How to Build a Debt Portfolio in Rising Interest Rates

Mitali Dhoke

Jun 16, 2022

Listen to How to Build a Debt Portfolio in Rising Interest Rates

00:00

00:00

In the recent years, amidst the COVID-19 outbreak, RBI had reduced policy rates to encourage economic growth. However, as inflation in India is rising at an alarming rate, the central bank moved its priority from economic growth to inflation control.

In an off-cycle move, on May 04, 2022, the RBI announced a rise of 40 bps in the benchmark repo rate and a 50 bps hike in the Cash Reserve Ratio (or CRR). As the spiralling inflation continues to sting the economic growth, the Monetary Policy Committee (MPC), at its meeting held on June 08, 2022, decided to increase the policy repo rate under the liquidity adjustment facility (LAF) by 50 basis points to 4.90% with immediate effect.

Historically, Debt Funds are known as a safer investment option, particularly in times of market volatility. Rising interest rates, an uncertain macro environment, and higher yields, on the other hand, are likely to have influenced investors' debt market investing preferences. With the RBI's rate hike to combat inflation, investors in Debt mutual funds and other securities are concerned about their returns.

According to the data from the Association of Mutual Funds in India (AMFI), debt mutual funds focused on investing in fixed-income securities witnessed a net outflow of Rs 32,722 crore in May as the Reserve Bank of India (RBI) tightened monetary policy to control inflation caused by global factors. This comes after an inflow of Rs 54,656 crore in April 2022.

Mutual fund investors could tweak their fixed income portfolio as the Reserve Bank of India's increased focus on managing inflation has driven up short-term interest rates. Except for overnight and liquid funds, most Debt fund categories have seen outflows due to the current situation and broader market expectations. Single-digit returns and a strong preference for other asset classes, such as equity, are likely to have influenced debt fund flows.

For debt fund managers, certain previous financial years can be described as dreadful. The IL&FS Securities Services Ltd. crisis triggered a wildfire in the NBFC sector. In addition, Franklin Templeton credit risk debt funds fiasco also disturbed the debt fund investor sentiment. All of these events have contributed to the debt markets' instability.

Furthermore, the global economy is currently dealing with multi-decadal high inflation and slow economic growth, persistent geopolitical tensions and sanctions, rising crude oil and other commodity prices, and COVID-19-related supply chain limitations. In such a scenario, building a stable debt-oriented mutual fund portfolio is a key challenge for investors.

Image source: www.freepik.com

Image source: www.freepik.com

Join Now: PersonalFN is now on Telegram. Join FREE Today to get 'Daily Wealth Letter' and Exclusive Updates on Mutual Funds

Rising Bond Yields...

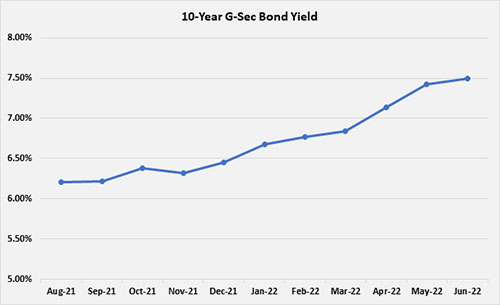

Debt Mutual Funds invest in fixed income securities like corporate or government bonds and money market instruments. The start of the rate hike cycle, inflationary pressure (particularly oil prices), falling Rupee, higher government borrowings, a worrying debt-to-GDP ratio, and the uncertainties due to the Russia-Ukraine war kept the yields elevated. Following the RBI's decision of a rate hike, Indian bond markets reacted swiftly, with the 10-year G-Sec benchmark yield crossing the 7.5% mark in June 2022.

Bond prices and interest rates are like the two halves of a seesaw: When one rises, the other falls. In the same way, when interest rates rise, bond prices fall, and vice versa.

The extent to which bond prices fluctuate in response to interest rate changes is determined by the bond's residual maturity (i.e., the number of years till it matures) or duration. The higher the duration, the greater the fluctuation in bond prices.

Graph: The 10-year benchmark yield fluctuations

Data as of June 16, 2022

Data as of June 16, 2022

(Source: Investing.com, PersonalFN Research)

The bond yields have increased up to 100 basis points over the last 10 months. Debt schemes that invest in short-term papers are best poised to benefit from the rise in bond yields. A rise in interest rates causes mark-to-market losses for long-term debt schemes like gilt funds, which bet on government paper, and income funds, as these products trade in bonds to produce returns.

Tweak Your Debt Portfolio...

With interest rates on the rise as a result of higher inflation, investors must adjust their existing debt fund portfolios and make new investments with an absolute time horizon in mind. When interest rates rise, the value of current debt fund investments decreases because investors choose to invest in higher-rate funds.

Conservative investors should adhere to short-term debt categories like liquid and money market funds, which tend to benefit from rising interest rates. Dynamic Bond Funds, which have the flexibility to adjust to changing macroeconomic conditions, are a good option for investors with a longer investment horizon and a higher risk tolerance.

How to build a stable Debt Mutual Fund Portfolio?

Since the longer end of the yield curve has higher volatility, investors should allocate more to the short end of the curve. If interest rates rise, and bond prices fall, the investors' return in the debt mutual fund scheme will suffer. Short-term maturity investments are becoming more appealing in this environment, and several fund houses are aligning their debt portfolios accordingly.

Investors may allocate their corpus into Debt Mutual Funds with a portfolio duration of 1 to 3 years, such as banking and PSU funds and corporate bond funds, where the impact of increased interest rates on overall returns is low. Some portion can be parked in liquid funds with a one-year maturity or ultra-short-term funds with a two-year maturity; the yields on these funds will begin to rise soon, and the impact of rising rates on underlying bond prices and overall return will be minimal. As the yields on banks and PSU debt or credit risk funds rise, liquid fund assets may be shifted to these categories.

Typically, you will invest in liquid funds to avoid negative impacts on your debt portfolio. However, liquid funds may offer higher returns than fixed deposits and savings accounts but generates lower returns as compared to liquid plus categories. If you can bear more risk and extend your investment horizon by two years, you will get substantially higher returns than liquid funds.

When you invest in debt funds holding debt securities of shorter duration the interest rate risk will be low because the investments will roll down, meaning the maturity will decrease over time. As a result, even if interest rates rise further, funds will not be impacted. The idea is basically to earn better risk-adjusted returns.

In a rising interest rate scenario, the reinvestment risk for debt funds is that the investor will only be able to profit once the entire rate hike cycle is completed. Investors should shift into medium-term or long-term duration funds once they believe the interest rate cycle has peaked, but until then, they should stay on the lower end of the curve.

There are other strategies that can help investors take advantage of the rising interest rate. These include increasing allocation to floating rate instruments or debt schemes focusing on such instruments with floating rates. Such debt funds invest at a point in the curve where the risk-reward ratio is favourable and then holds the investment until maturity. In a rising rate environment, the advantage of such a structure is that a portion of the corpus that matures each year is reinvested at a higher yield at the maturity point of the structure. Floating rate funds have the option of switching to newer issuances of higher-rate securities. Do note that debt funds with floating rates are high-risk-high return investment proposition.

Markets go through different cycles, and investors should stick to their asset allocation and diversification throughout each cycle to achieve the best outcomes. However, keep in mind that investing in debt funds entails certain risks, including credit risk, interest rate risk, liquidity risk, etc.

Ideally, considering the current market conditions, you will be better off to deploy your hard-earned money in short-term debt funds, but ensure you are giving due importance to your risk profile, investment horizon, and objectives.

As a result, to mitigate the effects of the RBI's Repo Rate hike, you should be prudent and wisely navigate your mutual funds in diversified asset classes, as per your suitability.

PS: If you wish to select actively managed worthy mutual fund schemes, I recommend that you subscribe to PersonalFN's unbiased premium research service, FundSelect.

As a bonus, you get access to PersonalFN's popular debt mutual fund service, DebtSelect.

PersonalFN recommendations go through our stringent process that assesses both quantitative and qualitative parameters, providing you with Buy, Hold, and Sell recommendations on equity and debt mutual fund schemes. Read here for more details...

If you are serious about investing in rewarding mutual fund schemes, Subscribe now!

Warm Regards,

Mitali Dhoke

Jr. Research Analyst