Why You Should Invest in PPF Even If You Have an EPF Account

Mitali Dhoke

Dec 06, 2022 / Reading Time: 11 mins

Listen to Why You Should Invest in PPF Even If You Have an EPF Account

00:00

00:00

Retirement is one of the most crucial phases of life. As it will take several years to build the desired retirement corpus, one should start retirement planning in the early stages of life while working to relish a peaceful life post-retirement. Among all the envisioned financial goals, retirement is the most important one.

When you're in your 20s, retirement seems so far off that many of you delay planning for your sunset years. While it's true that you should seize every moment and make the most of your present, at the same time, it is crucial to plan for the security of your future. Once you attain the retirement age, i.e., 60 years, you will no longer be earning regularly (in the form of salary or business and profession); thus, it will leave you dependent on the investments made earlier to meet your retirement expenses.

Your financial decisions today will influence your lifestyle post-retirement. As a result, one should carefully plan and choose investment option for retirement that best suits their needs and objectives. The earlier you plan, the better returns you would expect on your savings or investments.

[Read: Retirement Calculator]

For retirement planning, there are various investment avenues like NPS, ULIPs, Bank FDs, mutual funds, etc. Still, among them, the Public Provident Fund (PPF) and Employees Provident Fund (EPF) are the most popular ones. Let's review these two well-known government-backed retirement savings scheme options:

What is Employees Provident Fund (EPF)?

Employee Provident Fund (EPF) is launched under the supervision of the Government of India. The Ministry of Labour regulates EPF schemes in India under the Employee Provident Fund and Miscellaneous Provisions Act 1952. Employee Provident Fund Organisation (EPFO) manages this savings scheme. EPF aims to build a sufficient retirement corpus for an individual and inculcates the habit of saving money for salaried employees.

An individual working in an organisation having 20 or more permanent employees (across different departments and branches) may be entitled to provident fund benefits and holding an EPF Account.

EPF is a compulsory deduction from the salaries of employees working in eligible organisations. Every company registered with the EPFO will assign an EPF account number to their employees, which is an alphanumeric code. It represents the state, regional office, establishment, and EPF member code. On the other hand, Universal Account Number (UAN) is a unique number allotted to EPF members. Every time an employee changes their job, their EPF account number related to the employer changes; however, the UAN number remains the same.

EPF includes monetary contributions from both employer and employee. The actual amount of EPF contribution is calculated based on the employee's salary (Basic + Dearness allowance). Once an individual retires, they receive the total contribution (of both employee and employer) as a lump sum with interest. The rate of return earned is fixed which is set by EPFO.

How is Employee's contribution towards EPF calculated?

The employer directly deducts 12% from the employee's salary (basic + dearness allowance) every month for a contribution towards EPF. This entire contribution goes to the EPF account of the employee.

How is the Employer's contribution towards EPF calculated?

Similarly, the employer also contributes 12% of the employee's salary towards EPF. But the employer's contribution is spread across various categories as follows:

| EPF Contribution Rate 2022 |

| Category |

Contribution Percentage (%) |

| Employees Provident Fund |

3.67% |

| Employee Pension Scheme (EPS) |

8.33% |

| Employee's Deposit Link Insurance Scheme (EDLIS) |

0.5% |

Moreover, the employer also bears certain administration costs towards EDLI and EPF.

However, EPF contribution by the employer can be 10% in certain circumstances, as stated below:

-

If a company has less than 20 employees

-

The company incurs losses that are more than its entire net worth

-

If a company is associated with the beedi, jute, brick, guar gum or coir industry.

Image source: www.freepik.com

Image source: www.freepik.com

Join Now: PersonalFN is now on Telegram. Join FREE Today to get 'Daily Wealth Letter' and Exclusive Updates on Mutual Funds

Additionally, the contribution varies in the case of women employees. As per the Union Budget 2018-2019, new women employees can make an EPF contribution of 8% instead of 12%. This privilege is only for the first 3 years of employment.

[Read: EPF Calculator]

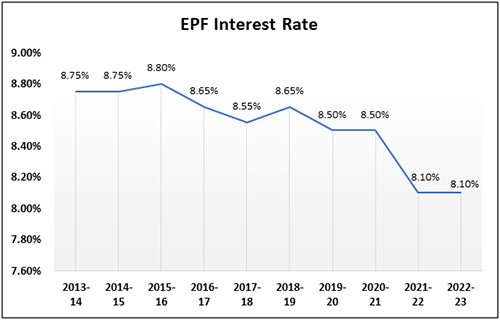

Interest Rate on Employees Provident Fund (EPF):

The Interest rate of EPF is reviewed on an annual basis after consultation with the Ministry of Finance by EPFO's Central Board of Trustees. The EPF interest rate for the fiscal year 2022-23 is 8.10%.

Graph: Decline in EPF Interest Rate (Past 10 years historical data)

(Data as on December 06, 2022)

(Data as on December 06, 2022)

(Source: EPFO)

Do note, although the interest is calculated monthly, it is only deposited to the EPF account once a year on March 31st of the applicable fiscal year. As you can see from the graph above, the EPF interest rate has been on a decline. The government may increase/decrease EPF interest rates in future in accordance to the changes in the RBI policy rates and bond yields.

However, for many salaried individuals, EPF is the cornerstone of their retirement planning, and often a question arises in their mind that - If we already have an EPF Account, is it worth opening and investing in a PPF account?

Well, considering the decline in EPF interest rates in recent years, you can't solely count on EPF investments for your retirement needs. While planning investment options for retirement, key factors that require attention are inflation (silent killer of your funds or savings), rising cost of living and anticipated higher medical treatment costs in future. Thus, it will be prudent to consider an additional investment avenue like PPF for building a robust retirement corpus.

In order to plan for your retirement effectively, you need to consider both the EPF Account as well as the PPF Account and make meaningful contributions to them (along with other investment avenues, viz. NPS, SIP in mutual funds, bank deposits, gold, etc.). This can prove to be a meaningful strategy that shall enable you to build a respectable retirement corpus and enjoy financial independence during the golden years of your life.

What is Public Provident Fund (PPF)?

PPF is another popular government-backed scheme with a fixed rate of return, traditionally better than bank FDs. PPF interest rate is linked to 10-year G-Sec yield. It is a long-term small saving scheme of the Central Government framed under the PPF Act of 1968. PPF is open to all Indian citizens residing in the country; it not just provides retirement security but even helps plan for other long-term financial goals, such as your child's future needs, viz., higher education and wedding expenses.

The PPF Account can even be opened in your minor child's name through a legal guardian. However, as per the PPF rules, the PPF Account cannot be held jointly, only one PPF Account per individual is permitted. A PPF account's balance enjoys a fixed interest rate throughout its tenure. However, the rate of interest is subject to revision by the Indian government every quarter.

While the government recently increased the interest rates of certain small savings schemes, the PPF interest rate was unchanged for the quarter ending December 31, 2022, the PPF will earn an interest rate of 7.1%.

Below are the features of the PPF Account:

-

Eligibility: The applicant should be an Indian resident

-

Tenure: 15 years, and on completion of 15 years, the account can be extended in a block of 5 years.

-

Minimum Investment: Rs 500 p.a. in a financial year (mandatory)

-

Maximum Investment: Rs 1.5 lacs p.a. (any number of deposits in multiples of Rs 50 in a financial year).

-

Access to PPF account: Any Post Office and some authorised branches of Banks

-

Who cannot invest: Hindu Undivided Family (HUF); Non-Resident Indians (NRIs); and Person of Foreign Origin

-

Mode of Payment: Cash/Crossed Cheque/Demand Draft/ Pay Order/Online Transfer in favour of the Accounts Officer.

-

Premature closure: Allowed but after the expiry of 5 full financial years from the end of the year in which your initial subscription was made and subject to certain conditions

-

Nomination: Available

-

Partial Withdrawals: Permitted

What are the Tax Implications of EPF and PPF?

The EPF and PPF contributions are eligible for tax deductions under the provisions of Section 80C of the Income Tax Act, 1961. In the case of EPF, annual contributions only up to Rs 2.50 lacs will earn you tax-free interest; beyond that, the interest earned is fully taxable. In comparison, your contributions to your PPF Account are eligible for a deduction of only up to Rs 1.50 lacs per financial year.

In addition, the maturity proceeds on the total investment are tax-free, and the withdrawal (including partial withdrawals) is exempt from tax. In other words, EPF and PPF enjoy an Exempt-Exempt-Exempt (E-E-E) tax status. Moreover, the money in the PPF Account remains safe and yours for life, and it cannot be attached by the order or decree of the court in case of any debt or liabilities, as per the PPF rulebook.

Since interest on both EPF and PPF schemes is tax-free, this will help you accumulate good funds without paying any tax on the income earned on these investments year after year.

Should you consider investing in a PPF Account?

Both EPF and PPF come with their set of pros and cons. In my opinion, to accumulate a sizeable corpus for your retirement, it is absolutely an excellent strategy to invest in both EPF and PPF, as both schemes help you achieve your long-term financial goals, especially your retirement.

The fact that EPF is transferable across employers, and you don't have to go through the hassle of depositing the money from your savings account as it is deducted directly from your salary is one significant benefit. On the other hand, PPF offers much flexibility to investors as you can contribute at your convenience. However, the lock-in period of 15 years might sometimes seem too long, but if you are aiming for your retirement, then it is a wise choice. You can also avail loan against the balance in your PPF account.

Therefore, PPF seems to be a worthwhile investment option for your retirement. You should consider opening a PPF Account and make meaningful contributions to it even though you already own an EPF account.

Happy Investing!

Warm Regards,

Mitali Dhoke

Research Analyst