How Donald Trump's Victory Would Playout On the Indian Equity Market

Rounaq Neroy

Nov 11, 2024 / Reading Time: Approx. 15 mins

Listen to How Donald Trump's Victory Would Playout On the Indian Equity Market

00:00

00:00

The Indian equity market has been rather volatile of late. One of the factors weighing on is the geopolitical scenario.

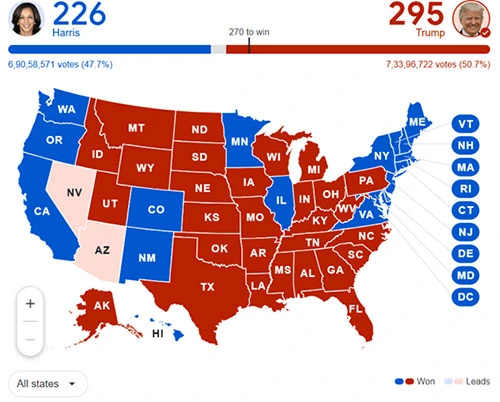

In the recently concluded U.S. Presidential elections, Donald Trump (of the Republican Party) triumphed over the Democratic Party candidate Kamala Harris, becoming the 47th President of the United States of America (USA) by a sweeping majority and also gained control of the Senate.

(Source: The Associated Press)

(Source: The Associated Press)

Trump is the second President who has been re-elected for the second non-consecutive term after Grover Cleveland, a Democrat -- the 22nd President of the U.S. from 1885 to 1889 and later the 24th President from 1893 to 1897. For the period 1889 to 1893, Benjamin Harrison, a Republican served as the 23rd President of the U.S.

With Trump back as 47th President (after serving as 45th President from 2016 to 2020) this time around, at his age of 78, he is also the oldest President in the history of the U.S. to be re-elected despite having faced impeachment proceedings twice.

During his earlier term, the S&P 500 -TRI gained around 68%, while under Joe Biden's term around 83% (absolute returns). Biden got an advantage of a major upswing in the equity market since the COVID-19 low. Nevertheless, Biden has beaten Trump as regards equity returns, contrary to Trump's warning then to voters back in 2020 (in the race for re-election as the 46th President) that stock market returns would implode if he were replaced by Biden.

But now Donald Trump is back as the 47th President of the U.S. Will he outshine his predecessor, Joe Biden as far as the U.S. stock market returns are concerned?

Also, the question is how his term will (post his inauguration ceremony on January 20, 2025) play out on the Indian equity market.

Well, the answer to these questions lies in the policies Trump follows.

As you may know, he reached out to voters with his campaign "Make America Great Again". He has pledged to help the United States "heal".

In this endeavour, it is likely that Trump would follow American-centric and protectionist policies.

Trunmponomics 2.0

Trump is likely to increase tariffs on foreign goods, potentially shift supply chains away from China to more favourable countries like India with the China+1 strategy in sight, push other countries to reduce trade barriers, tighten visa issuance to certain foreign nationals, reduce corporate tax in the U.S., resort to fiscal expansion and press the U.S. Federal Reserve to cut interest rates and much more -- all in the endeavour to re-industrialise America once again and invigorate economic growth.

In the recently held Federal Open Market Committee (FOMC) meeting on November 7, 2024 -- soon after the U.S. Presidential election -- the federal funds rate was cut by 25 basis points (bps) to 4.50%-4.75%.

This decision was taken in view of solid expansion in economic activity, a decrease in the unemployment rate, as labour market conditions eased, and inflation moved closer to the 2.0% target of the Federal Reserve (Fed). With the recent 25 bps rate cut, the Fed has so far cut rates cumulatively by 75 bps.

After Donald Trump's victory, Fed Chief, Jerome Powell, said that election results will have "no effects" on the central bank's policy decision in the near term.

The last statement of the FOMC meeting says that will continue to monitor the implications of incoming information for the economic outlook. It will consider a wide range of information, including readings on labour market conditions, inflation pressures and inflation expectations, and financial and international developments. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals.

That being said, for now, rate cuts have augured well for risk-on assets such as equities. The 10-year U.S. treasury yield too has softened a bit of late, however, since the previous September 2024 FOMC meeting the 10-year yield is still up around 70 bps.

It is unlikely that the ''Trump trade' would roll back the U.S. 10-year yield much while Trump potentially resorts to fiscal expansion, spending, reducing corporate tax, and imposing higher tariffs on foreign goods.

In such a scenario, the U.S. Dollar (USD) meanwhile would continue to exhibit strength. However, fiscal expansion and loose monetary policy may also lead to a high debt for Trump 2.0.

Speaking of trade policies with India, given the bonhomie Trump shares with Prime Minister, Narendra Modi, it is unlikely that he would be harsh on India. On the contrary, he would build on the good relations with India keeping in sight the China+1 strategy.

In his earlier term, Trump did increase tariffs on certain products from India and withdrew preferential treatment to India -- and in retribution, India also slapped higher tariffs on certain U.S. products. But the fact is bilateral trade between the two countries during Trump 1.0 did grow by 73% to USD 88.9 billion by the end of 2019-20.

Having said that, Trump is a transactional leader and objective in his approach. He will not partner unless there are clear benefits visible. Besides he is mercurial, who likes to keep everyone guessing. Owing to this trait geopolitical landscape will also be interesting to watch.

Geopolitics Under Trump 2.0

In the Middle East, where there are ongoing tensions between Israel and Iran (as a consequence of the Israel-Hamas war and Israel-Hezbollah conflict), there are fears that Trump 2.0 may empower Israel with the support of the U.S. to eliminate these terror groups sponsored by Iran.

Even Biden supported Israel in its war against Iran-backed terror groups. But now, under Trump 2.0, Iranians are fearing more strikes on its soil, sanctions, and economic hardships.

In the ongoing Russia-Ukraine war, a Euronews report suggests that some Ukrainians too fear that Trump's victory could imperil their future, as he for transactional and strategic gains would move closer to Russia's President, Vladimir Putin.

Besides, it's common knowledge that the U.S. shares strained relations with China. Moreover, there are tensions between China and Taiwan, China and the Philippines, as well as North Korea and South Korea.

The U.S. and South Korea are allies under the 1953 Mutual Defence Treaty. The U.S. military has also been supporting Taiwan primarily through the sale of arms & ammunition for decades so as to keep China away.

The crisis over Taiwan may trigger a war between the U.S. and China, even though the U.S. does not have a treaty obligation to defend Taiwan. This 'strategic ambiguity' seems to be intentionally maintained by the U.S., as it considers Taiwan as a key partner in the Indo-Pacific region.

In such times of geopolitical tensions and protectionist policies during Trump 2.0, there are good chances of geoeconomic fragmentation, supply chain disruptions, and 'imported inflation' (owing to a stronger USD).

Impact on Equity Markets

Given all the above facets, net inflow from Foreign Portfolio Investors (FPI) into emerging markets will also be contingent upon the geopolitics, policies, and macroeconomic activity actually pans out.

If under Trump 2.0 corporate taxes are indeed reduced (from the current 25% to 15% with a rider that companies should make their products in the U.S.) and President-elect Donald Trump's efforts indeed show up on earnings of companies, creating jobs, consumer spending, housing, among the other factors; flows to emerging markets, including India, may taper as U.S. equities outperform global markets. In the U.S., the Q3 2024 corporate earnings of several S&P 500 companies have been quite encouraging. U.S. equities are surging and in such a case global equity risk premium is also reducing.

In contrast, India's corporate earnings, at present after encouraging data post-pandemic (in the last four years), have entered a slow lane or a cyclical downturn owing to higher expenses, input costs, and slowing consumer demand.

During Trump 2.0 Indian equity market equity markets are going to get mixed signals, so tighten your seat belts and embrace high volatility.

A key factor that will set the direction of the Indian equity market will be corporate earnings growth. It would be imprudent to expect that Indian equities would do well just because Trump shares affability with Prime Minister Modi and would consider India for the China+1 strategy. Note that, ultimately it is important that corporate earnings justify market valuations.

Avoid getting carried away by and being over-optimistic about earnings when input costs and overhead expenses are increasing, plus demand is waning. Don't live under the impression that earnings would improve linearly quarter-on-quarter.

Pay Heed to Valuations

After a fast run-up in the Indian equity markets in the last few years, India commands a premium compared to global peers.

Graph: MSCI India witnessed a sharp upswing compared to MSCI Emerging Markets

Cumulative index performance - gross returns (INR). Date from October 2009 to October 2024

Cumulative index performance - gross returns (INR). Date from October 2009 to October 2024

Past performance is not an indicator of future performance.

(Source: MSCI India Index Factsheet)

The Morgan Stanley Capital International (MSCI) India Index trail Price-to-Equity (P/E) ratio is over 27x while the MSCI Emerging Markets Index and MSCI World Index trail P/Es are around 16x and 22x, respectively, as per the latest factsheets as of October 31, 2024.

While India's valuation premium dropped a bit since the peak, it is still way above the MSCI Emerging Markets Index and the World Index.

Even on a 12-month forward P/E, India with a P/E of nearly 23x is commanding a premium vis-a-vis the MSCI Emerging Market Index and World Index whose forward P/E is around 12x and 19x, respectively.

Now while some may perceive the premium that Indian equities command relative to global peers seems justified given that India is a "bright spot" and the fastest-growing economy with a favourable demographic dividend and rising income, in my view, the margin of safety is not very comforting at this juncture, particularly in the mid and smallcap segment of the market.

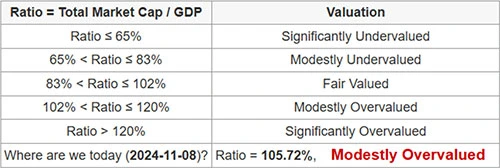

Table: India's current Market cap-to-GDP ratio

Data as of November 8, 2024

Data as of November 8, 2024

Based on historical values, divided into five zones.

(Source: https://www.gurufocus.com/global-market-valuation.php?country=IND)

At present, even India's market capitalisation-to-GDP ratio, famously called the Buffett indicator (named after legendary investor Warren Buffett), is in the 'modestly overvalued' zone notwithstanding some correction since the peak.

Particularly when there are ostensible clouds of global economic uncertainty and geopolitical tensions, you ought to adopt caution and not get carried away by irrational exuberance. Moreover, it is important to keep return expectations rational, given that volatility may increase.

"The essence of investment management is the management of risks, not the management of returns." - Benjamin Graham (the father of value investing and Buffett's mentor).

Keep in mind that for every level of return you seek, there is a certain level of risk. And it is not always true that that high risk translates into high returns.

Investment Strategy to Follow Now

It is important that you follow a 'Core & Satellite' approach when investing in equity mutual funds now. It is a strategy followed by some of the most successful equity investors around the world.

The term 'Core' refers to the portfolio's more stable, long-term equity holdings. Given that, Your core portfolio of the equity mutual fund portfolio should mainly comprise some of the best Large Cap Funds, Flexi-cap Funds/Multi-cap Funds, and Value/Contra Funds that can add stability to the investment portfolio and potentially steadily multiply your wealth by keeping an investment horizon of around 5 years.

The 'Satellite' portion of the portfolio, on the other hand, may include a couple of best Mid-cap Funds (max 2) and an Aggressive Hybrid Fund. In these funds keep an investment time horizon of around 7 to 8 years. These funds would support boosting the portfolio's overall returns given their risk-return characteristics. At this juncture, avoid adding Small Cap Funds and Sector/Thematic Funds to the satellite portfolio, even if you are a very aggressive investor with a stomach for very high risk and a good understanding of these funds.

Such a 'Core & Satellite' investment strategy shall prove sensible when deploying money into equity funds to address your long-term financial goals.

Should You Make a Lump Sum Investment or Take the SIP Route?

Given that there are chances of high volatility, to make fresh investments, at a market high, it would be prudent to make staggered lump sum investments, or even better is to take the Systematic Investment Plan (SIP) route (particularly when planning for your long-term financial goals).

[Read: Micro SIPs in Mutual Funds: Is It a Good and Feasible Idea?]

Apart from equities for wealth creation, also allocate sensibly to debt & fixed income instruments and gold. An adequate prudent exposure to these two asset classes may add some stability to your portfolio, they may protect you when equities undergo turbulent times.

[Read: Donald Trump Is Back as the 47th U.S. President. Here's What It Means for Gold]

If you are looking for a tactical allocation to equity, debt, and gold, investing in a Multi-Asset Fund would also be a meaningful choice now.

[Read: Why Investing in Multi-Asset Allocation Funds Makes Sense Now]

Following a prudent asset allocation as per your risk profile and envisioned financial goals, paves the way to financial success in the long run. Don't let Donald Trump's triumph get in the way of your sensible investing.

Be a thoughtful investor.

Happy Investing!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. Registration granted by SEBI, Membership of BASL and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

Mutual Fund investments are subject to market risks, read all scheme-related documents carefully.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and use such independent advisors as he believes necessary.