8 Guaranteed Ways to Improve Your Credit Score

Listen to 8 Guaranteed Ways to Improve Your Credit Score

00:00

00:00

A Credit Score is a number ranging from 300 to 900 that indicates an individual's creditworthiness. In simple words, it shows the consumer's ability to repay a loan. In India, there are four credit bureaus that calculate the credit scores, which are largely used by lenders across the country. For approving or rejecting the loans, lenders, like banks and Non-Banking Financial Corporations (NBFCs), heavily rely on these credit reports to check the applicant's creditworthiness.

It is advisable to improve/maintain your credit score since it is the primary factor that influences your loan or credit card application approval. Today's article will elucidate what a credit score is, how it is calculated, the benefits of having a good credit score, and how you can improve and/or maintain your credit score.

What is a Credit Score?

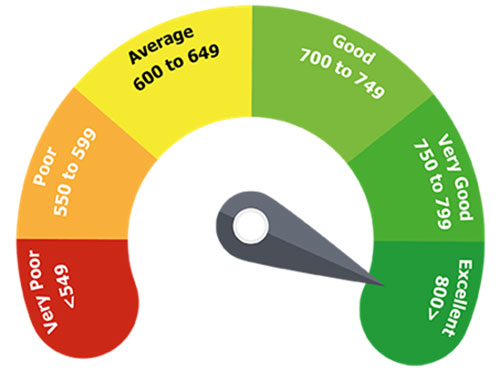

As we discussed, a credit score is a three-digit number ranging from 300 to 900 that depicts an individual's loan repayment capacity. Out of many factors that banks and NBFCs consider while approving or rejecting your loan application, your credit score is the major factor since it gives lenders an idea about your creditworthiness. The higher the credit score, the more banks and NBFCs will be interested in granting you a loan because a higher score indicates a lower probability of a loan default. Therefore, a higher credit score is the key to loan approval, whereas a lower credit score reduces the chances of getting a loan.

The Credit Score Indicator below can help you understand the different ranges of credit scores:

Who calculates the Credit Score?

In India, we have four credit bureaus that calculate credit scores:

-

TransUnion CIBIL

-

Equifax

-

Experian

-

CRIF High Mark

The primary purpose of these bureaus is to rate an individual or a business entity after collecting and analysing their respective credits data and repayment history. Banks and NBFCs across the country largely use the CIBIL score from TransUnion Credit Information Bureau (India) Limited (CIBIL).

What factors influence your Credit Score?

Your credit score is calculated based on a point system that involves several factors. We have explained the major influencing factors below:

1. Repayment history:

Your credit repayment history is a significant factor influencing your credit score. This is because the credit bureaus keep track of the Economic Monthly Instalments (EMIs) you pay towards your debt, your credit card bill payments, and other credit repayments. So, when you or the lender requests a credit bureau for your credit score, generally, your credit history of the last few years is considered to calculate your credit score.

2. Credit Utilisation Ratio:

Credit Utilisation Ratio (CUR) is another crucial factor that influences your credit score considerably. Basically, it is the percentage of credit you have utilised against your available credit limit. So, you can calculate your CUR by dividing your entire outstanding debt balance by your total credit limit. The more you use your credit card, the lower your credit utilisation ratio will be until you clear your debt. Therefore, it is advisable to utilise up to 30% of your total credit limit. If you have higher expenses, using multiple credit cards can help reduce the CUR.

3. Credit history:

The age of your credit has a medium impact on your credit score. Having a good credit history over years helps increase your credit score by a few points. For lenders, offering a loan to a borrower/consumer with a long repayment history is less risky than providing a loan to anyone without a significant repayment history. Moreover, if you have a borrowing history of less than six months or do not have a borrowing history at all, the credit bureaus give you a credit score of 0 to -1.

4. Number of credit accounts:

The number of credit accounts active in your name is a low impact factor that affects your credit score. However, if you are able to manage multiple loans with good credit repayment history, your credit score can increase by a few points. Also, having multiple types of loans, such as secured and unsecured loans, can positively impact your credit score. Therefore, your total debt should be a balanced credit mix.

5. Number of credit score inquiries:

The number of times you or the lenders inquire about your credit score also impacts your credit score. Therefore, it is advisable not to apply with multiple lenders in a short duration to limit your credit score inquiries. In addition, the number of rejections that come with multiple applications can also harm your credit score.

(Image Source: www.freepik.com)

(Image Source: www.freepik.com)

What are the benefits of having a good credit score?

1. Faster approval of loan applications:

Lenders consider a consumer's profile to be low-risk if you have a good to excellent credit score, which ultimately leads to a faster approval of your loan application. Whereas, if your credit score is not up to the mark, the lenders will have to consider other factors to analyse the risk in your profile, which can delay the loan process. Also, if you have an excellent credit score, your chances of getting pre-approved and instant loan offers increase.

2. Credit card offers:

Credit cards offer various benefits, such as No Cost EMIs, discounts, rewards points, etc. Banks and credit card companies check if you have a good credit score before they offer you any credit card/s. A good credit score proves that you have been paying your dues timely and gives lenders the confidence to offer you credit cards with higher credit limits.

3. Concessions:

Lenders are more interested in offering loans to individuals with high credit scores since they know the chances of loan repayment default are likely to be fewer. Therefore, to attract such individuals, the lenders offer a lower rate of interest and discount in processing fees.

How can you improve your credit score?

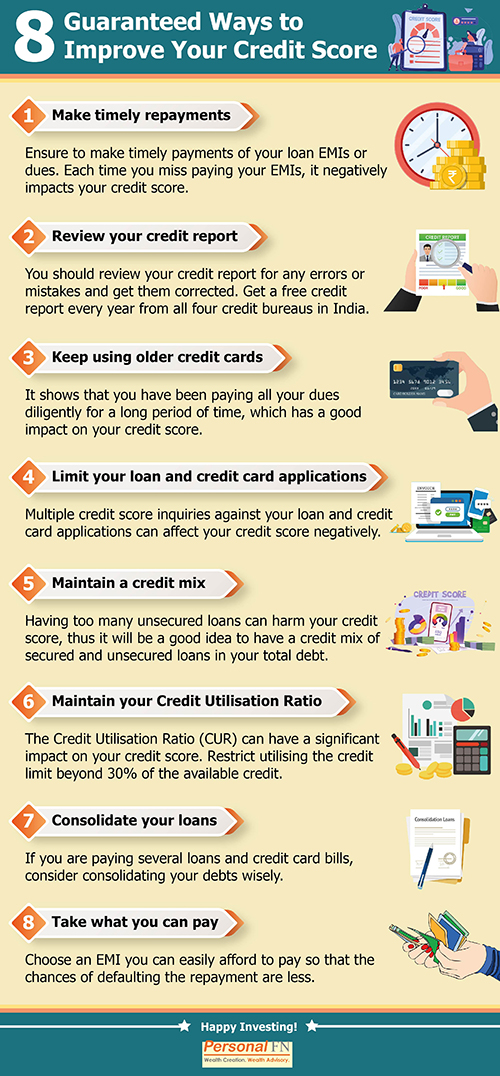

1. Make timely repayments:

Since credit bureaus keep track of your monthly repayments of EMIs and credit cards bills, it is necessary to pay your dues on time to maintain and improve your credit score. This is the simplest yet most beneficial thing you can do to improve your credit score. However, each time you miss to pay your EMI, it gets recorded in your credit history, which negatively impacts your credit score.

2. Review your credit report:

Reviewing your credit report every year is an excellent practice to follow. You can get a free credit report every year from all four credit bureaus. You should review and check for any errors or mistakes and get them corrected. Moreover, you should use these reports to check if you are using credits in the right way. For example, if you see your credit score has decreased due to the overuse of credit card limits, be careful with credit card usage in the future to improve your score.

3. Keep using older credit cards:

Using older credit cards helps increase the age of your credit, which is another important factor that has a high impact on your credit score. It shows that you have been paying all your dues diligently for a long period of time. However, if you have new credit cards with higher benefits and using the old credit cards is not affordable anymore, make sure to close your older credit card accounts properly.

4. Limit your loan and credit card applications:

When you apply for a new loan or a credit card, the lender inquires about your credit score with credit bureaus. As we discussed, multiple credit score inquiries in a short period can affect your credit score. Moreover when lenders reject your applications due to poor credit scores, it can also harm your credit score. Therefore, check and compare all the details of any loan offered by various banks and NBFCs, check if you match their eligibility criteria, and choose one or two lenders that suit your requirements. This practice may need more time initially, but it will help limit your credit score inquiries, ultimately improving your credit score.

5. Maintain a Credit Mix:

It is essential to have a good mix of secured and unsecured loans in your total debt. Having maximum unsecured loans can harm your credit score. Therefore, it is advisable to balance both types of loans. However, if you do not have any credit history, you can start with any kind of loan.

6. Maintain your Credit Utilisation Ratio:

As we have already discussed, the Credit Utilisation Ratio (CUR) can have a significant impact on your credit score. Therefore, you should always pay your credit card bills in full. If it is not possible, restrict utilising the credit limit beyond 30% of the available credit. If you need to use higher credit limit, request your credit card provider to enhance your credit card limit. You can also try to get another credit card, enhancing your total credit card limit.

7. Consolidate your loans:

If you are paying several loans and credit card bills, it is good to consolidate them. First, you should clear off the possible loans. If clearing off the loans is not financially manageable, you can take a debt consolidation loan from a bank. This will help you clear off the existing loans and you will have only one loan to repay. If you have a single running loan, try to clear it first before taking another similar loan.

8. Take what you can pay:

The best practice to maintain and/or improve your credit score is to choose an EMI you can easily afford to pay so that the chances of defaulting the repayment are less. Also, you should not unnecessarily opt for a loan amount higher than you require simply because the lender is offering a higher amount.

The Bottom Line:

A credit score plays a vital role in approving your loan or credit card application. Although the tips given above will help you maintain and/or improve your credit score, you cannot expect it to completely change your credit score overnight. However, if you follow these tips regularly and have patience, you will eventually see a positive result in your credit score. If you want to see the results soon, start practising these tips the earliest.

Warm Regards,

Ketki Jadhav

Content Writer

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds