Should You Buy Family Health Insurance This Festive Season?

Listen to Should You Buy Family Health Insurance This Festive Season?

00:00

00:00

Last year the festive season was restrained as many states across India were under complete lockdown due to the COVID-19 pandemic. But now people have gotten habituated to living with the virus and following safety norms, and cannot wait to celebrate this festive season with their friends and families.

But since we are celebrating in such challenging times this year, why not think of gifting your loved ones something different yet beneficial. If you are wondering what could be a thoughtful gift, then there is no better option than a family floater health insurance policy.

Why is a Family Floater Health Insurance Policy important?

The steady rise in the cost of raw materials and import duties, increased demand for advanced medicines and treatments are the main reasons for the medical inflation in India. As you may know, medical tourism is booming, with people coming from all over the world to India for primary as well as advanced medical treatments because they find the best healthcare services at affordable prices. This is another reason why the cost of healthcare services are on the rise.

Health and health insurance awareness in India has been a concern for many years. But, the current pandemic has been an eye-opener; people have started realising the importance of clean eating, drinking an adequate amount of water, daily exercising, and securing themselves and their families with health insurance.

Although health insurance may just be the best gift this festive season, one should make an informed decision while choosing the right health insurance plan.

Read on to know how you can choose the best-suited family health insurance plan this festive season.

(Image source: freepik.com)

What is Family Floater Health Insurance?

-

As the name suggests, family floater health insurance is a health insurance plan specifically made to cover an entire family under one roof.

-

Since it is a single policy, you have to pay a single premium that provides coverage to multiple members.

-

It provides reimbursement for all the medical expenses and hospital bills of the insured members.

-

If you go for treatment in a network hospital of the insurance company, you do not have to pay anything from your pocket, except the co-pay amount, depending on the terms and conditions of your health insurance. The insurance company directly settles the amount with the hospital.

-

If you would like to go to a hospital of your choice which is not a part of your insurer's network hospitals, you can claim the amount with the original hospital bills.

-

Normally, health insurance provides pre and post hospitalisation coverage, coverage for treatments done under AYUSH (Ayurveda, Yoga and Naturopathy, Unani, Siddha, and Homeopathy), ambulance coverage, etc.

-

Some critical illnesses are covered under basic family floater health insurance.

What is the difference between Individual and Family Floater Health Insurance?

Family floater health insurance has all the benefits that an individual health insurance plan offers. The key difference being that it extends the coverage to the entire family. To understand the family floater health insurance in a better way, let's see how it is different from individual health insurance:

-

Coverage:

Individual health insurance policy offers coverage to only one person. This means only that person can take advantage of the plan. For example, if you have purchased an individual health insurance policy with a sum insured of Rs 5 Lakhs, you can use it to cover only your own medical expenses. If your loved one or dependant falls sick within the policy period, you cannot use this policy to cover their expenses since it is in your name.

A family floater health insurance offers coverage to an entire family. Hence all the insured members in the family can take advantage of it. For example, if you have purchased a family floater health insurance policy with a sum insured of Rs 5 Lakhs and have added your spouse, child, and yourself as insured family members, all three of you can use the sum insured within the policy period.

-

Premium:

In the case of an individual health plan, you have to pay a separate premium for each family member that you want to secure under health insurance, which ultimately increases the premium cost of having health insurance.

With the family floater health insurance, you pay a single premium that takes care of your entire family's health insurance need. This makes the premium payment not only convenient but also cost-effective.

-

Sum Insured:

The sum insured in the individual health insurance policy is dedicated to a single policyholder. Whereas, in family floater health insurance, the sum insured is shared amongst all the insured family members, which could be the biggest disadvantage when maximum or all the family members fall sick during the policy period. But, many general insurance companies have started offering a feature that provides a separate sum insured for each member covered.

-

Suitable for:

An individual health insurance plan is suitable for single adults and senior citizens. Although you can cover your elderly parents under your family floater policy, the premium is significantly higher than individual plans.

A family floater health insurance plan is ideal for married couples or small families with 2 adults and 1 or 2 children.

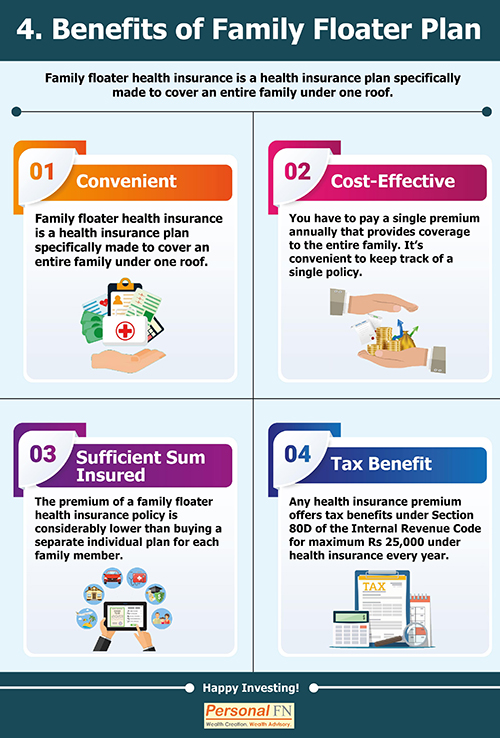

What are the benefits of Family Floater Health Insurance?

-

Convenient:

Since you have to pay a single premium annually that provides coverage to the entire family, you have to keep track of a single policy. You may consider purchasing a long-term health insurance policy for a period of 2-3 years that you do not have to renew every year.

-

Cost-Effective:

The premium of a family floater health insurance policy is considerably lower than buying a separate individual plan for each family member. Hence, it is a cost-effective way to cover all your family members under one roof.

-

Sufficient Sum Insured:

Family floater health insurance policy generally starts with a higher sum insured. The possibility of all the members falling sick in a single policy year is relatively lower, and people usually opt for a higher sum insured in a family floater. This makes the sum insured sufficient for all the insured members.

As discussed earlier, many insurers are coming up with a feature that provides a separate sum insured for each member. For example, you have a family floater plan with a sum insured of Rs 5 Lakhs that covers your spouse, child/children, and yourself. Say you have utilised Rs 4 lakhs of the sum insured in the third month of the policy, and in the seventh month, your spouse needs a cover of Rs. 5 Lakhs. As you had already utilised 4 Lakhs, your wife would be entitled to get the benefit of the remaining Rs 1 Lakh only . However, with the feature of a separate sum insured for each member, your spouse will also get the benefit of the policy, which otherwise would not be possible with a normal family floater health insurance policy.

-

Tax Benefit:

Any health insurance premium offers tax benefits under Section 80D of the Internal Revenue Code. You are eligible for a tax deduction of maximum Rs 25,000 under health insurance every year.

What are the things I need to consider before buying a family health insurance policy?

It is important to take precautionary measures while choosing the best-suited family floater health insurance policy. Consider these points while you make a purchase decision.

-

Plan Details:

Make sure the sum insured is adequate for all the family members that you want to cover. It is advisable to take individual plans for your parents and in-laws to save on the premium amount. While choosing a health insurance plan, compare the premiums online to get the best deal.

-

Inclusions and Exclusions:

Buying a policy from an established insurer does not necessarily mean it offers all the features you are looking for. Visit the official website of the insurer to check the list of inclusions that tells you what is included in the policy. You must also check the list of exclusions that explains what is not covered and/or exempted from the policy.

-

Claim Settlement Process:

Ideally, the claim settlement process should be easy and quick. Sometimes, if the claim settlement process is tedious and not clear, people discard the settlement process mid-way and end up paying from their own pockets.

-

Cashless Hospital Network:

Ensure that your insurer has the maximum hospitals in its network as it will help you with a cashless claim settlement. In times of uncertainty, arranging for cash can be challenging and therefore cashless claim settlement would be preferred by most people.

-

No Claim Bonus:

No Claim Bonus, also known as NCB, is a cumulative bonus that is added to your sum insured as a reward for every claim-free year. Generally, insurance companies offer 5% NCB every year, until you reach its maximum limit of 50%.

-

Co-pay:

Co-pay is a percentage of a health insurance claim amount that a policyholder needs to pay from his/her own pocket. For example, if you have filed a claim for Rs 2,00,000, and a co-pay mentioned in your policy document is 10%; in this case, you need to pay Rs 20,000 towards your hospital bill and the insurance company will pay the rest of the amount.

-

Added Benefits:

Do take into account the list of other benefits that the insurer offers, such as a cap on ICU rent and room rent, pre and post hospitalisation expenses, daily hospital cash allowance, COVID-19 coverage, online renewal, lifelong renewal, etc.

Conclusion:

Undoubtedly, in today's post-pandemic climate, health insurance is a must-have investment for every household. The festive season is the right time to gift your family a financially secured future. Ensure you understand the plan completely, know all the features, consider all the points mentioned above, and choose the right policy that protects you and your family.

Warm Regards,

Ketki Jadhav

Content Writer

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds