How to Improve the Resilience of Your Investment Portfolio

Listen to How to Improve the Resilience of Your Investment Portfolio

00:00

00:00

India is in the third phase of the extended lockdown due to the increasing number of COVID-19 test positive cases with no signs of containment yet. Despite the severe impact of the coronavirus pandemic, people are becoming more resilient.

Resilience and adaptability are two important traits that determine how we recover after we take a punch in the gut, a shock to your senses, and bounce back. Resilience is what we need to survive and lead a life when regular income is highly uncertain due to the current situation.

[Read: Coronavirus Has No Antidote. Your Bad Investments Could Have.]

Recently a friend said, "Aditi! By worrying about job cuts which are happening, no available vacancies and even salaries that are being held up, we can't change anything. We have to just focus on what we can do next to go on."

It really did strike a chord and I realized that the COVID-19 crisis is actually instrumental in making us more resilient. We have no other choice but to accept it and keep going on undeterred. We are doing our part with social distancing and staying home to prevent the spreading of the virus, but is that enough?

The imposed lockdown has changed our outlook on money management. Saving more for survival and preserving wealth is of prime importance now. It is beneficial to have a similar approach towards investments as well. Of course, it is extremely hard in the current circumstances; and my colleague rightly mentioned, "Cash Is King" in How Should a Novice Approach Mutual Funds amidst COVID-19.

Since the news of very first COVID-19 case was reported in Wuhan, China - the epicenter of the deadly Coronavirus on November 17, 2019, and in India, on January 30, 2020; the equity markets in India (and across the world) have been reacting extremely volatile -- almost a roller-coaster full of troughs and crests with more troughs seen though.

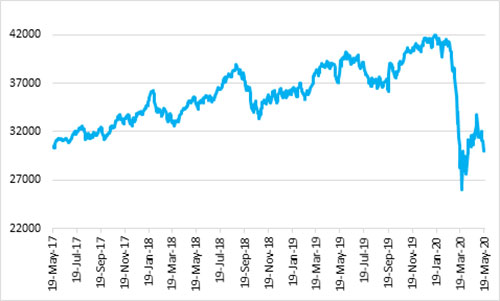

The S&P BSE Sensex has spiraled downward and investors are losing their capital (see graph 1)

Graph 1: S&P BSE Sensex fallen off the cliff

Data from November 8, 2019, to May 8, 2020

Data from November 8, 2019, to May 8, 2020

(Source: BSE; PersonalFN Research)

With the daily rise in the number of cases being reported, there is no end in sight. It's like heading into uncharted territory - what the future holds is unknown. Some experts state that the bear phase is bottoming out and is heading for a recovery, yet the Indian equity markets are expected to remain volatile going forward.

With more than 25% correction in barely a couple months, there have, of course, been bouts of impulses or upturns with many investors recognising value-buying opportunity - and rightly so.

But then, it would be imprudent to rule out the reversals or downturns, particularly when the COVID-19 pandemic is playing havoc and may be followed with a financial crisis (as the credit risk is amplified) and the risk of a global recession looms large.

But then, volatility is the very nature of the equity market; it is how we use it to our advantage, perceive the situation sensibly, and devise an efficient strategy that decides our investment success.

The credit risk has already begun to amplify; going forward, we cannot dismiss the chances of downgrades and defaults. Companies may approach the Courts to prevent default, but the capital market has abhorred this because it is not an industry best practice.

To provide some leeway to value debt securities in light of the hardships caused by COVID-19 lockdown (and/or as an afterthought to the moratorium permitted by RBI), the capital market regulator has eased valuation norms for debt securities. This allows rating agencies to go a bit easy on the definition of 'default', provided the delay in payment of interest/principal has solely arisen due to the COVID-19 lockdown.

Image Source: Image by dawnfu from Pixabay

Image Source: Image by dawnfu from Pixabay

That said, it does not make investing in debt mutual funds very safe - particularly if the debt papers held are those of private issuers. This is because the chance of downgrade cannot be ruled out even for top-rated issuers and there have been many instances in the past where even AAA and equivalent rated papers have been downgraded by rating agencies during challenging times.

Agreed that, in such times there has been 'capital erosion' and focus is capital protection. But 'capital protection' does not strictly mean warding off negative returns. Losses are inevitable when the equity market hits turbulence and descends. Hence, what 'capital protection' actually means is cutting down on a disproportionate loss, wherein the damage is measured and appropriately contained.

So what should an investor do?

The wealth creation journey indubitably is going to be a non-linear process in 2020. Having said that, it is important to be mindful that a further correction cannot be ruled out and the bottom is unknown.

Do not give in to the trials of short-term volatility and look beyond the fear of the bears running loose. Keep investing; do not apply brakes on the journey of wealth creation.

In the current situation, there exist a good value-buying opportunity with a decent margin of safety. Just ensure that investments are congruent with your risk profile, investment objectives, financial goals, and time in hand to achieve the envisioned goals.

In such times, you, as an investor, must stay away from any external noise of pessimism and free advice from friends/ family/ neighbors because investing is an individualistic exercise.

Remain focused on the end goal of wealth accumulation and accomplishing financial goals, and need to review your risk profile (gauge how much risk you willing to assume) and take necessary measures to preserve your capital.

While different assets have different moods based on the market fluctuations, a proper allocation across asset class and investment style may protect you from the significant ups and downs of any single asset class and scheme in your portfolio.

Every asset class has a risk-return trait suitable for a certain level of personal risk appetite, investment objectives, financial goals, and the time horizon to achieve them.

Graph 2: Risk-return trade-off of various asset classes

For illustrative purpose only

For illustrative purpose only

(Source: PersonalFN Research)

An intelligently crafted asset allocation with the help of a SEBI-registered investment advisor or an investment counsellor will serve as an investment strategy in itself. This way you could balance the risk-reward to create a robust diversified portfolio that suits you best for your long-term financial and physical wellbeing.

A diversified portfolio helps to provide optimum returns and mitigates the risk of any single asset class has. Amidst the COVID-19 pandemic, the fixed income instruments would shield your portfolio, address short-term liquidity needs, and serve effective to build an emergency fund as they provide secure and steady returns.

Likewise, consider allocating some portion of the total investment portfolio to gold. The precious yellow metal commands a store of value, i.e. it is looked up to as a lender of last resort during economic uncertainties and displayed its trait of being an effective portfolio diversifier, a hedge over the years. On a year-to-date basis, gold has gained +5.0% and about +30.0% in the last one year.

[Read: Why Tactically Invest Across Asset Classes amidst COVID-19 with Quantum Multi-Asset Fund Of Funds]

Besides, do a comprehensive portfolio review to weed out the duds and replace them with something that can help you accomplish financial goals. Since the overall performance of your investment portfolio hinges on the investment schemes/options you hold.

For equities, check the inconsistence performance for over 3-year and the 5-year time period and the fallen interest rates on many fixed-income instruments due to the debt crisis.

Approach to investment

The pandemic has taught us what is essential and need to lead a moderate life and for that how much money we will actually require it is equally important to evaluate if the fundamentals of your investments have changed.

In the current scenario, it would be wise to diversify across market capitalisation via a multi-cap fund, while holding some proportion of your equity allocation in a large-cap fund, mid-cap fund, as well as a value style fund. Ensure you have a high-risk appetite, investment time of at least 7-8 years, and selecting the best schemes.

Staggered lump sum investments and Systematic Investment Plans (SIPs) is the strategy to follow in the journey of wealth creation. And in volatile times, do not stop or pause your SIPs. Discontinuing your SIPs will be unbeneficial to your portfolio and obstruct wealth creation.

[Read: How Quantum Multi Asset Fund of Funds Protects the Downside Risk]

Here's food for thought by the legendary investor Mr. Warren Buffett, "Be fearful when others are greedy and greedy when others are fearful".

Happy Investing!

Warm Regards,

Aditi Murkute

Senior Writer

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds