How to Protect Against the Downside Risk as the COVID-19 Booster Package Has Failed To Excite the Markets

Listen to How to Protect Against the Downside Risk as the COVID-19 Booster Package Has Failed To Excite the Markets

00:00

00:00

On the eve of May 12, 2020, the Prime Minister of India, Narendra Modi, announced a massive stimulus package worth Rs 20 lakh crore (purportedly almost 10% of India's GDP, but in reality around 1% of GDP) to counter the Coronavirus or COVID-19 crisis and said it will cover farmers, labourers, the middle class, the honest tax-payers, MSME, the cottage industry, and many other sectors.

Besides, he made a clarion call for 'Atmanirbhar Bharat' or self-reliant India, citing five pillars, as under:

-

An economy - which doesn't bring incremental changes but make a quantum jump

-

Infrastructure - that becomes the identity of modern India

-

Systems - that no longer based on the rules and rituals of the past, but one that actualises the dreams of the 21st century with technology

-

A vibrant democracy - which is a source of energy for self-reliant India

-

Demand - wherein the strength of demand plus the supply chain should be utilised to full capacity

It all sounded really exciting!

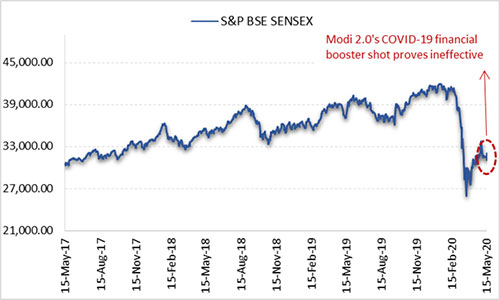

From May 13 to May 17, around 4:00 pm, post the trading hours of the Indian equity markets, the finance minister, Ms Nirmala Sitharaman and her subordinate, Mr Anurag Thakur (Minister of State for Finance and Corporate Affairs), in tranches unveiled the details.

But except May 13, 2020, where the S&P BSE Sensex jumped +2% (or +637.49 points) -- rallied on hopes -- on the ensuing dates the Indian equity markets did not end in green. In fact, became restless and lost hopes.

Graph: Booster shot failed to boost market spirits

Data as of May 15, 2020

Data as of May 15, 2020

Source: bseindia.com; PersonalFN Research

Some announcements, among many others, have far-reaching effects such as:

-

✓ Boost to the agriculture sector by spending Rs 1 lakh crore on building farm-gate infrastructure for farmers

-

✓ Use of technology to increase the shelf-life of various perishable agricultural commodities

-

✓ Enhanced credit assistance to farmers

-

✓ Foodgrains to migrant workers

-

✓ Hike the MGNREGA budget by an additional Rs 40,000 crore (from Rs 61,500 crore allocated in the Union Budget 2020-21)

-

✓ Ending the monopoly of APMC markets in India

-

✓ Ending the monopoly of government in the coal sector and introducing mining sector reforms;

-

✓ Opening Foreign Direct Investments (FDI) in the defence sector

-

✓ Liquidity infusion to NBFCs (worth Rs 45,000 crore)

-

✓ Loans to MSMEs (with Government of India guarantee) and launch of a Fund of Fund (FoF) to make equity infusion

-

✓ Interest subvention scheme for first-time homebuyers

-

✓ Relief in filing tax-returns and reduction in Tax Deduction at Source (TDS) and Tax Collection at Source (TCS) rates

-

✓ Labour reforms with provision for universal floor wages

...and more

However, to me most of the announcements seem long-term structural measures with the boastful drumroll of self-praise, rather than 'booster shots', which are supposed to address the immediate problem; provide a boost to the Indian economy, which is in an Intensive Care Unit (ICU) panting for breath as it fights the COVID-19 crisis.

The long-term structural reforms are, of course, needed to pave the path for 'Atmanirbhar Bharat' or self-reliant India, but this cannot be at the cost of an ailing Indian economy which is currently fighting the downside effects of the lockdown.

Why didn't the government bring up many of these reforms three-and-half months ago in the Union Budget 2021 announcements? If they had, perhaps that would have exuded more confidence in the economy and helped counter the present crisis better. The Budget 2021 failed to excite the Indian equity markets enough and so has the Modi 2.0 COVID-19 financial booster package.

It is unclear how the booster package will translate into higher demand, address supply-chain issues, and help businesses plus households deal with financial losses incurred on account of the COVID-19 pandemic and extended lockdowns alongside travel bans imposed to contain the spread of the deadly virus. The government should have placed money in pockets/accounts of those who need it the most.

While the credit line is opened with loans to different sectors and sections of the society, there is risk-aversion that has set in due to the money tap running thin (or dry) amidst the extended lockdowns. There may not be many takers for these loans, and even if there are, there is a high risk of those loans turning bad.

Ironically, banks have parked approximately Rs 8 lakh crore in reverse repos, which indicates that they are shying away from lending the money to businesses. However, the finance minister claimed in a press conference that many borrowers have asked banks to keep the disbursals on hold until clarity prevails on to when the lockdowns will end.

Former Finance Minister, Mr P Chidambaram mocked the announcement of this stimulus package calling it "a headline and a blank page", and also expressed that he will count every additional rupee that the government infuses into the economy.

How is the Indian equity market likely to respond going forward?

The S&P BSE Sensex is already down nearly -25% on a year-to-date basis. The bears are running loose as there is no end in sight from the Coronavirus pandemic.

The World Health Organisation (WHO) has warned that the virus is likely to be around for a long time, and everything appears extremely uncertain until the production of an effective vaccine. Currently, efforts are in the direction to develop an effective COVID-19 vaccine, but it may take around 12 to 18 months before it is available with medical store and practitioners.

For now, social distancing and lockdown seem the only way to contain the spread. And as a result, the economic impact of the coronavirus pandemic might last for a long time.

The International Monetary Fund (IMF) has warned that we could be looking at the worst global recession - worse than the Global Financial Crisis of 2008 and the Great Depression of the 1930s.

On the backdrop of the above, heightened volatility of the Indian equity market is here to stay -- investors may be on a crazy rollercoaster. But then volatility is the very nature of the equity market; it is how we use it to our advantage, perceive the situation sensibly, and devise an efficient strategy that decides our investment success.

If you have already been investing in equities and have a portfolio of equity-oriented funds, I suggest the first review the investment portfolio comprehensively seeking the help of a proficient SEBI-registered investment advisor. This will help you, the investor, in the following ways...

-

✓ Ensure that your investments and the asset allocation are in line with the financial objectives/goals, the risk appetite, and the time in hand to achieve the envisioned financial goals

-

✓ Facilitate portfolio rebalancing and consolidation

-

✓ Weed out the underperformers and replace them with better and more suitable ones

-

✓ Minimise portfolio risk and ensure the liquidity of the portfolio

-

✓ Facilitate portfolio optimal structuring and portfolio diversification

-

✓ Make sure you are on track to accomplish the envisioned financial goals

Currently, valuation-wise Indian equities look attractive, there is a decent margin of safety available, and the potential to earn respectable returns in high. This offers a good investment opportunity provided you are willing to take a higher calculated risk and have an investment time horizon of at least 7-8 years. Having said that, structuring the portfolio strategically and scheme selection is the key.

(Image source: freepik.com; photo courtesy mindandi)

(Image source: freepik.com; photo courtesy mindandi)

Follow the 'Core and Satellite' approach to investing

Under the current market scenario, prefer the 'Core & Satellite' approach to invest in equity-oriented mutual funds. This is a time-tested investment strategy followed by some of the most successful equity investors.

The 'Core' holdings should form a major portion (around 65-70%) of the mutual fund portfolio and ideally should consist of a Large-cap Fund, Multi-cap fund, and a Value Fund.

The rest, say around 35-40%, can be 'Satellite' holdings consisting of a Mid-cap Fund, Large & Mid-cap Fund and an Aggressive Hybrid Fund. If you are willing to take the risk, a small portion could be allocated to Small-cap Fund as well in the satellite holding.

The higher allocation to 'Core', stable funds with a long-term view is expected to add the stability factor to the portfolio, while the 'Satellite' funds generate alpha by seeking high-growth opportunities in the prevailing market conditions.

That being said, here are certain rules to create a strategic portfolio:

-

The selected funds should be amongst the top scorers in their respective categories. The portfolio should be built with a time horizon of at least five years

-

It should be diversified across investment style and fund management

-

Each fund should be true to its investment style and mandate

-

They should be managed by experienced and competent fund managers and belong to fund houses that have well-defined investment systems and processes in place

-

Each fund should have seen outperformance over at least three market cycles

-

The portfolio should contain an adequate number of schemes in the right proportion. In short, it should carry the most optimum allocation to each scheme and investment style

-

The number of schemes in your portfolio must be limited to seven

-

Not more than five schemes should be managed by the same fund manager

-

Not more than two schemes from the same fund house should be included in the portfolio

When all the aforesaid rules are followed judiciously, you will be able to draw the six key benefits of Core & Satellite approach:

-

Optimal diversification;

-

Reduce the need for constant churning of the entire portfolio;

-

Reduce the risk to the portfolio;

-

Gain from a variety of investment strategies;

-

Aims to create wealth cushioning the downside; and

-

Hold the potential to outperform the broader market

But what matters the most is the art of astutely structuring the portfolio by assigning weights to each category of mutual funds and the schemes selected for this strategic portfolio.

Moreover, with a change in market outlook, the allocation/weight to each of the schemes, especially in the satellite portfolio needs to change.

'Core and Satellite' strategy of investing will help you tide the COVID-19 crisis better without having to miss the investment opportunity that comes your way.

If you wish to invest in a readymade portfolio of top recommended equity mutual funds based on the 'Core & Satellite' approach to investing, I recommend that you subscribe to PersonalFN's Premium Report, "The Strategic Funds Portfolio For 2025 (2020 Edition)".

This premium report will help you build your optimum mutual funds portfolio for 2025 without any effort on your part. If you haven't subscribed yet, do it now!

Given that the Indian equity market is likely to be very volatile in the near future, taking the SIP route -- particularly if you are addressing long-term financial goals -- would be a wise thing to do. SIPs will help you to deal with the market volatility (with the inherent rupee-cost averaging feature of SIPs), instil the good habit of regular & systematic investing, and will be lighter on the wallet, while you endeavour to compound your hard-earned money.

You may invest a lump sum in a staggered manner, but avoid deploying the entire investible surplus at one go.

Apart from the above, buy and hold gold. As long as global uncertainty prevails, gold is expected to exhibit its sheen and prove its trait of being an effective portfolio diversifier, a safe haven, a hedge (when other asset classes fail to post appealing returns), and does command a store of value. Allocate around 10-15% of your entire investment portfolio to gold and hold it with a long-term investment horizon.

Finally, given that we are surrounded by uncertainty due to the COVID-19 crisis, hold 'optimal' cash level to pay your necessary monthly expenses and for your emergency needs. For the latter, park 12 to 24 months of regular monthly expenses, including EMIs on loans, in separate savings bank account and/or a pure Liquid Fund or an Overnight Fund, and never touch unless for an emergency.

Our friends at Quantum Mutual Fund have highlighted the secret behind their debt management strategy, which has helped them provide safety and liquidity to investors when it comes to investing in Quantum funds. Don't Worry, Quantum Liquid Fund always aims for Safety and Liquidity.

Happy Investing!

Warm Regards,

Rounaq Neroy

Editor, Daily Wealth Letter

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds