RBI Keeps Policy Rates Unchanged Again! Here’s How to Approach Debt Mutual Funds Now

Rounaq Neroy

Aug 10, 2023 / Reading Time: Approx. 7 mins

Listen to RBI Keeps Policy Rates Unchanged Again! Here’s How to Approach Debt Mutual Funds Now

00:00

00:00

The Reserve Bank of India (RBI) for the third successive time has kept the policy repo rate under the Liquidity Adjustment Facility (LAF) unchanged at 6.50% in its August 2023 bi-monthly monetary policy 2023-24 meeting today.

The six-member Monetary Policy Committee (MPC) also decided to remain focused on the withdrawal of accommodation to ensure that inflation progressively aligns with the target, while supporting growth.

On the policy rate decision, all six members of the MPC unanimously voted in favour of this decision. However, as regards the stance of the monetary policy, Prof. Jayanth R. Varma expressed reservations.

The Standing Deposit Facility (SDF) rate -- which absorbs excess liquidity -- also remained unchanged at 6.25% and the marginal standing facility (MSF) rate (which is a window for banks to borrow from the RBI in an emergency, when inter-bank liquidity dries up) and the Bank Rate (at which RBI lends money to commercial banks for short-term loans) at 6.75%.

Table: RBI Monetary Policy Actions and Stance

| Month |

Repo Policy Rate |

Policy Action

(Basis points) |

Monetary Policy Stance |

| Feb-2019 |

6.25% |

-25 |

Neutral |

| Apr-2019 |

6.00% |

-25 |

Neutral |

| Jun-2019 |

5.75% |

-25 |

Accommodative |

| Aug-2019 |

5.40% |

-35 |

Accommodative |

| Oct-2019 |

5.15% |

-25 |

Accommodative |

| Dec-2019 |

5.15% |

Status quo |

Accommodative |

| Feb-2020 |

5.15% |

Status quo |

Accommodative |

| Mar-2020 (an exceptional off-cycle meeting) |

4.40% |

-75 |

Accommodative |

| May-2020 (an exceptional 2nd off-cycle meeting) |

4.00% |

-40 |

Accommodative |

| Aug-2020 |

4.00% |

Status quo |

Accommodative |

| Oct-2020 |

4.00% |

Status quo |

Accommodative |

| Dec-2020 |

4.00% |

Status quo |

Accommodative |

| Feb-2020 |

4.00% |

Status quo |

Accommodative |

| April-2021 |

4.00% |

Status quo |

Accommodative |

| June-2021 |

4.00% |

Status quo |

Accommodative |

| Aug-2021 |

4.00% |

Status quo |

Accommodative |

| Oct-2021 |

4.00% |

Status quo |

Accommodative |

| Dec-2021 |

4.00% |

Status quo |

Accommodative |

| Feb-2022 |

4.00% |

Status quo |

Accommodative |

| Apr-2022 |

4.00% |

Status quo |

Accommodative |

| May-2022 (Off-cycle meeting) |

4.40% |

+40 |

Accommodative |

| June-2022 |

4.90% |

+50 |

Focus on withdrawal of Accommodative stance |

| Aug-2022 |

5.40% |

+50 |

Focus on withdrawal of Accommodative stance |

| Sep-2022 |

5.90% |

+50 |

Focus on withdrawal of Accommodative stance |

| Dec-2022 |

6.25% |

+35 |

Focus on withdrawal of Accommodative stance |

| Feb-2023 |

6.50% |

+25 |

Focus on withdrawal of Accommodative stance |

| Apr-2023 |

6.50% |

Status quo |

Focus on withdrawal of Accommodative stance |

| May-2023 |

6.50% |

Status quo |

Focus on withdrawal of Accommodative stance |

| Aug-2023 |

6.50% |

Status quo |

Focus on withdrawal of Accommodative stance |

Data as of August 10, 2023

(Source: RBI Monetary Policy Statements, Data collated by PersonalFN Research)

These decisions were in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4.0% within a band of +/- 2.0%, while supporting growth.

Inflation is a concern...

The overall monetary policy decision was in line with the market expectation, given that CPI inflation after hitting a low of 4.3% in May 2023, rose once again in June 2023 to 4.8% largely led by food group dynamics on the back of higher prices of vegetables, eggs, meat, fish, cereals, pulses and spices. Core inflation -- which excludes food and fuel inflation -- was also steady at 5.1%.

The RBI Governor in his statement to the media opined that a heightened vigil on the evolving inflation trajectory was warranted. He said possible El Nino weather conditions along with global food prices need to be watched closely against the backdrop of a skewed south-west monsoon so far. Also, he envisaged a surge in inflation in July and August 2023 led by vegetable prices (as torrential rainfalls in many parts of the country have damaged crops).

Going forward, the risk to the inflation trajectory according to the RBI emanates from...

-

✓ The spike in vegetable prices led by tomatoes.

-

✓ The impact of the uneven rainfall distribution (and possible El Nino conditions).

-

✓ Upward pressures on global food prices due to geopolitical hostilities

-

✓ Firming up of crude oil prices amidst production cuts

-

✓ And an expected increase in output prices (as revealed by manufacturing, services and infrastructure firms polled in the Reserve Bank's enterprise survey).

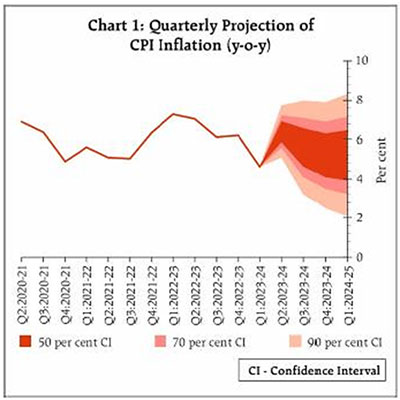

Considering these factors and assuming a normal monsoon, the RBI projected CPI inflation to be at 5.4% for 2023-24 (with Q2 at 6.2%, Q3 at 5.4% and Q4 at 5.2%, with risks evenly balanced), which is higher compared to 5.1% projected in its June 2023 bi-monthly monetary policy statement for the fiscal year 2023-24. For the fiscal year 2024-25 first quarter (Q1:2024-25), CPI inflation is projected at 5.2%.

Graph: RBI's quarterly projection of CPI Inflation

Data as of August 10, 2023

Data as of August 10, 2023

(Source: RBI 3rd bi-monthly Monetary Policy Statement 2023-24)

The cumulative rate hike of 250 basis points undertaken by the MPC is transmitting through the economy and its fuller impact should keep inflationary pressures contained in the coming months, but the RBI is prepared to undertake policy responses, should the situation so warrant.

The growth outlook is positive, but...

Speaking about the growth outlook, the RBI is of the view that the recovery in kharif sowing and rural incomes, the buoyancy in services and consumer optimism should support household consumption.

Besides, for the capex cycle which is showing signs of getting broad-based, the healthy balance sheets of banks and corporates, supply chain normalisation, business optimism and robust government capital expenditure are favourable.

But the headwinds from weak global demand, volatility in global financial markets, geopolitical tensions and geoeconomic fragmentation do pose a risk to the economic growth outlook.

Thus, considering all these factors, real GDP growth for 2023-24 is projected at 6.5% (with Q1 at 8.0%; Q2 at 6.5%; Q3 at 6.0%; and Q4 at 5.7%), with risks broadly balanced. Real GDP growth for Q1:2024-25 is projected at 6.6%.

What should be your strategy to invest in debt mutual funds now?

The RBI has chosen to remain focused on the withdrawal of accommodation to ensure that inflation progressively aligns with the target while supporting growth. The MPC will maintain a close vigil on the evolving inflation scenario and remain resolute in its commitment to aligning inflation to the target and anchoring inflation expectations. If CPI inflation moves up and worries the RBI, maybe another 25-35 bps policy rate could go up later in the year. Having said that, it appears that we are almost near the peak of the interest rate upcycle.

Now would be an opportune time to invest in longer-duration debt mutual funds with a medium-term view of 3 to 5 years whereby you benefit from higher yield and unlock the capital growth.

Typically, one can consider Medium to Long Duration Debt Funds, Long Duration Funds, Gilt Funds, and Dynamic Bond Funds in the current interest rate cycle by assuming slightly higher risk and keeping a time horizon of 2 to 3 years or more. But it is best to invest in these funds in a staggered manner.

For those who can't afford to take slightly high risk and/or the investment horizon is very short (a few days, weeks or a few months), Overnight Funds, Liquid Funds, Ultra Short Duration Funds, and/or Money Market Funds could be considered.

Don't just invest in debt mutual funds randomly, and don't be discouraged by the new tax rule for debt mutual funds, wherein the capital gains on selling debt mutual funds units, irrespective of Short Term Capital Gain (STCG) or Long Term Capital Gain (LTCG) will be taxed at the marginal rate of taxation, i.e. as per one's income-tax slab.

[Read: Does it Make Sense to SIP in Debt Mutual Funds?]

Even now debt mutual funds have an edge over bank fixed deposits as regards returns are concerned. To make the best choice among the plethora of schemes available within the respective sub-categories of debt funds, all one must do is evaluate a host of quantitative and qualitative parameters such as the following:

-

✓ The credentials and experience of the fund management team

-

✓ The AUM and expense ratio of the scheme

-

✓ The portfolio characteristics (who are the issuers, the sector they belong to, the type of debt papers held, the ratings of the respective debt papers, etc.)

-

✓ The maturity profile of the fund

-

✓ Returns across time periods (3 months, 6 months, 1 year, 2 years, 3 years, and so on)

-

✓ The risk ratios (Standard Deviation, Sharpe Ratio, Sortino Ratio, etc.)

-

✓ The current interest rate cycle

-

✓ The performance across interest rate cycles

Plus, it would be better to understand the investment ideologies, processes, and systems followed at the mutual fund house.

In the evaluation process, if the mutual fund house lacks a robust risk management framework and depends excessively on ratings assigned by credit rating agencies, the fund manager compromises on the quality of the portfolio, chases yields, and plays down on the liquidity aspects of the portfolio, one should be concerned.

Want to know which are the Best Debt Mutual Funds to Invest in 2023? Click here.

Avoid picking debt mutual fund schemes looking at just the past returns, as they are in no way indicative of the future performance of the scheme.

Be a thoughtful investor and follow a holistic approach to make the best choice among the debt mutual fund schemes.

Happy Investing!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.