Know Your Rights as an Insurance Policyholder

Rounaq Neroy

Sep 10, 2024 / Reading Time: Approx. 18 mins

Listen to Know Your Rights as an Insurance Policyholder

00:00

00:00

Here's what IRDA member, Mr Satyajit Tripathi recently said at the CII Financial Summit held in Mumbai:

“Grouse (in life insurance) is about mis-selling a product, and I must say that it is at an alarming level. It is at an alarming level because it has caught the attention of the policymakers. If we are talking about increasing the penetration, sale of various products, making it affordable, then we must address these grievances.”

In the case of non-life insurance policies, particularly health insurance, the grievance of policyholders concerns the payment of claims (as claims have been rejected or far less claim is paid) and exclusions.

In both life and health insurance policies, a common issue is that agents or sales officials do not explain the features of the policy to the proposers or prospects in totality; they hide certain crucial information. In other words, they simply hard-sell the policy in question to meet their sales targets. As a result, many individuals often go by the words of the agent and sales official, only to realise later that they were mis-sold the policy.

However, recognising all this, the IRDA has now issued a master circular last week to protect the interest of policyholders.

Here are the key measures stated...

-

Processing of the Proposal Form:

The proposer, i.e. the person or entity initiating the process of buying the policy, submits the proposal form, and the insurers will now be required to process the proposal with speed and efficiency. In case of the requirement for further details/clarifications on details given in the proposal form, the same will now need to be called for in one go within 7 days from the date of receipt of the proposal form, and not on a piecemeal basis.

Further, the insurer is required to decide on the proposal form within 7 days of receipt of the information. Also, on acceptance of the proposal form, the insurer will be required to promptly communicate its decision to the prospect along with the premium payable and provide coverage from the date of receipt of the premium payable.

In the case of non-acceptance of a proposal, the insurer shall inform the prospect of its decision within 7 days along with the reasons for non-acceptance.

-

Payment of Premium/Premium Deposit:

Only after the insurer communicates the decision of acceptance of the proposal to the proposer, the risk cover shall commence only after receipt of the premium.

No premium deposit/proposal deposit is required to be paid by you, the proposer to the insurer along with the proposal form, except in case of policies issued based on declaration of good health where risk cover commences immediately on receipt of premium. In such a case, there should not be scope for either short or excess collection of premiums by the insurer.

Moreover, insurers shall ensure that explicit consent is obtained from the prospect/policyholder for the deduction of the amount towards premium payment from the bank account.

-

Issuance of the Insurance Policy:

The insurers on acceptance of the proposal will be required to issue the insurance policy in an electronic form. As a policyholder, you have the option to store the soft copy of the policy document in Digilocker.

That said, all policies issued in electronic form by the insurer directly to the policyholder shall also be issued in physical form if requested by the policyholder. In this regard, the choice for you, the prospect/policyholder/customer, to avail of physical policy documents shall be mandatorily made available in the proposal form. So, don't forget to make your choice in the proposal form.

-

Documents to Be Submitted to the Insured:

When the prospect or proposer buys the policy, the insurer shall within 15 days of acceptance of a proposal, furnish the following to the prospect without any additional charge:

-

Covering letter for the policy document informing the free look period

-

Policy document

-

Copy of the proposal form submitted by the prospect

-

Copy of Benefit Illustration

-

Customer Information Sheet

-

Copy of Need Analysis document under Suitability Assessment, if any

-

Medical reports, wherever applicable

-

Any other document as may be required by the specific product

-

Make Available Customer Information Sheet (CIS):

At the time of receipt of the policy document, a CIS must be available in Schedule D of The Insurance Act, 1938, to you, the insured.

The CIS is a statement provided by the insurer along with the policy document that provides in simple words, important information and basic features of the policy issued in one place. These include:

-

Type of Insurance

-

Sum Assured

-

Benefits of the policy

-

Summary of exclusions which the policy does not cover

-

Certain important details, viz., free-look period, Policy Renewal date, options like the revival of policy, policy loan and any other options

-

Information regarding the claim Procedure, policy servicing and grievance redressal mechanism, including the contact details of the Insurance Ombudsman of the appropriate jurisdiction

On request, the CIS can also be obtained by you from the insurance company in a regional language.

As per the IRDA, CIS shall be provided to every policyholder in case of both 'Individual Insurance' policyholders as well as a member of a 'Group Insurance Policy'.

Further, the insurer will be required to obtain acknowledgement in physical or digital from the policyholder.

If you, the policyholder find any inconsistency in the coverage or scope of the policy, the same may be taken up with the insurer either directly or through the distribution channel engaged in procuring the policy for suitable rectification.

-

Free Look Period:

From the date of receipt of the life insurance policy having a policy term of one year or more, you, the policyholder will have 30 days, called the 'Free Look period', to review the terms and conditions of the policy.

In case you, the policyholder, are not satisfied with policy terms or conditions, you have the option to return the policy within these 30 days to the insurer for cancellation. Irrespective of the reasons mentioned, the insurer will have to accept the request to exercise the option of free look cancellation.

As regards the refund of the premium paid, you, the policyholder shall be entitled to it subject only to a deduction of a proportionate risk premium for the period of cover and the expenses, if any, incurred by the insurer on medical examination of the proposer and stamp duty charges.

In case it is a linked insurance policy, subject to the deductions mentioned, the insurer shall refund the proceeds by repurchasing the units at the Net Asset Value (NAV) of the units on the date of cancellation.

The applicable refund of the premium upon free look cancellation shall be refunded within 7 days of receipt of the request for free look cancellation. In case of any delay in the refund, the insurer would be required to pay interest at the bank rate plus 2% on the refundable amount, from the date of receipt of the request for free look cancellation till the date of refund. Such interest shall be paid suo-moto by the insurer.

-

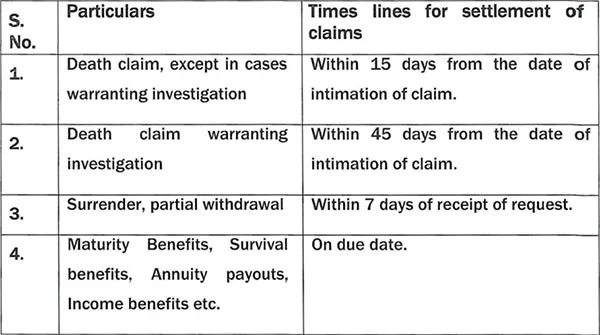

Intimation and Settlement of Claim:

On the happening of a special event as specified in in the policy document, you, the policyholder or claimant, as the case may be, will be required to inform the insurer, about the happening of the insured event resulting in a claim under the insurance policy, at the earliest possible time either in person or through the online mode, through distribution channel, or authorised call centre of the insurer, or any other mode as specified in the policy document.

All documents to process a claim need to be stated by the insurers in the policy document plus displayed on their website with the claim form made available.

No claim shall be rejected or closed for want of documents or due to delayed intimation of the claim.

The life insurance claims received by the insurers shall be processed and settled within the timelines specified as under:

(Source: IRDA Master Circular, dated September 5, 2024)

(Source: IRDA Master Circular, dated September 5, 2024)

In case the claim is not settled within the specified timelines, then the claimant is entitled to interest at bank rate plus 2% from the date of receipt of intimation till the date of payment. Such interest shall be paid by the insurer suo-moto along with the claim amount.

Other than the above, the key measures specific to health insurance are as follows...

-

Make Available Products/Add-ons/Riders to the Policyholders

Health insurers are responsible are required to make available products/ products/add-ons/riders to policyholders/prospects catering to:

-

All ages

-

All types of existing medical conditions

-

Pre-existing diseases and chronic conditions

-

All systems of medicine and treatments, including Allopathy, AYUSH and other

systems of medicine

-

Every situation of treatment, including domiciliary hospitalisation, outpatient treatment (OPD), daycare and homecare treatment

-

All regions, all occupational categories, persons with disabilities and any other categories

-

All types of Hospitals and Health Care Providers to suit the affordability of the policyholders/ prospects

According to the IRDA, insurers shall allow for customisation of products by customer by providing the flexibility to choose products/add-ons/riders as per his/her medical conditions or specific needs.

The IRDA master circular also states that insurers shall offer products in accordance with relevant provisions of the following laws:

-

The Mental Healthcare Act, 2017

-

The Rights of Persons with Disabilities Act, 2016

-

The Surrogacy (Regulation) Act, 2021

-

The Transgender Persons (Protection of Rights) Act, 2019, and

-

The HIV and AIDS (Prevention and Control) Act, 2017

Moreover, you, the policyholder cannot be denied coverage in case of emergency situations.

-

CIS For Health Insurance Policy:

The CIS for health insurance policies should include:

-

Type of Insurance

-

Sum Insured

-

Coverage provided

-

Summary of exclusions which policy does not cover

-

Sub-limits (a pre-defined limit above which the insurer will not pay),

-

Deductibles (specified amount up to which an insurer will not pay any

-

Claim/which will be deducted from the total claim, if the claim amount is more than the specified amount), co-payment,

-

Waiting period(s) (time period during which specified diseases/treatments are not covered), and

-

Certain important things, such as the free look period, policy renewal, migration, portability and moratorium period

Moreover, CIS for a health insurance policy should also carry information regarding the claims procedure, policy servicing, and grievance redressal mechanism, including contact details of the Insurance Ombudsman of the appropriate jurisdiction.

-

No Claim Bonus (NCB) Adjustment:

During the policy term of your health insurance, if there is no claim, the NCB shall be adjusted as an addition to the sum insured without an associated increase in the premium and/or discount in the renewal premium.

-

Health Insurance Claim:

The policyholder or the claimant, as applicable, is required to inform the insurer, about the happening of a claim under the insurance policy, at the earliest possible time either in person or through the online mode, distribution channel, TPA, hospital/healthcare provider where such facility is provided, authorised call centre of the insurer, or any other mode as specified in the policy document.

Further, no claim shall be rejected or closed for want of documents or due to delayed intimation of the claim.

[Read: Your Health Insurance Just Got Better - New IRDA Regulations Explained]

[Also read: A Single Platform for All Your Cashless Health Insurance Claims]

In case the claim is not settled within the specified timelines, then the claimant is entitled to interest at bank rate plus 2% from the date of receipt of intimation to the date of payment. Such interest is to be paid suo-moto by the insurers.

-

Claim Settlement for Multiple Health Insurance Policies:

In the case of 'indemnity policies', if you, the policyholder have more than one health insurance policy from different insurers, you can file for claim settlement as per your choice under any policy.

The insurer of that chosen policy shall be treated as the 'primary insurer'. In case the available coverage under the said policy is less than the admissible claim amount, the 'primary insurer shall' seek the details of other available policies of the policyholder, his/her choice of the other insurer(s), and shall coordinate with other insurers to ensure settlement of the balance amount as per the policy conditions, without causing any hassles to you, the policyholder.

In the case of 'benefit-based policies', on the occurrence of the insured event, you, the policyholder, can from all insurers under all policies.

What about the Complaint Mechanism or Raising of Complaints?

In case you, the policyholder or the claimant needs to raise a complaint against the insurer, distribution channel, authorized entity to collect premiums, or third-party administrators (TPA), there are grievance addressal procedures available.

You can file the complaint by visiting the nearest branch, through a letter or email or on the insurer's website or by calling the designated call centre of the insurer.

You, the policyholder or the claimant also have the option to register the complaint online on the IRDAl's Bima Bharosa by visiting https://bimabharosa.irdai.gov.in

When a complaint is filed, you are entitled to receive an acknowledgement of the complaint immediately. As per the IRDA, insurers are required to provide a resolution to the complaint within 14 days along with the reasons for not accepting the complaint with specific reference to the relevant terms and conditions of the policy.

In case you, the complainant, are not satisfied with the resolution of the grievance provided by the insurer, you can escalate the unresolved / partially resolved complaints to the Insurance Ombudsman of the concerned jurisdiction, in case the claim amount is up to Rs 50 lakh.

As a policyholder, you also have the option to take up the matter before the insurance ombudsman of competent jurisdiction without any charge/fee in person, online by visiting https://cioins.co.in/Complaint/Online or by writing by post or by email by providing complete details.

Final Words...

The IRDA, apart from playing the role of an insurance development authority, of late, has been on the vigil to keep check on malpractice and instances of mis-selling in the insurance industry. By categorically stating what insurers need to do, IRDA has truly empowered policyholders. Watch this video:

Besides, there are several initiatives, such as 'Cashless Everywhere' and a single platform for all cashless health insurance, called the National Health Claims Exchange (NHCX) -- to settle cashless health insurance claims -- which, in my view, would make claim settlement a hassle-free experience for policyholders and the frustratingly long wait time for claim settlement.

[Read: Your Ultimate Guide to Cashless Health Insurance]

So, all in all, the IRDA is playing a customer-centric approach, which shall set high standards of service in the insurance industry and protect the interest of policyholders.

Make sure you have insured yourself adequately -- for health and life. It is an integral aspect of financial planning.

When you buy a life insurance cover, the sole objective should be to indemnify risk to your life as the breadwinner and safeguard the financial well-being of the dependent family members. Hence ensure that you have adequate life insurance coverage with a term plan considering your Human Life Value (HLV).

Similarly, a comprehensive health insurance policy with an adequate sum insured (considering your family's medical history, the pre-existing diseases or comorbidities (if any), the number of dependent family members, the state and city you reside for access to healthcare facilities, the network of hospitals, and the healthcare costs) along with the all-embracing features of the policy (including the no-claim bonus) is important.

So make sure you adding to your financial security.

Be thoughtful in your approach.

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and use such independent advisors as he believes necessary.