How RBI's Recent Announcements Impact Your Debt Funds

Listen to How RBI's Recent Announcements Impact Your Debt Funds

00:00

00:00

Two months into the nationwide lockdown to curb the spread of virus, the economic conditions have deteriorated. The India Manufacturing Purchasing Managers' Index (PMI) fell to an all-time low of 27.4 in April from 51.8 in March due to the sudden halt in business operations. Similarly, PMI for services fell to a record low of 5.4 in April as compared to 49.3 in March.

[Read: Make Mindful Choices of Mutual Fund investments in Current times]

The Monetary Policy Committee (MPC) of RBI is of the view that the macroeconomic impact of the pandemic is turning out to be more severe than initially anticipated. It expects GDP growth in 2020-21 to remain in negative territory, with some pick-up in growth impulses from the second half of the year.

Taking cognizance of the acute risk to growth, the MPC felt it was necessary to facilitate the flow of funds at affordable rates and rekindle investment impulses. Accordingly, on May 22, MPC voted to reduce the policy repo rate by 40 basis points from 4.4 per cent to 4.0 per cent while maintaining the accommodative stance as long as necessary to revive growth, mitigate the impact of COVID-19, while ensuring that inflation remains within the target. Reverse repo has been reduced to 3.35 per cent from 3.75 per cent earlier.

Table: Series of policy rate cuts in 2019-20 to address growth concerns

| Month |

Repo Policy Rate |

Policy rate cut (Basis points) |

Monetary Policy Stance |

| Feb-19 |

6.25% |

25 |

Neutral |

| Apr-19 |

6.00% |

25 |

Neutral |

| Jun-19 |

5.75% |

25 |

Accommodative |

| Aug-19 |

5.40% |

35 |

Accommodative |

| Oct-19 |

5.15% |

25 |

Accommodative |

| Dec-19 |

5.15% |

Status quo |

Accommodative |

| Feb-20 |

5.15% |

Status quo |

Accommodative |

| Mar-20 (an exceptional off cycle meeting) |

4.40% |

75 |

Accommodative |

| May-20 (an exceptional 2nd off cycle meeting) |

4.00% |

40 |

Accommodative |

| Total |

|

250 |

|

Data as of May 22, 2020

(Source: RBI)

The MPC expects inflation to remain firm in the first half of 2020-21, but should ease in the second half. It stated that if the inflation trajectory evolves as expected, more space will open up to address the risks to growth.

In addition, as the extension of lockdown is likely to put further strain on debt servicing, RBI has decided to extend the moratorium on term loan installments and the ease of financing working capital requirement by an additional 3 months, i.e. from June 1, 2020 till August 31, 2020.

The extension of loan moratorium also means that exemption from being classified as 'defaulter', resolution timelines for stressed assets, and asset classification standstill will also be extended by a period of three months.

Notably, interest would continue to accrue on the outstanding portion of the term loans during the moratorium period.

[Read: RBI Finally Pulls Out Its Weapons to Combat the Coronavirus Pandemic]

Impact of rate cut on debt funds

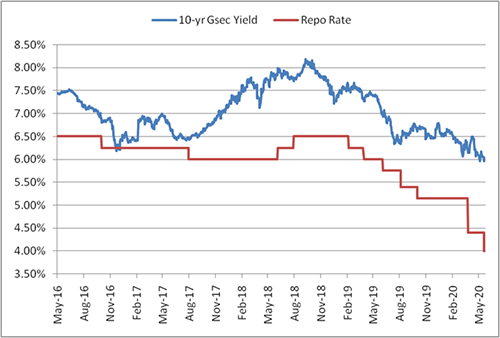

Debt funds generally gain from RBI's rate cuts. As interest rate and bond prices are inversely related, a rate cut pushes up NAVs of debt funds. This is especially true for long duration funds because they are more sensitive to movement in interest rates.

However, we may not see significant rally in longer duration funds.

The government has raised its FY21 borrowing limit by over 50% to Rs 12 lakh crore from Rs 7.8 lakh crore on account of COVID-19 pandemic. Higher borrowing puts upward pressure on bond yields.

Moreover, most of the rally at the longer end of the yield curve has already come about since the time RBI started reducing policy rates. So, the longer end of the yield curve could thus prove less rewarding and risky (may encounter high volatility) in the foreseeable future.

For shorter duration funds, the rate cut would have limited impacted on prices and the yields.

Graph: Impact of rate cut on G-Sec yield

Data as of May 26, 2020

Data as of May 26, 2020

(Source: RBI, PersonalFN Research)

Impact of extension of loan moratorium

While the extension of loan moratorium comes as relief to borrowers facing a liquidity crunch, it is a sign of worry for banks and NBFCs. A large chunk of outstanding loans of banks and NBFCs has come under the moratorium.

Though RBI has provided temporary relaxation in recognizing such accounts as non-performing assets, after the end of relaxation period, bad loans are expected to shoot up in the financial system.

Many debt funds have substantial exposure to papers in banking and finance sector.If the non-performing assets of these firms pile-up, it will have an impact on the mutual funds holding exposure to such firms.

How to approach debt funds

In the current volatile and uncertain market condition, short duration funds look attractive from the risk-return point of view. But approach even short-term debt funds with your eyes wide open and pay attention to the portfolio characteristics and quality of the scheme.

[Read: Lessons Learnt from the Debt Fund Crisis]

Do note that the extended COVID-19 lockdown is likely to amplify the credit risk (owing to a slowdown in business). Hence, stick to debt mutual funds where the fund manager does not chase yields by taking higher credit risk.

Preferably, invest in instruments issued by government and public sector enterprises, and stay away from those having high exposure to private issuers. Remember, investing in debt funds is not risk-free.

At present, it would be better to opt for a pure Liquid Fund and/or Overnight Fund which does not have high exposure to private issuers.

Assess your risk appetite and investment time horizon while investing in debt funds and prefer the safety of principal over returns.

Warm Regards,

Divya Grover

Research Analyst

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds