Direct vs Regular Plan: Can Expense Ratio Make Significant Difference to Your Mutual Fund Returns?

Divya Grover

Feb 28, 2024 / Reading Time: Approx. 7 mins

Listen to Direct vs Regular Plan: Can Expense Ratio Make Significant Difference to Your Mutual Fund Returns?

00:00

00:00

When you invest in mutual funds, you have the option to choose between Direct plan or Regular plan.

Regular and Direct plans of mutual funds are similar in every aspect, such as investment strategy, objective, portfolio, and fund manager. The only differentiating factor is the expense ratio.

To run a mutual fund house and schemes, several costs are involved such as investment management fees, brokerage on buying and selling securities, registrar & transfer fees, custodian fees, legal fees, audit fees, sales & marketing /advertising expenses, administrative expenses, and so on.

These costs are levied on the mutual fund scheme as a percentage of its daily net assets and are referred to as the Total Expense Ratio (TER). All mutual fund schemes are mandated to disclose the daily NAV after adjusting the TER.

How is the Total Expense Ratio or TER calculated?

The formula used to calculate TER is as follows:

Total Expense Ratio (TER) = (Total Expense of the Scheme during the period / Total Scheme Assets) x 100

When you opt for the Regular plan, you transact through an intermediary, whereas in the case of Direct plan, you purchase units directly from the asset management company or through mutual fund platforms encouraging Direct plans.

The Regular plan of a mutual fund charges a higher expense ratio compared to the Direct plan to incentivise the intermediary. Notably, mutual fund distributors usually advise investors on the type of schemes they should consider investing in. They also assist them with the investment process such as submitting KYC documents and application form, as well as generating account statement, placing redemption requests, etc.

For rendering these services, the asset management companies (AMCs) pay regular commission to the distributors as long as investors stay invested in the regular plan. The AMC adds these commissions to the TER of Regular plans. As a result, the TERs of regular plans are higher.

In the case if Direct plans, investors can directly invest in schemes through the website of the AMC or through various only investment platforms available in the market. Since there are no intermediaries involved the AMCs do not incur distribution expense. As a result, the TER of Direct plans are lower.

Can the difference in expense ratio make a big difference to your mutual fund returns?

The difference in expense ratio of Direct plan and Regular plan of diversified equity mutual funds ranges from 0.4% to 2%, with an average difference of about 1.2%.

A marginal difference of 0.5-1% may not seem much. But over a sufficiently long investment horizon, the difference in expense ratio of Direct plan and Regular plan of mutual funds can make substantial difference to the overall returns generated by a scheme, thanks to the power of compounding.

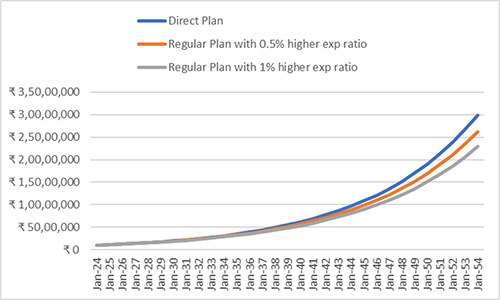

Difference in overall corpus between Direct plan and Regular plan of mutual funds

(For illustration purpose only)

(For illustration purpose only)

Source: PersonalFN Research

As we can see in the above chart, there is a notable difference in corpus at the end of the goal period. In this example an investment of Rs 10 lakh is invested in Direct plan, with a similar investment in the Regular plan of the same scheme assumed at 0.50% and 1% higher expense ratio.

The table below demonstrates how small savings of 0.50% or 1% in the expense ratio over 30 years can make a huge difference, assuming the returns clocked are 12% compounded annualized.

|

Direct Plan (in Rs) |

Regular Plan with 0.5%higher Exp. Ratio (in Rs) |

Regular Plan with 1%higher Exp. Ratio (in Rs) |

| Amount invested |

10,00,000 |

10,00,000 |

10,00,000 |

| Value after 30 years |

29,959,922 |

26,196,666 |

22,892,297 |

(For illustration purpose only)

Source: PersonalFN Research

At the end of 30-year period, the corpus under the Direct plan would have appreciated to nearly Rs 3 crore.

If we consider a similar investment in a Regular plan that has a 0.5% higher expense ratio, the corpus at the end of 30-year timeframe would be around Rs 37.6 lakh lower compared to investment in Direct plan.

Likewise, the end value of same amount invested in a Regular plan with 1% difference in expense ratio would be around Rs 2.3 crore.

So, even a 1% lower expense ratio makes a whopping difference of about Rs 70 lakh.

This highlights the promising potential of choosing Direct plan over Regular plan.

Another benefit of investing in Direct plan is that you can avoid potential mis-selling by certain mutual fund distributors who may misguide you. Investing in Direct plans gives you the opportunity to do your own research and analyse the various options available.

Should you opt for Direct plan or regular plan?

As an investor, if you can build and monitor your mutual fund portfolio on your own, you can opt for the Direct plan and benefit from the lower expense ratio. However, if you lack the expertise and/or time required to select the right mutual funds and monitoring of the portfolio and other investment decisions, you can seek assistance of an intermediary.

Once you have selected suitable and worthy funds for your portfolio, stay invested until you achieve your goals. Remember, frequently buying and selling mutual fund units can also add to the expense ratio of your portfolio, which can impact your overall returns. It would be prudent to understand the pros and cons of each plan and then decide what works best for you.

You can shift from regular to direct plan by putting a switch request to AMC. However, since switch out from one plan or schemes is treated as redemption, exit load and charges may apply. Capital gains tax may also apply depending on the holding period.

Should you always opt for schemes with lower expense ratio?

Whether you opt for Regular or Direct plan, the expense ratio is always charged on your investment, and it can eat into your profits. Though the difference between the expense ratio of two schemes within a category seem small, it can affect your overall returns. Over time the difference in expense ratio can have a considerable impact on the profit due to the effect of compounding.

Difference in expense ratio and net returns of two schemes

|

Fund A |

Fund B |

| AUM (Rs) |

1,00,000 |

1,00,000 |

| Scheme return |

15.00% |

15.00% |

| Expense as % of AUM |

2.50% |

1.25% |

| Net returns |

12.50% |

13.75% |

| Gross returns in Rs |

15,000 |

15,000 |

| Expense in Rs |

2,500 |

1,250 |

| Net returns in Rs |

12,500 |

13,750 |

| Expense as % of returns |

16.67% |

8.33% |

(The figures are for illustrative purpose only)

Source: PersonalFN Research

However, this does not mean that a fund with a lower expense ratio is always better. Each scheme follows its own investment strategy and style. A fund may have a higher expense ratio compared to other schemes within the category if it follows an aggressive investment strategy. It can still generate higher returns and compensate investors for the high expense it has charged. Note that mutual fund schemes charge the expense ratio on a regular basis regardless of the fund's performance.

So, if you always choose funds with the lowest expense ratio, you may lose out more in terms of returns than what you would gain from lower expense of the scheme. This highlights that the expense ratio cannot be a sole parameter to select funds.

Instead, the expense ratio should be looked at in conjunction with other criteria, quantitative and qualitative, that will help you determine the worthiness of the scheme. Click here to read about the parameters to look into to select the best mutual fund schemes

Before shortlisting any fund on the aforementioned parameters, ensure that the investment objective of the scheme aligns with your own risk profile, investment horizon, and financial goals.

If you find two or more funds with similar performance track record and quality of fund management, you can consider selecting a fund with lower expense ratio. However, bear in mind that expense ratios are not static and may rise in the future.

We are on Telegram! Join thousands of like-minded investors and our editors right now.

DIVYA GROVER is the co-editor for FundSelect, the flagship research service of PersonalFN. She is also the co-editor of DebtSelect. Divya is an avid reader which helps her in analysing industry trends and producing insightful articles for PersonalFN’s popular newsletter – Daily Wealth letter, read by over 1.5 lakh subscribers.

Divya joined PersonalFN in 2019 and has since then used stringent quantitative and qualitative parameters to analyse funds to provide honest and unbiased research to investors. She endeavours to enable investors to make an informed investment decision and thereby safeguard their wealth.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.