RBI Cuts Rates Again! What Debt Market Investors Should Know

Rounaq Neroy

Apr 12, 2025 / Reading Time: Approx. 10 mins

Listen to RBI Cuts Rates Again! What Debt Market Investors Should Know

00:00

00:00

In the months preceding the April 2025 policy review, clear signs of a rate cut were emerging. Both domestic and global economic data indicated a softer interest rate environment, leading investors, economists, and bond market participants to price in the cut early.

The Monetary Policy Committee (MPC) held its 54th meeting and the first of the financial year 2025-26 from April 7th to 9th under the chairmanship of Shri Sanjay Malhotra, Governor, Reserve Bank of India. The MPC members Dr Nagesh Kumar, Shri Saugata Bhattacharya, Prof. Ram Singh, Dr Rajiv Ranjan, and Shri M. Rajeshwar Rao attended the meeting.

"After a detailed assessment of the evolving macroeconomic and financial conditions and outlook, the MPC voted unanimously to reduce the policy repo rate by 25 basis points to 6.00% with immediate effect," said Sanjay Malhotra.

This is his second significant policy announcement as RBI Governor, who took office in December 2024. The RBI said it would keep the system in surplus liquidity.

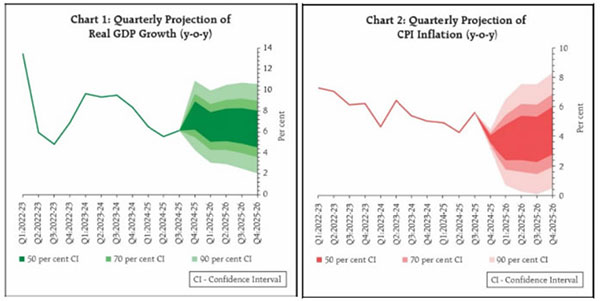

Graph: RBI's Quarterly Projection of GDP Growth & CPI Inflation

(Source: Monetary Policy Statement, 2025-26, April 7 to 9, 2025)

(Source: Monetary Policy Statement, 2025-26, April 7 to 9, 2025)

With inflation appearing to moderate, aided by a sharp drop in food prices, the RBI believes it can facilitate growth, especially since it is increasingly confident that inflation will be aligned with the 4% target. Given the moderate recovery amid global uncertainties, the MPC unanimously cut the repo rate by 25 bps to 6.00% and shifted its stance from neutral to accommodative, while stressing the need for continued vigilance.

The six-member MPC decided to heighten uncertainty in the global market following the recent announcement of reciprocal tariffs by US President Donald Trump. The rate cut has come in the wake of fears that higher tariff rates may lead to inflation, an increase in trade tensions and lower growth in the world economy.

"Global economic outlook is fast changing. FY26 has started on an anxious note and some global trade frictions are coming true," the RBI Governor said.

Table: Repo Rate Cuts in the Past Decade

| Effective Date |

Repo Rate |

% Change |

| 09 April 2025 |

6.00% |

0.25% |

| 07 February 2025 |

6.25% |

0.25% |

| 06 December 2024 |

6.50% |

- |

| 18 September 2024 |

6.50% |

- |

| 08 June 2023 |

6.50% |

- |

| 08 February 2023 |

6.50% |

0.25% |

| 07 December 2022 |

6.25% |

0.35% |

| 30 September 2022 |

5.90% |

0.5% |

| 05 August 2022 |

5.40% |

0.5% |

| 08 June 2022 |

4.90% |

0.5% |

| 04 May 2022 |

4.40% |

0.4% |

| 09 Oct 2020 |

4.00% |

0.00% |

| 06 Aug 2020 |

4.00% |

0.00% |

| 22 May 2020 |

4.00% |

0.40% |

| 27 March 2020 |

4.40% |

0.75% |

| 06 February 2020 |

5.15% |

0.25% |

| 07 August 2019 |

5.40% |

0.35% |

| 06 June 2019 |

5.75% |

0.25% |

| 04 April 2019 |

6.00% |

0.25% |

| 07 February 2019 |

6.25% |

0.25% |

| 01 August 2018 |

6.50% |

0.25% |

| 06 June 2018 |

6.25% |

0.25% |

| 02 August 2017 |

6.00% |

0.25% |

| 04 October 2016 |

6.25% |

0.25% |

| 05 April 2016 |

6.50% |

0.25% |

| 29 September 2015 |

6.75% |

0.50% |

| 02 June 2015 |

7.25% |

0.25% |

| 04 March 2015 |

7.50% |

0.25% |

| 15 January 2015 |

7.75% |

0.25% |

Data as of April 11, 2025

(Source: RBI, data collated by PersonalFN Research)

The RBI has reduced policy rates by a total of 50 basis points in 2023, leading to banks transmitting the rate cut in the coming quarters. When the RBI reduces the repo rate, it reduces borrowing costs for banks, and in turn, banks will reduce their lending rates on loans like home, personal, or business loans.

[Read: Will RBI Cut the Policy Repo Rate Again in April 2025 as CPI Inflation for February Falls]

Borrowers with floating-rate loans that are coupled to external benchmarks, like the repo rate, may see a reduction of EMIs and may have cheaper new loans. However, a decline in the repo rate will reduce the banks' margins if they are only able to pass on reductions in lending rates, without a corresponding reduction in funding costs.

Furthermore, the lower repo rates will also reduce effective interest rates on deposits, which are particularly seen in fixed deposits and recurring deposits. Banks, able to borrow at lower rates, will have less incentive to offer higher interest rates on deposits, which means lower returns for conservative investors, especially in fixed deposits.

Rate cuts are often associated with lower lending rates, as well as lower deposit rates, which has an impact on the market-especially on the debt market.

Everything from bond yields to debt mutual funds, the RBI's monetary policy decision propagates into the fixed income space, and this can affect both incursions and long-term funding strategies.

When the RBI cuts rates, should debt investors cheer or worry?

Imagine this: You've invested your money into a debt mutual fund or fixed-income instrument with the expectation of getting your returns in a closer to predictable way. Then the headlines shout "RBI slashes repo rate again!".

For a retail investor, this will cause some confusion and curiosity. Is this a hint that your debt investments will do well? Or is it the right time to rebalance your portfolio?

In the world of investing, few events may shake up your investments, nothing is quite like a rate cut by the RBI. Although events such as rallies and crashes in the stock market are visible in real-time on your screens, a rate cut plays out more under the radar but with just as much impact, on debt trades.

So before going into the implications for your investment, let's talk about why everyone from economists to equity analysts is trying to guess the RBI's next move.

[Read: Will Debt Mutual Fund Returns Improve After RBI's Latest Bi-Monthly Monetary Policy]

Changes (cuts or hikes) in the interest rate by the central bank are not random moves. They are calculated events based on inflation trends, economic growth, global financial conditions and even fiscal action.

When the economy shows signs of slowing down like lower GDP growth, sluggish consumption, or global headwinds the RBI often steps in with a rate cut. The idea is simple: lower interest rates reduce borrowing costs, boost business activity, and inject momentum into the economy.

RBI's Latest Rate Cut in April 2025: A Signal or a Series?

It was no surprise that RBI reduced the repo rate by 25 basis points to 6.00%, but a confirmation. The central bank already suggested that it was in 'accommodative mode,' and with inflation being addressable and GDP growth flat, every market participant had expected this cut.

But it's not about this cut. It's about what comes next.

Is this the beginning of an extended rates-easing cycle? Will the RBI go further to spur demand and private investment? And what does this mean for your debt mutual funds, fixed deposits, and bond investments?

Impacts on Your Debt Market Investments.

1. Rising Bond Prices, Better Gains for Existing Holders

A rate cut makes newly issued bonds offer lower coupon rates. In contrast, older bonds locked in at higher rates become more valuable in the secondary market. As demand for these older, higher-yielding bonds rises, so do their prices.

Investors who sell these bonds stand to gain through capital appreciation, while those who hold them enjoy relatively better returns in a falling-rate environment.

2. Longer Duration Bonds Gain the Most

Not all bonds react the same way to a rate cut. Long-term bonds, which mature over a longer horizon, are more sensitive to interest rate movements. This means that when rates drop, these bonds tend to see sharper price gains. For investors seeking to capitalize on this opportunity, allocating to long-duration instruments could enhance overall returns, especially when a prolonged easing cycle is expected.

3. Debt Mutual Funds See NAV Upside

Debt mutual funds, particularly those with medium- to long-duration profiles, benefit significantly when bond prices rise. The value of the fund's underlying holdings increases, pushing up the Net Asset Value (NAV). Funds like dynamic bond funds, gilt funds, and income funds may perform particularly well in this environment.

As returns from traditional fixed-income instruments like FDs decline, more investors are likely to shift towards these funds in search of better yields.

4. Corporate Bond Activity Gets a Boost

Lower policy rates translate into cheaper borrowing for businesses. As a result, companies often ramp up their bond issuances to raise capital at reduced costs. This trend becomes more visible in an accommodative rate regime, like in April 2025, where Indian corporates could raise billions through bonds to fund growth and refinance older, costlier debt.

For fixed-income investors, this also means a wider basket of corporate bond offerings to choose from.

5. Shifting Investor Preferences

When interest rates decline, it changes how investors think about their portfolios. With bank deposit rates being relatively low, traditional instruments are less appealing. Investors (especially those looking for fixed income) may venture into higher-quality corporate bonds, debt mutual funds, and/or target maturity funds. The supply and demand dynamic in the debt market will also shift, which will likely increase trading volumes and shift allocations away from short-duration debt to longer-dated debt.

For investors, especially those looking at building a balanced fixed-income portfolio, this also calls for reconsideration and repositioning of the debt portfolio. However, it is important to do this wisely, not strictly looking for returns, but on your expectations, time horizon, and risk appetite.

-

Medium Term (3-5 Years):

Choose medium-to-long duration funds, especially those with about 30% G-sec exposure, because lower rates result in capital appreciation. If rates fall, it supports capital appreciation. Invest in a staggered manner using SIP or staggered lump sums to manage timing risk.

-

2-3 Year Horizon:

Consider Banking & PSU Debt Funds for stability and quality. Up to one-third (30%) of your debt portfolio can be allocated to Banking & PSU Debt Funds, since most of their portfolios will be high-rated government and quasi-government securities.

-

Short Term (1-2 Years):

Stick with Ultra-Short or Short Duration Funds that emphasize safety. Prioritize schemes with high government/PSU allocation and minimal private issuer exposure to protect capital.

-

Very Short Term (Up to 1 Year):

Use Liquid Funds to park money safely. Choose those with low or no exposure to private credits. They're more flexible than FDs and offer slightly better returns without extra risk.

SIPs in Debt Mutual Fund?

SIPs are best used for volatile investments in which the prices fluctuate can help average out your cost over time. However, that advantage does not hold for short-duration debt funds where the NAVs are stable.

If you invest in longer-duration debt funds as Gilt Funds, Dynamic Bond Funds are Medium-to-long duration funds, SIPs can work well because they allow you to ride through interest-rate cycles and smoothen the investment journey.

On the contrary, if you invest in short-duration funds like Liquid Funds, Ultra Short Duration Funds, or Money Market Funds, SIPs don't add much value. With limited price movement, a lump sum investment is helpful and often preferred.

Finally, keep in mind that league debt fund returns on SIPs will never be a match for long-term equity fund returns. The goal of the debt fund storyline is consistency, stable income, and capital preservation, not necessarily growth.

However, if you still prefer bank fixed deposit (FD), ensure it is locked into current good rates before the banks lowered them, since some banks on March 5 2025, raised their interest rates lower, with thirty basis points from the 25 bps policy repo rate cut in February 2025.

To Conclude...

From an outlook perspective, if the RBI has reduced the repo, it may indicate a shift to a slightly more accommodative position. However further rate reductions will depend on how the inflation and other global uncertainties evolve. For debt fund investors, this will require flexibility and a keen eye on your investment horizon.

You may consider a balanced, quality-focused approach with short or long-duration funds to navigate this interest rate environment considerately. Keep an eye on policy signals, but don't let noise work against you to disrupt your plans for the future.

We are on Telegram! Join thousands of like-minded investors and our editors right now.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.