Are You Setting Your Risk-Return Expectations Right While Investing in Mutual Funds?

Rounaq Neroy

Nov 16, 2022

Listen to Are You Setting Your Risk-Return Expectations Right While Investing in Mutual Funds?

00:00

00:00

Risk and returns are two sides of the same coin. To put it differently, they are correlated: for every return you seek, there is a certain level of risk. That's why, in investing, it is important to evaluate returns more meaningfully by assessing the risk involved.

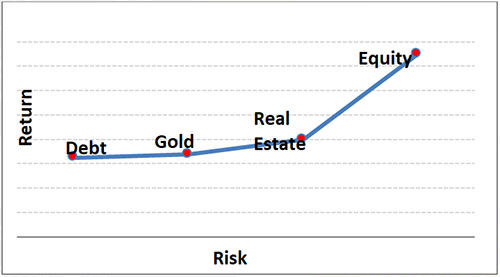

Every asset class -- be it equity, debt, gold, or real estate -- commands a certain level of risk-return trade-off. Typically, fixed-income & debt instruments carry low risk, while real estate and equity are at the higher end of the risk-return spectrum. That said, it is not always that high risk translates into high returns.

Graph 1: Distinctive risk-return trade-off of asset classes

(The graph above is for illustration purposes only.)

(The graph above is for illustration purposes only.)

Benjamin Graham, the father of value investing, the author of the famous book- The Intelligent Investor (published in 1949), and Warren Buffett's hero and mentor aptly states, "Successful investing is about managing risk, not avoiding it."

Graham further opines, "The essence of investment management is the management of risks, not the management of returns."

Thus, you must be mindful of the risk involved -- and not invest blindly going by just the returns. Only tracking the returns of a mutual fund scheme is stupid; it may be detrimental to your health and wealth.

Even when a bank is offering an extraordinarily high interest rate (than the market rate) on deposits, it should sound an alarm bell. You would appreciate that the money in bank deposits is essentially to preserve capital and not clock a high return.

For better returns you could, of course, consider mutual funds, which are a potent avenue for wealth creation. But mind you, depending on your scheme choice, the investment will be subject to macroeconomic risk, inflation risk, interest rate risk, price risk, business risk, political risk, credit risk, liquidity risk, re-investment risk, and fund management risk, among others.

Every category (equity, debt, hybrid, gold, solution, and others) and sub-category of a mutual fund scheme has distinctive traits (in terms of asset allocation, investment strategy, and investment objective), and finds a distinct place on the risk-return spectrum.

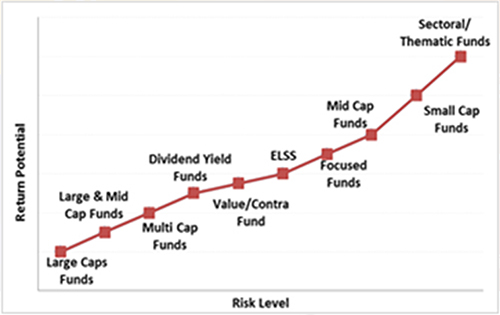

Graph 2: Risk-Return Spectrum of Equity Funds

(For illustration purposes only)

(For illustration purposes only)

For example, amongst the equity-oriented ones, a Large Cap Fund is usually placed at the lower end of the risk-return spectrum (as they invest in stocks of well-established companies having reliable brand equity, customer loyalty, competitive advantage, large and deep moat, quality management, strong balance sheet, easy access to various resources, and sustainable business models), whereas a Sector/ Thematic Fund is placed at the high end of the risk-return spectrum (due to portfolio concentration risk and the fortune of the fund is closely linked with that of the sector or theme).

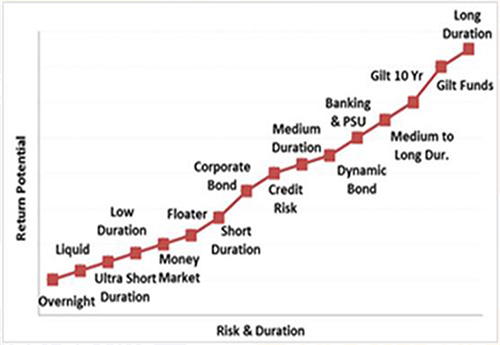

Graph 3: Risk-Return Spectrum of Debt Funds

(For illustration purposes only)

(For illustration purposes only)

In the case of debt-oriented schemes, the Overnight Funds and Liquid Funds are the least risky (as they invest in debt instruments having a maturity of a day, week and/or up to 91-days --typically in money market instruments, viz. T-Bills, Repos on G-secs, call money, CDs, and CPs. Whereas the credit risk funds (owing to high credit risk) and longer duration funds (due to sensitivity to interest rates) are placed at the higher end of the risk-return spectrum.

[Read: 5 Best Low-Risk Mutual Funds to Invest in 2023]

Note that mutual funds are mandated to disclose an indicative risk-o-meter for every scheme. Depending on the investment mandate, a fund is classified as Low Risk, Moderately Low Risk, Moderate risk, Moderately high, High, and Very High Risk. The regulatory guidelines make it binding on fund houses to review the risk-o-meter of the respective schemes in the product basket monthly and disclose the reviewed risk-o-meter along with the portfolio disclosures for all their respective schemes, plus make it live on the fund house and AMFI website (by the 10th of every month). Further, they are mandated to disclose the number of times the risk level changed over the year.

For you, the investor, it is vital to pay attention to this aspect to understand the risk traits of the scheme. You ought to make thoughtful choices considering your personal risk profile and ensure that it matches that of the schemes you choose.

You can't be investing in an ad hoc manner or simply follow what the next-door neighbour, friends, relatives and/or colleagues do with their investments. Investing in an individualistic exercise, there is no such thing as a one-size-fits-all approach.

Therefore, gauge what's your risk profile. This can be done by considering factors such as your current age, financial circumstances, insurance cover, the broader investment objectives, the financial goal/s you wish to address, and the time horizon to achieve the goal/s, among others.

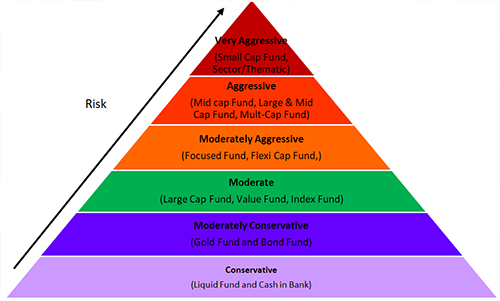

Risk profiling would help you assess whether you are a...

- Very Aggressive Investor (willing to take exceptionally high risk for extraordinary returns);

- Aggressive Investor (willing to take high risk for high returns);

- Moderately Aggressive Investor (willing to take a high calculated risk to clock moderately high returns); or

- Moderate investors (willing to take a moderate risk for moderate returns)

- Moderately conservative (willing to take average risk for average returns)

- Conservative Investor (who is satisfied with low returns with low risk and looking for portfolio stability)

Image 1: Allocation Pyramid Based on Risk Profile

(For illustration purposes only)

(For illustration purposes only)

Also, just skewing your investments to one particular asset is unwise. To balance the risk-return trade-off, investing across asset classes such as equity, debt, gold, real estate, or even holding cash, for that matter, is important. This is akin to putting eggs in different baskets, helping you to reduce the risk.

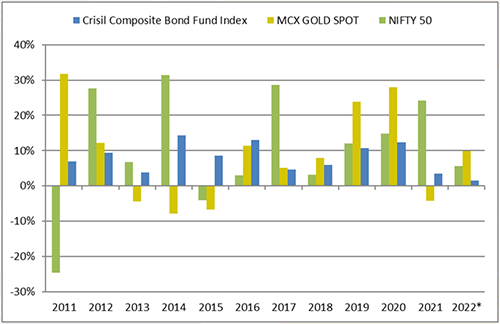

Graph 4: Performance of various asset classes over the years

*Data as of November 15, 2022

*Data as of November 15, 2022

MCX spot price of gold used.

(Source: MCX, ACE MF, PersonalFN Research)

The graph above is testimony to the fact that not all asset classes have moved in the same direction always. In certain years equities have rewarded investors handsomely (such as in 2012, 2014, 2017, 2020, and 2021). In years when equities encountered headwinds due to macroeconomic uncertainty and rising interest rates; gold, debt and fixed-income instruments have done well.

(Image source: freepik.com)

(Image source: freepik.com)

Join Now: PersonalFN is now on Telegram. Join FREE Today to get 'Daily Wealth Letter' and Exclusive Updates on Mutual Funds

Hence, follow a sensible asset allocation as per your risk profile. It would stand as a strategy adducing the following eight great benefits:

1) Diversify the portfolio, which is one of the basic tenets of investing

2) Reduces dependence on a single asset class

3) Minimises the risk when a certain segment of the capital market hits turbulence

4) Provide the freedom from timing the market

5) Optimise the risk-adjusted returns of the portfolio

6) Ensure adequate liquidity to the investment portfolio

7) Help build a weather-proof portfolio

8) Aids in achieving the envisioned financial goals

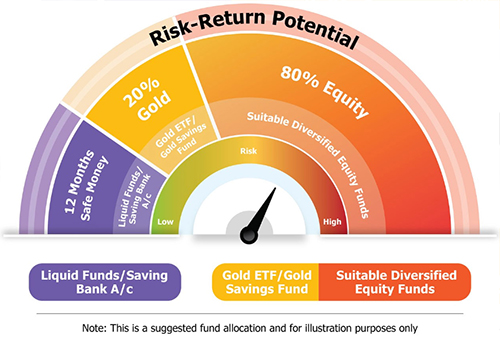

Image 2: 12-20-80 Asset Allocation

Say you are young, have financial goals to achieve, and are willing to take the risk to clock an efficient real return (also known as inflation-adjusted returns); you could broadly follow a 12-20-80 Asset Allocation strategy, wherein you start off by setting aside 12 months of regular monthly expenses (including EMIs on loans) into a Liquid Fund and/or Savings Account (to address any exigencies), park 20% in gold as a portfolio diversifier (a hedge, plus a store of value in times of economic uncertainties), and the remaining 80% invest in suitable diversified equity funds as per your risk profile. This strategy could potentially offer your portfolio the correct mix of stability, growth, and protection.

When selecting equity-oriented funds, be wary of schemes that expose you to extra-ordinarily high risk but don't compensate enough on a risk-adjusted basis. In a rising market, most mutual funds may fare well, but the true test would be in assessing how they are able to limit the downside risk volatile and corrective phases of the market.

To help you invest in the best equity funds that might help you outperform the broader markets, I suggest subscribing to PersonalFN's unbiased flagship mutual fund research service, FundSelect.

PersonalFN's FundSelect service will provide you with insightful and practical guidance on which mutual fund schemes to Buy, Hold, and Sell.

PersonalFN's FundSelect is driven by S.M.A.R.T processes -

S - Systems and Processes

M - Market Cycle Performance

A - Asset Management Style

R - Risk-Reward Ratios

T - Performance Track Record

This stringent process has helped our valued mutual fund research subscribers to own some of the best mutual fund schemes in their investment portfolio with a commendable long-term performance track record.

Currently, with the subscription to FundSelect, you could also get Free Bonus access to PersonalFN's Debt Fund recommendation service DebtSelect.

We are also providing direct recommendations on the best Equity Linked Saving Schemes (ELSS) to invest in 2022, which can help you save tax (under Section 80C of the Income Tax Act, 1961).

If you are serious about investing in rewarding mutual fund schemes, subscribe to FundSelect now!

A thoughtful and informed decision you make as an investor, taking a calculated risk, may prove to be in the interest of your long-term financial well-being.

Happy Investing!

Warm Regards,

Rounaq Neroy

Editor, Daily Wealth Letter