Sovereign Gold Bonds Up for Premature Redemptions. What Should Investors Do?

Rounaq Neroy

Apr 21, 2025 / Reading Time: Approx. 7 mins

Listen to Sovereign Gold Bonds Up for Premature Redemptions. What Should Investors Do?

00:00

00:00

The Reserve Bank of India (RBI) has announced a premature redemption window for several series of Sovereign Gold Bonds (SGBs).

SGBs were initially launched in November 2015 by the government with the objective of borrowing and was part of the gold monetisation scheme -- aimed at reducing the physical demand for gold in India, encourage financialization of savings, and channelling idle gold for the productive use of the economy.

Investors were assured of the market value of gold at the time of maturity and periodical interest (at 2.50% fixed rate) payable/credited semi-annually to the bank account of the investor and the last interest will be payable on maturity along with the principal.

Premature redemption of SGBs is permitted after the fifth year from the date of issue of such gold bond, while the full term or tenor of these bonds is 8 years.

Now with the surge in price per gram of gold (999 purity), the government has decided to discontinue SGBs and prematurely redeem them, considering the high borrowing cost.

The last tranche of SGB was offered in February 2024 at an issue price of Rs 6,263 per gram and today (as of April 16, 2025) the price per gram of gold (for 999 purity) is Rs 9,457 -- that's an absolute return of +51.0% in little over a year.

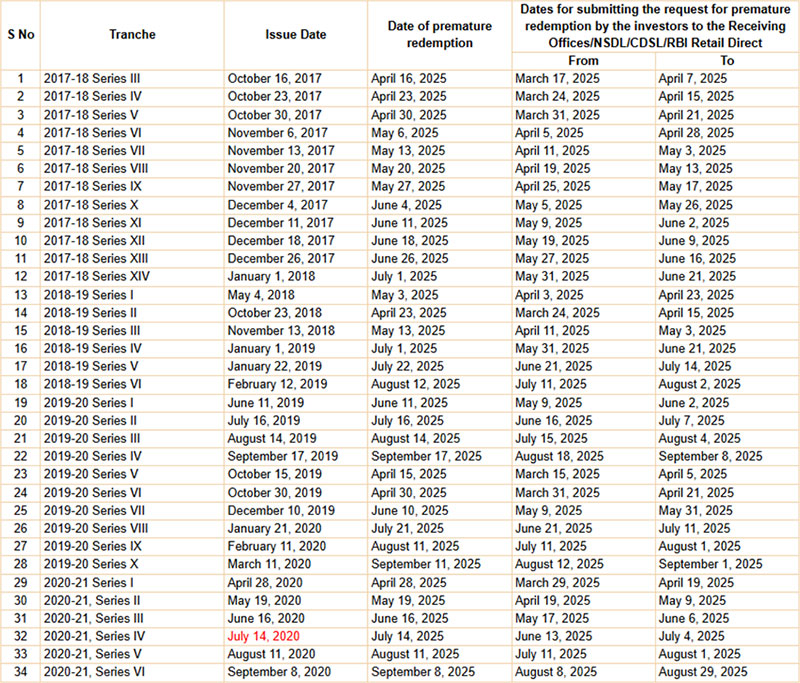

Table 1: Scheduled Premature Redemption of SGBs (April to September 2025)

(Source: RBI Press Release)

(Source: RBI Press Release)

Recently the SGB 2017-18 Series III (issued on October 16, 2017, at Rs 2,964 per unit) was redeemed on April 16, 2025, at a price of Rs 9,221 per unit of SGB (based on the simple average of closing price of 999 purity gold for the three business days i.e., April 09, April 11, and April 15, 2025, published by the India Bullion and Jewellers Association Ltd.).

Before that, on April 15, 2025, the SGB 2019-20 Series V (issued on October 15, 2019, at Rs 3,788 per unit) was prematurely redeemed at a price of Rs 9,069 per unit of SGB (based on the simple average of the closing price of 999 purity gold for the three business days i.e., April 08, April 09, and April 11, 2025.)

Given this, investors in SGB 2017-18 Series III and SGB 2019-20 Series V have made handsome capital gains. Thanks to gold exhibiting its sheen amidst the looming geopolitical and macroeconomic uncertainties. And if we consider the bi-annual interest, the total returns earned are even more attractive.

Table 2: Investors Have Struck Gold in SGBs

|

SGB 2017-18 Series III |

SGB 2019-20 Series V |

| Issue Date |

16-Oct-25 |

15-Oct-25 |

| Issue Price (Rs per unit) |

2,964 |

3,788 |

| Premature Redemption Date |

16-Apr-25 |

16-Apr-25 |

| Premature Redemption Price (Rs per unit) |

9,221 |

9,069 |

| Absolute Returns |

211% |

139% |

| CAGR |

25% |

19% |

(Source: RBI, data collated by PersonalFN Research)

Going forward, as per the RBI's premature redemption schedule for SGBs, two more SGBs will be redeemed in April 2025: SGB 2027-18 Series IV and Series V.

In the ensuing months as well, many more SGBs are scheduled for premature redemptions. Given that gold has scaled up and exhibited its sheen, investors would be earning appealing returns.

Note that if you, the investor, choose to hold SGBs until their full tenure of 8 years the redemption amount will be as per the price of gold (999 purity) at that time, and you shall continue earning interest maturity.

What Should Investors Do?

In the last five years, particularly after the COVID-19 pandemic, gold has seen a remarkable run-up. The present elevated price of gold allows you to benefit from the premature redemption of SGBs.

Graph: Gold Has Exhibited Its Sheen in the Long Term

Data as of April 16, 2025.

Data as of April 16, 2025.

(Source: MCX, data collated by PersonalFN Research)

If you have been already investing in gold and your allocation has exceeded 10-15% of your portfolio amidst the rally it would be prudent to redeem/book profit to bring back the portfolio to the desired allocation.

The SGB units can be tendered for premature redemption, reach out to your bank, post office, or broker/agent through whom you originally purchased the SGBs.

That said, if your exposure to gold is well within the aforesaid allocation, then maybe you could consider holding on to your SGBs (a smart avenue to invest in gold) until the full maturity of 8 years.

A fact is unlike financial assets, gold is a real asset -- meaning gold does not carry credit or counterparty risk.

You see, even a stronger U.S. Dollar (USD) typically seen during the stagflation period hasn't dampened the sentiments toward gold, according to the WGC. The Trump 2.0 administration ostensibly favouring a weak USD and the uncertain effects of tariffs could serve as a tailwind for gold.

Against the backdrop of trade wars, heightened geopolitical risk, and its repercussions on global economic growth, inflation and financial markets, it makes sense to have some tactical allocation to gold.

In the past as well, i.e. in CY2019, CY2020, CY2022, CY2024 when we witnessed the pandemic, wars, and military conflict and geopolitical tension in many parts of the world, gold has exhibited its sheen.

One needs to consider the long-term uptrend exhibited by gold (see the graph above). Even central banks of the world, recognising the looming risks (macroeconomic and geopolitical) are buying gold strategically as a part of their reserve management.

The World Gold Council (WGC) has also expressed that given gold's strategic significance and the economic uncertainties that continue to look ahead, investors should carefully consider the portfolio benefits gold can offer in 2025 and beyond.

So, despite the discontinuation of Sovereign Gold Bonds (SGBs), gold continues to be a good investment option.

The Tax Implications of Sovereign Gold Bonds

Keep in mind that, the interest on the bonds will be taxable as per the provisions of the Income-tax Act, 1961 (43 of 1961). The interest is taxable under the head 'Income from Other Sources' as per your applicable income tax slab, i.e., at the marginal rate of taxation.

As regards, the proceeds from the premature redemption of SGBs through the RBI window (available after five years of holding) are exempt from Long Term Capital Gains Tax, as per the current tax rule.

However, if you miss this window and sell the SGBs in the secondary market, they will be subject to capital gains tax (plus the surcharge and health and education cess as applicable).

Hence, if you are considering redeeming SGBs, either utilise the premature redemption window made available by the RBI or then hold until the maturity period of 8 years to save from the axe of tax.

If you hold the SGBs until their full maturity period of 8 years, the resulting capital gains will be exempt from tax, as they are not considered a transfer for capital gains.

Note, that it is your responsibility as a SGB holder to comply with the tax laws.

Make sure to be thoughtful in your approach.

Happy Investing!

We are on Telegram! Join thousands of like-minded investors and our editors right now.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.