you decide to invest in mutual funds directly, here are the different paths:

-

Asset Management Company

Once you have decided in which fund to invest, you can visit the nearest AMC office or its website to invest in the mutual fund. You could invest in mutual fund schemes directly through the online portal of the Asset Management Company.

For instance, if you wish to invest in Fund A, you can go its fund house website and buy fund units online.

However, if you have multiple funds, register and invest in each fund house individually. Of course, this is an inconvenience if you choose to have a number of schemes from different fund houses. So, choose your investments with due diligence

-

Registrar & Transfer Agent (R&TA)

The registrars also facilitate online investing in mutual funds, however, the investment will be limited to the mutual funds registered with them.

The registrars also facilitate online investing in mutual funds, however, the investment will be limited to the mutual funds enrolled with them.

You can either visit the CAMS or Karvy website and invest in schemes of your wish.

-

Mutual Fund Utilities

Mutual fund transaction portal, MFU (Mutual Fund Utilities) is a single window for you to transact across mutual fund schemes.

Mutual Fund Utilities is a shared platform of different fund houses. You need to create an account first, before transacting and you can transact in mutual funds of almost all the AMCs. Using a Common Transaction Form (CTF) or through the online portal you can invest in multiple funds of different fund houses.

Moreover, there is no additional charge for mutual fund investments made through this portal. The cost of the platform is shared by the participating fund houses.

-

Robo-Adviser

Robo-advisers are digital advisers that provide portfolio management and financial planning services online, without any human intervention. These types of advisers are usually more affordable than human advisers to all classes (of investors). The advantage with robo-advisers is zero human bias in the advice, but there could be few limitations to the way information is sought without human intervention.

A robo-adviser can offer you a world of convenience, thanks to the advancement in technology. Opt for a specialised robo-advisory service that will ensure your financial well-being through mutual funds—one that proves to be worth more than it costs.

Opt for robo-advisers who are genuinely concerned about your long-term financial well-being. Be careful of not investing your hard-earned money through fly-by-night operators.

And select a robo-adviser backed by established companies in the financial services space. Check if their investment recommendations are fully supported by their sound and ethical research processes. They should be fee-based to ensure that the commissions they earn do not influence their advice.

With a 24x7-service window, robo-advisers are the future of financial planning and investments in a time-strapped world.

As an investor you should remain focussed on their long-term financial goals and invest in the right mutual funds to fulfil these goals. The basics of investing in mutual fund schemes remain the same.

Are direct plans suitable for first time investors?

If you are a naïve mutual fund investor you can still invest in direct mutual fund to meet your financial goals.

So, if you are a diligent investor, and have fair knowledge about of how to select mutual fund schemes, you may consider investing in ‘direct plans’.

But don’t ignore monitoring the funds and rebalancing the portfolio when needed. If you can do this, you don’t require a mutual fund distributor / investment advisor.

On the other hand, if you are an alien to mutual fund space but want to explore the potential of wealth creation, you might as well seek guidance of a ‘Certified Financial Planner’ who provides sound financial planning services.

We at PersonalFN, are committed to provide you unbiased and honest views and opinions on various personal finance issues that can impact your investments and finances. We have been providing personalized Financial Planning solutions to our clients residing in India as well as abroad (NRIs) so as to help them meet their financial goals and objectives.

Through our Financial Planning Service, you get a holistic Financial Plan that takes into account your current financial position and tells you how to get to where you want to be with all of your financial goals.

Once your Plan is created, we can even assist you with the implementation of your plan and monitor the execution of your investments through our Wealth Planning Service. With this Service, you can choose to receive a Financial Plan for single or multiple financial goals.

You can also choose to avail only a review of your investments (mutual fund and insurance portfolio).

While you’re selecting a ‘financial guardian’ ensure you take enough care. Judge his/her financial knowledge and credibility and be rest assured that you aren’t in wrong hands.

A ‘financial guardian’ will help you build a portfolio recognising your risk appetite, investment objectives, investment horizon and financial goals. He will help you manage your hard-earned money with as much care as he manages his own.

#5 Best Direct Plans

Many a times our readers have this question “Which are the best direct mutual funds”

And the answer to it is: “None!”

Yes, you read it correct. Direct Plans are just a mode investing in mutual funds.

You need to learn the art of selecting winning mutual funds to build wealth. There are no best direct plans but you can have best mutual funds to select from the galaxy of options available.

To Conclude

But many investors find this job very tedious and time-consuming. If this has been your reason for not investing, it's time you re-examine. Many platforms offer you ready tools to compare funds just at a click and control of the mouse.

Alternatively, you can always seek help of an independent mutual fund advisor who offers an unbiased research-based view for a fee, and you're always free to invest in a direct plan. For your long-term financial wellbeing, it is essential that you review your portfolio so that corrective measures can be taken at the right time.

The time has come to ask yourself and judge: Are you compromising on long-term returns for a little comfort in the short-term by availing services of mutual fund distributors or is there a real value.

Besides, there's PersonalFN to your help, who can power your investment decisions with unbiased research recommendations on mutual funds. PersonalFN follows a rigorous research process to help you, investors, select the best mutual fund schemes for your investment portfolio.

PersonalFN has put together a research report on potentially the best mutual fund SIPs for your long-term portfolio — The Super Investment Portfolio – For SIP Investors. Under this, we conduct a detailed analysis on how SIPs in the top shortlisted mutual fund schemes have performed, across multiple market conditions and timeframes. Only those funds that successfully pass this evaluation are chosen.

Don't miss out on early bird discounts. Subscribe to the report here

If you are an investor looking for readymade solutions, you can opt for PersonalFN's FundSelect Plus, a comprehensive portfolio service to benefit from SEVEN time-tested, readymade equity and debt mutual fund portfolios.

Based on your risk profile and investment horizon, you can choose from three equity portfolios and three debt portfolios. In addition, you get a readymade tax-saving portfolio as well. This service has a decade-long market-beating track record.

You cannot afford to miss this offer available, subscribe now 😊

Direct plans vs. Regular Plans – which of the two you prefer and why while investing in mutual funds? Share your view us below or on social media. We would be happy to hear from you 😊

Happy Investing 😊

<