Here's How to Make a SMART Financial Plan to Buy a Car Instead of Taking a Car Loan

Ketki Jadhav

Jan 17, 2023 / Reading Time: Approx. 12 mins

Listen to Here's How to Make a SMART Financial Plan to Buy a Car Instead of Taking a Car Loan

00:00

00:00

A common man has to face a huge problem when travelling by public transport during peak hours. In a crowded city like Mumbai, even expecting a place to stand on a local train or bus could be a lot to ask for. Furthermore, the water clogging the rail tracks during the rainy season can even cause a delay in commuting. Apart from these public transport issues, many frequent travellers avoid taking taxis and rickshaws due to the lack of transparency in pricing and the arrogance of the taxi and rickshaw drivers.

Having your own car solves most of these issues. That's why a car is the next big purchase most of us would like to make after a house. However, most car buyers choose to go a little out of their budget when it comes to buying a new car because they consider it an asset they usually buy only once or twice in their lifetime. That is why financing a car by taking a car loan has become a very common practice worldwide.

When we categorise loans as good loans or bad loans, certain types of loans like home loans and education loans are considered good loans as they help you achieve your goals faster and manage funds better. Whereas loans like personal loans and credit card spending are considered bad loans as they make you spend more than your capacity and create a debt trap. However, a car loan is quite a grey area as driving a car is a necessity for some individuals, whereas others buy it because it gives them a sense of achievement or due to sheer peer pressure.

While some of us prefer buying a car in cash, i.e. by saving a sufficient amount for it over a period, others cannot wait to get their hands on the new steering and hence opt for a car loan. This article elucidates the pros and cons of availing of a car loan, the alternative to owning a car, how delaying the purchase and making a financial plan can help you save a substantial amount, and a simple yet efficient way to make a financial plan and choose the best mutual funds to buy your dream car.

Buying a car with a car loan:

Buying a car with a finance option, i.e. with a car loan, has many benefits:

-

Instant Possession:

When buying a car with a loan, you do not have to wait until you save up the required amount. Generally, banks and NBFCs finance up to 85% to 90% of the on-road price of the car. However, some leading banks can offer 100% financing based on the car model, your repayment capacity, and your credit profile. Besides, with the availability of options like pre-approved car loans, you can get the loan amount disbursed within 24 hours to 48 hours.

-

More Choices:

Since a car loan allows you to go out of your budget with affordable monthly instalments, you get more options to choose the car model. You can get a high-end model of your desired car, which otherwise could be unaffordable.

-

Ensures no disturbance to your other goals:

You do not have to liquidate the investments made for other financial goals, such as retirement, a child's wedding, etc. or sell your existing assets to buy your dream car.

While the benefits of car loan are alluring, it also has certain disadvantages:

-

You pay much more than the actual cost of the car:

When applying for a car loan, the lender shows you how affordable your monthly instalment, i.e. EMI, will be. However, the car loan interest rate varies from lender to lender and currently ranges between 8% p.a to 10% p.a. Considering the loan amount and loan tenure, the car loan interest rate can significantly increase the cost of your loan.

Apart from the interest rate, charges like processing fees, documentation charges, GST, prepayment charges, foreclosure charges, etc., can impact the overall cost of your car loan.

-

Your car is Hypothecated:

A car loan is a secured loan because it is backed up by the car you purchase with the loan. Therefore, your car is hypothecated to the lender until the last EMI is paid. So, in case you default on the car loan repayment, the lender holds the right to seize/repossess your car to recover the unpaid dues.

Here's an example of how much a car loan costs you:

Suppose you are buying a car worth Rs 12 lakhs with 100% financing for 7 years tenure at the interest rate of 8.5% p.a. In this case, your monthly EMI will be Rs 19,004. While the EMI may look affordable, your total interest outgo comes to Rs 3,96,318, and the total payable amount goes to Rs 15,96,318 (apart from the processing fee and other charges).

| The cost of a Car Loan for 3 years, 5 years, and 7 years of loan tenure |

| Loan Amount |

12 lakhs |

12 lakhs |

12 lakhs |

| Interest Rate (p.a.) |

8.5% |

8.5% |

8.5% |

| Loan Tenure |

3 years |

5 years |

7 years |

| EMI |

37,881 |

24,620 |

19,004 |

| Total Interest Outgo |

1,63,718 |

2,77,190 |

3,96,318 |

Total Payable Amount (does not include processing fee,

documentation charges, GST, etc.) |

13,63,718 |

14,77,190 |

15,96,318 |

(Source: PersonalFN Research)

Apart from the interest, there will also be other costs, such as processing fees, documentation charges, CIBIL charges, GST, etc. These charges may vary from lender to lender and can make a considerable difference in the final total payable amount.

Is buying a car with a car loan worth it?

Due to the lack of comfort in public transport and a need to keep a safe distance due to the threat of the emergence of Covid-19 variants, public transport is not the safest transport, and hence there has been an increase in the demand for cars. However, one should note that while safe transportation is necessary for a happy and healthy life, not creating financial stress is equally necessary.

Today, cab-availing services like Ola and Uber have reached most cities and towns across the country and have proved to be a cost-effective alternative to owning a car for short-distance travellers.

Image source: www.freepik.com

Image source: www.freepik.com

Join Now: PersonalFN is now on Telegram. Join FREE Today to get 'Daily Wealth Letter' and Exclusive Updates on Mutual Funds

Here are the key benefits of availing of cab services over owning a car with a car loan:

-

There is no burden of down payment and EMIs with cab services.

-

With a steep rise in petrol and diesel prices, the fuel cost can be an additional financial burden if you own a car.

-

Opting for cab-availing services can save your yearly costs of car maintenance, the salary of a car driver, and car insurance.

-

In case of an accident, the repair and replacement cost can be an out-of-pocket expense if the insurance claim gets rejected.

-

With 5 to 7 years of loan tenure, you pay approximately 20% to 30% extra amount than the actual cost of your car. And, by the time you pay off your EMIs and close your loan, the market value of the car substantially decreases due to the car depreciation.

However, if you frequently travel a medium or long distance, opting for cab services might not be the best solution. With cab services, there can sometimes be issues like the non-availability of the cab, ride cancellation by the driver, price surges in peak hours, etc. Also, if you prefer comfort over cost, there is no better alternative to owning a car. However, since a car loan significantly increases the cost of your vehicle, it does not make sense to avail of a car loan. In such a scenario, delaying your loan-based purchase and making a solid financial plan to achieve your goal is advisable.

Buying a car with savings or financial plan:

While buying a car with a car loan could be luring, considering its many benefits, buying it in cash or with a robust financial plan can prove to be a smarter choice in the long run.

Here are the benefits of buying a car with a financial plan:

-

Simple Process:

When you buy a car without a car loan, you do not have to spend time researching the right lender, checking their terms and conditions, arranging documents, applying for the loan, waiting for disbursal, etc. You simply choose the car, pay the amount, and get the car.

-

No Additional Cost:

As the above example shows, taking a car loan involves several costs like interest and processing fees. However, a car is a depreciating asset and hence it is best to keep the cost minimum. Buying a car with savings helps keep the total cost as low as possible. Besides, some dealers may also offer an additional discount for buying a car in cash.

-

No Burden of EMIs:

Like any other loan, a car loan is a long-term commitment. Since most borrowers choose a 3 to 7 years long loan tenure, the EMIs become a fixed expense for them until they pay off the entire loan amount. In case they face any financial difficulty in the future, repaying the EMIs can be burdensome and create stress.

-

No Restrictions from the Lender:

Lenders can have several criteria when offering a loan, such as a car model for which a car loan can be taken, in whose name the car can be purchased, etc. However, when you buy a car in cash, there are no such restrictions. So, you can buy any model in any family member's name.

The only drawback of not opting for a car loan and getting a car with a financial plan is that you cannot get access to the car immediately. While getting your hands on a brand-new car without dropping any money immediately seems alluring, delaying the purchase and buying it with a solid financial plan is always a smarter choice that saves a substantial amount of money and does not create any financial burden on you.

Here's how you can make a financial plan or invest your money to buy your dream car:

When making a financial plan for a specific goal, in this case, buying a car, asset allocation, i.e. choosing the suitable investment avenues, is crucial. The time in hand and your risk profile largely decide how your asset allocation should be like.

As you might be aware, risk and returns go hand in hand. So, for every return you seek, there is a certain level of risk associated with it. Each asset class, such as equity, debt, gold, real estate, or the category of scheme you choose, comes with a certain level of risk reward.

(Source: PersonalFN Research)

(Source: PersonalFN Research)

As you can see in the pyramid, large-cap funds are relatively stable and carry lower risk compared to the mid-cap and small-cap fund categories. However, at the same time, it sacrifices the return potential. Similarly, debt instruments and fixed-income products carry low risk, whereas equity and equity-related instruments are at the higher end of the risk-return spectrum. That said, the high risk does not guarantee high returns.

Therefore, you should never invest imprudently going by just returns and must be mindful of the risk involved. On the other hand, while fixed-income products like bank fixed deposits carry low risk, it does not make sense to put all your money in such investment avenues for a very long term, as they might fail to generate inflation-beating returns. However, you can consider allocating a small portion of your investment to safer instruments to diversify your risk.

Since different financial instruments require different investment horizons, investment amounts, target amounts, etc., it does not make sense to apply a single investment strategy to all your goals. Investing in carefully selected rewarding mutual funds can help you yield inflation-beating returns and achieve your objectives within a target date.

When you choose the best mutual funds for your specific goals, it is important to analyse several qualitative and quantitative factors. The qualitative factors include portfolio quality, fund manager's experience, fund manager's investment style, fund-to-fund manager ratio, turnover ratio, portfolio ratios and concentration, investment system and the processes at the fund house, asset under management, and so on, whereas quantitative factors include the past performance of the scheme and risk-adjusted returns, among others.

Apart from these qualitative and quantitative factors, you should also consider personal factors, viz., your risk profile, time horizon, and investment objective.

Similar to the different asset classes, each mutual fund category has a distinct place on the risk-reward spectrum.

However, at PersonalFN, we understand that not everyone can be a financial expert, and you may need assistance to make the financial plan to achieve your S.M.A.R.T. goals. Therefore, we are committed to providing you with unbiased and honest views and opinions on various personal finance issues that can impact your investments and finances. We have been providing personalised Financial Planning solutions to our clients in India and to NRIs to help them meet their financial goals and objectives.

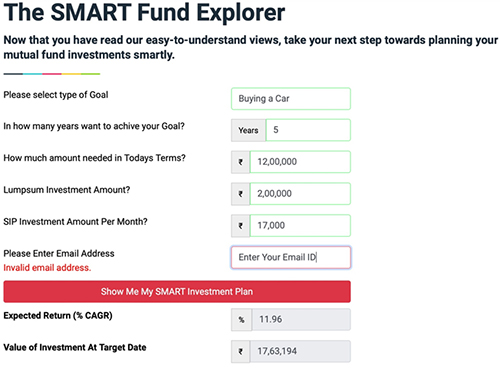

To help you make your mutual fund investments simpler yet more efficient, we at PesonalFN, have introduced the SMART Fund Explorer, which you can use to plan your mutual fund investments smartly with a mix of lump sum and SIP investments. You can simply provide details like the type of goal, time to a goal, the amount needed in today's terms, lump sum investment, and SIP investment. As you submit these details along with your email id, the SMART Fund Explorer will provide you with a decent expected rate of return on the investment and the value of an investment at the target date, considering the details provided by you.

Let us continue with the above example. Suppose, instead of opting for a car loan, you decide to postpone your purchase by 5 years and invest Rs 2,00,000 in a lump sum and Rs 17,000 p.m. towards the SIP mode of investment.

Here's how the PersonalFN's SMART Fund Explorer will look once you provide the details:

(Source: PersonalFN SMART Fund Explorer)

(Source: PersonalFN SMART Fund Explorer)

The SMART Fund Explorer calculates the Value of Investment At Target Date considering the 8% inflation rate.

As you scroll down, the explorer will offer you two mutual fund investment options (A and B) that you can choose based on your risk appetite.

Depending upon the target value, target date, lump sum & SIP investment amount, the SMART Fund Explorer will prepare two smart investment options for you, which you can choose from based on your risk appetite and get instant access to the list of the best suitable mutual fund schemes as per your selected plan by enrolling on PersonalFN's SMART Fund Explorer.

To conclude:

As discussed earlier, while owning a car gives a sense of owning a property, a car is a depreciating asset that loses its value over time. If you are not going to use the car for medium to long distances very often and do not want to spend a huge amount on the depreciating asset, availing of cab services could be the best option for you. Take note that if you opt for a car loan with a 5 to 7 years loan tenure, by the time you repay the loan and own the vehicle completely, it may get significantly depreciated, and you may outgrow it.

If you can wait for a few more years to get your hands on the brand new car, making a solid financial plan and investing in the carefully selected best mutual funds can prove to be a smart way that helps you save a substantial amount and manage your finances better. In case you cannot delay your purchase until you save the required amount, it is best to make the maximum down payment and minimise the loan tenure, which will ultimately reduce your debt burden.

KETKI JADHAV is a Content Writer at PersonalFN since August 2021. She is an MBA (Finance) and has over seven years of experience in Retail Banking. Ketki specialises in covering articles around banking, insurance, personal finance, and mutual funds and has been doing it for over three years now.