Interest Rates for Small Savings Schemes Hiked Again! Here’s All You Need to Know

Mitali Dhoke

Jan 03, 2023 / Reading Time: Approx. 6 mins

Listen to Interest Rates for Small Savings Schemes Hiked Again! Here’s All You Need to Know

00:00

00:00

Most individuals invest in some kind of small savings scheme to create wealth. The purpose of the central government-backed Small Savings Schemes is to encourage all citizens, regardless of age, to save regularly. These schemes come with a sovereign guarantee, tax benefits, and returns that are typically higher than bank fixed deposits with less risk and volatility.

The small savings schemes can be grouped under 3 categories as below:

-

Post Office Deposit - It includes savings, recurring, and time deposits with 1, 2, 3, and 5-year maturities and the monthly income account.

-

Savings Certificates - These are the two investment options; National Savings Certificate (NSC) and Kisan Vikas Patra (KVP)

-

Social Security Schemes -This includes Public Provident Fund (PPF), Senior Citizens Savings Scheme (SCSS), and the Sukanya Samriddhi Yojana.

Amidst the spiralling inflation and rising policy rates by RBI to curb the inflation, banks have increased both lending as well as deposit rates. As a result, many investors anticipated that the Government will increase the interest rates of small saving schemes.

How are the interest rates set for Small Savings Schemes?

Before deciding on the interest rates of small savings schemes, the government will keep an eye on the nation's inflation and liquidity situation. The government announces interest rates for small savings plans on a quarterly basis. The method to calculate interest rates for small savings schemes has been provided by the Shyamala Gopinath Committee. The committee had recommended that the interest rates of various schemes be 25 to 100 basis points higher than the yields of similar maturity government bonds.

Given the rising rates on government bonds, the most recent interest rate increase was anticipated. Small savings rates are based on yields on bonds with the same duration and are updated every three months. Bond yields decreased steadily in 2020-21. Small Savings Schemes saw a sharp 60-70 basis point rate drop that was hastily reversed in April 2021 in response to concerns. Now that bond yields have spiralled, small savings rates have been revised upwards.

Image source: www.freepik.com

Image source: www.freepik.com

Join Now: PersonalFN is now on Telegram. Join FREE Today to get 'Daily Wealth Letter' and Exclusive Updates on Mutual Funds

Hike in interest rates for small savings schemes for Q4 FY 2022-23:

On December 30, 2022, the finance ministry issued a circular that the government has increased the deposit rate on some small savings schemes for the January-March 2023 quarter by 20-110 basis points bps (one percentage point is equivalent to 100 basis points. This is the second quarter of an increase in a row in interest rates for some schemes. Earlier, the government had increased the interest rate on these small savings schemes by 10-30 basis points for the October-December 2022 quarter. Prior to that, though, the rates remained unchanged for nine straight quarters.

[Read: What Does Rate Hike on These Small Savings Schemes Mean to Investors]

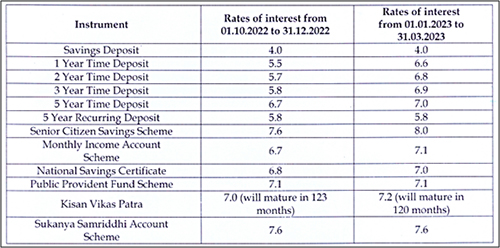

Here's the list of revised interest rates on small savings schemes for the January to March 2023 quarter:

(Source: DEA, Govt. of India)

(Source: DEA, Govt. of India)

As you can see, the interest rates of schemes like the Senior Citizen Savings Scheme, Monthly Income Savings Scheme, National Savings Certificate, Kisan Vikas Patra, and all post office time deposits have been hiked. However, the interest rates of the Public Provident Fund and Sukanya Samriddhi Yojana have not been changed for this quarter.

The government has given the New Year gift to all their investors and some of the new investors that are looking forward to investing in small saving schemes. Out of the 12 saving schemes, 8 have gone through rate hikes recently. In addition, the government has been favouring retirees and the senior savings scheme since the rate hike is more lucrative there.

[PPF Calculator] / [Retirement Calculator]

Should you invest in small savings schemes?

When most other fixed-income avenues - be it bank fixed deposits or bonds have seen falling interest rates, the small saving schemes saw rates at attractive levels. The hike in the interest rate of small savings schemes should be considered seriously because these interest rates won't be sustainable for a long time.

Also, considering the intensified market volatility, many investors would like to stick to high-credit quality bonds. Since small saving schemes are backed by a sovereign guarantee, there is low credit risk. Post office monthly income schemes are a good option if someone is looking for monthly income. It's good for retired investors. Since inflation has already shown signs of cooling, and if this trend continues, we may not see a significant hike in the next quarter, thus locking your investments at this revised rate could be beneficial.

However, do note that even though small savings schemes offer attractive interest rates, do not jump with all your money. Do take your liquidity needs into account, as many of these schemes score low on the liquidity front due to long-term lock-in periods. Most importantly, one should keep asset allocation in mind; if you have a shortage of debt in your investment basket, then small savings schemes are a good alternative.

Additionally, you should consider the macroeconomic uncertainties because they could result in low purchasing power of your savings and fixed-income investments. Since equities often beat inflation over a long period of time, some exposure to equities through mutual funds can help you tide over the risk of high inflation.

I would recommend a mix of equity mutual funds and small savings schemes where you have a regular and fixed cash flow. For instance, if you are looking for intermittent liquidity and have some long-term financial goals, such as funding your retirement corpus, then you may consider investing some money in PPF along with equity mutual funds. Additionally, if you intend to save money for your daughter's education over more than ten years, then complimenting Sukanya Samriddhi Yojana with systematic investment plans (SIP) in mutual funds makes sense.

PS: PersonalFN's SMART Fund Explorer can help you plan your mutual fund investments smartly to achieve your financial goals. You can simply state your S.M.A.R.T financial goals, such as the type of goal (buying a house, car, retirement, etc.), determine a suitable time frame for achieving them, and insert the amount of money that you are willing to invest towards your goal.

PersonalFN's SMART Fund Explorer will offer you with two mutual funds investment options (A & B) that you can choose based on your risk profile. Further, you can also get instant access to the list of the best suitable mutual fund schemes as per your selected plan by enrolling to PersonalFN's SMART Fund Explorer.

This is an opportunity to begin your investment in mutual funds with a smartly selected list of recommended mutual funds by our research team. So what are you waiting for? Click on the key to accomplishing your financial goals with PersonalFN's SMART Fund Explorer.

Warm Regards,

Mitali Dhoke

Research Analyst