How an Extended Lockdown Has Amplified Credit Risk

Listen to How an Extended Lockdown Has Amplified Credit Risk

00:00

00:00

The turbulent wave of COVID-19 is seeping into the cracks of India's credit environment, which is striving to revive itself ever since the great defaulters were pulled out.

The default caused a ripple effect that led to rising NPAs and liquidity crunch. This further led to drop in demand and pushed the economy on a slow growth trajectory.

However, green shoots of economic revival were seen in the interim, thanks to several government measures, and consecutive repo rate cuts as well. But the pandemic Coronavirus has given the economy the worst flu of slowdown it has ever seen.

[Read: Coronavirus Has No Antidote. Your Bad Investments Could Have.]

To control the pandemic, a lockdown of 21 days from March 25, 2020 was put into effect. This has affected lot of sectors of the economy. And from April 14, 2020 onwards, another 21 days of lockdown has been introduced across the nation.

Already in lockdown 1.0, a host of companies from cement to heavy engineering, from automakers to ancillaries had announced temporary shutdowns. Eventually, FMCG companies cut down on their production capacities. Adding to it, the falling crude prices and Yes bank's bail out has left the economy crippled.

Image Source: Image by Mimzy from Pixabay

Image Source: Image by Mimzy from Pixabay

Current Credit Market overview

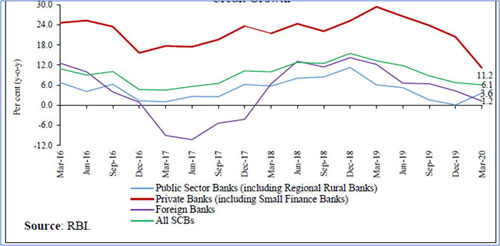

As per the monetary policy report released by the RBI, there was a seasonal decline in the credit growth in Q3 in 2019-20 that was more pronounced than a year ago. While the offtake during Q4:2019-20 (up to March 13) has been subdued as compared with the corresponding quarters of the previous two years.

The slowdown in credit growth was spread across all bank groups, especially private sector banks. Credit growth of public sector and foreign banks remained modest, even as there has been some uptick in credit by public sector banks in the recent period.

Graph 1: Bank Group Wise Credit Growth

(Source: RBI Monetary Policy Report - April 2020)

(Source: RBI Monetary Policy Report - April 2020)

Of the incremental credit extended by scheduled commercial banks (SCBs) during the year (March 15, 2019 to March 13, 2020), 62.6% was provided by private sector banks, 36.6% by public sector banks and 0.8% by foreign banks.

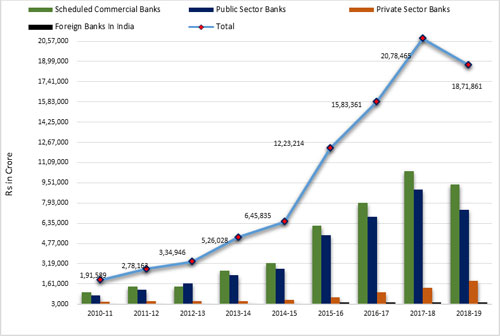

And the overall non-performing assets (NPA) ratio of SCBs remained unchanged in December 2019 from end-March 2019. The RBI's Financial Stability Report released in December 2019 expects bank GNPAs to rise to 9.9% by September 2020 from 9.3% in September 2019.

Likewise, bank frauds have reported a spike due to delayed recognition. Going by the RBI's Financial Stability Report released in December 2019, a total 4,412 cases of frauds amounting to Rs 1.13 trillion were reported in the first half of the fiscal year 2019-20, while the total frauds in the previous financial year were worth Rs 71,543 crore (with 6,801 cases).

Graph 2: Gross NPAs need to reduce

As per the data available up to Financial Year 2018-19.

As per the data available up to Financial Year 2018-19.

(Data source: RBI)

Overview of Credit Risk Funds...

Credit risk involved is directly proportional the quality of debt instruments held in an investment portfolio of a mutual fund. Credit risk refers to the risk of loss of principal and/or the interest on the debt instrument one holds.

Most commonly in credit risk funds, the credit risk is high. As per the categorisation norms, a credit risk fund will invest minimum 65% of its total assets in corporate bonds (below highest rated instruments), i.e. investment will be predominantly in AA and below rated instruments.

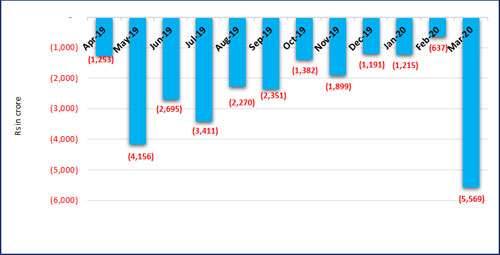

Banking frauds and the rising NPA does not reveal a very healthy and virtuous picture for the investors and, therefore, the credit risk is very much evident. A number of debt mutual fund schemes have taken a hit, particularly, Credit Risk Funds.

Most of these funds held toxic debt papers, and the recent pandemic has impacted credit risk funds, which are yet to see inflows, further.

Graph 3: Investors cashing out of Credit Risk Funds

Data as on March 31, 2020

Data as on March 31, 2020

(Source: AMFI; PersonalfN Research)

Outlook: Probable Amplified Credit Risk

The COVID-19 lockdown that is bound to hurt the economy for a couple of quarters is likely to amplify the credit risk. Lockdown 2.0 is going to hit the bottom lines of many companies.

[Read: 5 Valuable Money Management Lessons from the Coronavirus Pandemic]

Small and medium companies will require loans to sustain operations, which will lead to more borrowing activity and lower consumption demand is expected to drag economic growth further.

While India does not have official high frequency labour market data, the unemployment rate put together by the Centre for Monitoring Indian Economy, or CMIE, shows a spike in the last week of March and first week of April. The unemployment rate during the last week of March rose to 23.8 percent and stayed around those levels in the first week of April.

One can't imagine the plight of deferment and drop in income of people, which will affect the credit line as the number of defaulters will rise because cash strapping will be seen. Lockdown 2.0 is about survival, but it comes at the cost of the livelihoods of the people and India's economy growth with rising NPAs.

In addition, being aware that disruption caused by COVID-19 is likely to put a burden on debt servicing, the RBI directed a three months moratorium in respect to all term loans outstanding as on March 1, 2020.

[Read: RBI Finally Pulls Out Its Weapons to Combat the Coronavirus Pandemic]

However, in latest RBI announcement on April 17, 2020, as a stimulus relief measure the RBI decided to provide an asset classification standstill for standard accounts that avail a moratorium between 1 March and 31 May. This means that the bad loan classification period changes to 180 days for all such accounts from 90 days.

According to the RBI's latest announcement, the accounts turn non-performing assets (NPAs) after 90 days of overdue in making payments. The accounts are classified as standard before the 90-day period. In addition, the RBI also allowed the NBFCs to grant relaxed NPA classification to the borrowers.

Recognising the risk stemming from the bottom hit economy, wherein the growth projections by the IMF are almost 1.9% due to the CoVID-19. The NPAs of banks and NBFCs are expected to increase. "Considering that there has been no substantial improvement in the economy, ageing provisions and coupled with the recent outbreak of COVID-19, the banking sector might witness an adverse impact on credit delivery and asset quality, leading to pressure on capital adequacy," said CARE Ratings in a report. Further, the rating agency envisages prolonged disruption to impact the ability of companies - particularly the Micro, Small and Medium Enterprises (MSMEs) across various sectors - to service their loans resulting in higher NPAs. Gross Non-performing Assets (GNPAs) of Banks would increase to 9.6-9.9% from 9.3%.

What should investors do?

At this juncture, investing in debt mutual funds by blindly chasing higher credit risk is unwise. Avoid investing in Credit Risk Funds.

It is essential to evaluate the portfolio characteristics of debt mutual funds to assess the quality of debt papers and their maturity profile and weigh the potential risk-reward. Choose debt mutual funds where the fund house has a robust investment process and risk management strategy in place and where the fund manager does not chase returns by taking higher credit risk.

At PersonalFN, we select and recommend mutual funds on quantitative and qualitative parameters using our S.M.A.R.T Score Matrix:

-

S - Systems and Processes

-

M - Market Cycle Performance

-

A - Asset Management Style

-

R - Risk-Reward Ratios

-

T - Performance Track Record

If you wish to select worthy mutual fund schemes, I recommend you to subscribe to PersonalFN's unbiased premium research service, FundSelect.

Additionally, as a bonus, you get access to PersonalFN's popular debt mutual fund service, DebtSelect.

Warm Regards,

Aditi Murkute

Senior Writer

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds