HSBC Corporate Bond Fund: A Fund for Strong Stomach

Listen to HSBC Corporate Bond Fund: A Fund for Strong Stomach

00:00

00:00

The recent Liquidity Surplus and RBI's Accommodative stance has reduced the returns that was favourable earlier at the short end of the yield curve for investment within debt mutual funds category.

Besides certain recent norms introduced by the capital market regulator is making investment in debt mutual funds more transparent for investors interest for better returns. And the government also asked fund houses to increase their portfolio allocation of some categories of debt mutual funds to government securities.

Looking at the aforementioned, HSBC Mutual Fund sought this opportunity to launch HSBC Corporate Bond Fund (HCBF), which will invest mainly in AA+ and above rated corporate bonds. Fund house is of the view that the current environment is presenting a pool of "High credit quality papers" and is favourable for 3 to 5-year duration range of maturity on the yield curve.

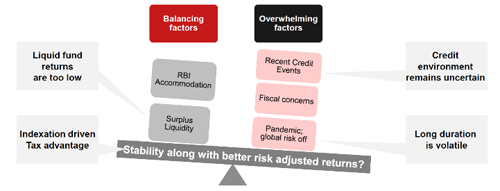

Image 1: Factors favouring corporate bond

(Source: HSBC Corporate Bond Fund NFO Note)

(Source: HSBC Corporate Bond Fund NFO Note)

Hence as per asset allocation mandated, HCBF will invest accordingly to capture optimum returns for investors having an investment time horizon of 3 to 4 years.

Table 1: Details of HSBC Corporate Bond Fund

| Type |

An open-ended debt scheme predominantly investing in AA+ and above rated corporate bonds |

Category |

Debt Scheme - Corporate Bond Fund |

| Investment Objective |

To seek to generate reasonable income and provide risk-adjusted returns by investing primarily in AA+ and above rated corporate debt securities. However, there can be no assurance or guarantee that the investment objective of the scheme would be achieved. |

| Min. Investment |

Rs 5,000 and in multiples of Re 1 thereafter |

Face Value |

Rs 10 per unit |

| Plans |

*default |

Options |

- Growth*

- Dividend

- Pay-out facility

- Reinvestment facility*

*Default option |

| Entry Load |

Nil |

Exit Load |

Nil |

| Fund Manager |

Mr Ritesh Jain |

Benchmark Index |

NIFTY Corporate Bond Index |

| Issue Opens: |

September 14, 2020 |

Issue Closes: |

September 28, 2020 |

(Source: Scheme Information Document)

How will the scheme allocate its assets?

Under normal circumstances, it is anticipated that the asset allocation of HBCF will be as follows:

Table 2: HBCF 's Asset Allocation

| Instruments |

Indicative Allocation (% of Total Assets) |

Risk Profile |

| Corporate Bonds rated AA+ and above |

80% to 100% |

Low to Medium |

| Corporate Bonds rated AA and below, including securitized debt* |

0% to 20% |

Medium to High |

| Money market instruments including cash and cash equivalents and debt instruments issued by central and state governments |

0% to 20% |

Low |

| Units of REITs and InVITs |

0% to 10% |

Medium to High |

* If the Scheme decides to invest in securitised debt, it is the intention of the Investment Manager that such investments will not normally exceed 20% of the corpus of the Scheme. No investments shall be made in foreign securitized debt.

(Source: Scheme Information Document)

What is the Investment Strategy of HCBF?

The Scheme would invest predominantly in corporate debt securities across maturities which are rated AA+ and above for the purpose of achieving the investment objective. The Scheme will largely be exposed to shorter to medium term fixed income yield curve, with focus to increase its accrual via selective and opportunistic exposure to corporate bonds and money market instruments. The security selection would be driven by investment team's view on credit spreads, liquidity and the risk reward assessment of each security.

The Scheme would largely maintain high credit quality portfolio. The investment team will carry out in depth credit evaluation of the debt instrument to be invested in. The credit evaluation will include financial position of the issuer, external credit ratings opinions, operational metrics, past track record as well as the future prospects of the issuer.

Strategies for fixed income derivatives

-

Bond - Swap: Under this strategy, the fund manager pays fixed rate on Overnight Indexed Swap (OIS) against an underlying bond of a similar or greater tenor and receives Mumbai Inter- Bank Offer Rate (MIBOR).

This is essentially done for hedging interest rate risk or for rebalancing portfolio allocation to fixed and floating rate bonds. Effectively, through this trade the fund manager is able to convert a fixed rate bond into a floating rate MIBOR linked instrument. The trade has exposure to 'basis movement' - the relative movement of bond versus OIS.

-

Receive OIS: Here the fund manager receives fixed rate on OIS against either cash or a floating rate bond of a similar or greater tenor, and pays MIBOR. The objective is to rebalance portfolio

in favour of fixed rate exposure.

-

Curve Steepener: This strategy aims to capture a potential steepening of the curve between any 2 tenors: say, 1 and 5 years. However, apart from the relative spread between the 5 year and 1 year OIS, the trade is also exposed to relative duration for the 2 tenors as well as basis

risk on the bond-swap.

-

Curve Flattener: This strategy aims to capture a potential flattening of the curve between any 2 tenors. Like mentioned above, the trade is also exposed to duration as well as basis risk.

Who will manage the HSBC Corporate Bond Fund?

Mr Ritesh Jain is the dedicated Fund Manager for HSBC Corporate Bond Fund. He is the Senior Vice President & Head of Fixed Income at the HSBC Asset Management Company.

He has a post-graduate diploma in business administration with a specialisation in finance and has a work experience of over 21 years.

Before joining HSBC Asset Management (India) Private Limited in June 2019, he worked at IIFL Asset Management Ltd as Partner & Head of Fixed Income, DHFL Pramerica Asset Managers Pvt Ltd as Executive Director & Head of Fixed Income, and Morgan Stanley Investment Management as Executive Director & Head of Fixed Income.

The outlook for HSBC Corporate Bond Fund

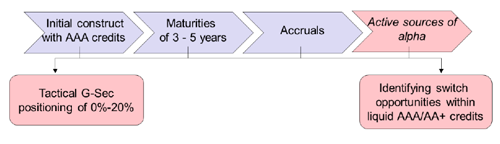

The HSBC Corporate Bond Fund will be actively managed to achieve the stated objective of the scheme. As per the intended asset allocation, the scheme will largely be exposed to a shorter to medium-term fixed income yield curve.

Image 2: Flowchart of asset allocation process

(Source: HSBC Corporate Bond Fund NFO Note)

(Source: HSBC Corporate Bond Fund NFO Note)

To construct the portfolio, the fund manager and his team will use the following investment strategy to deliver optimum returns for the investors.

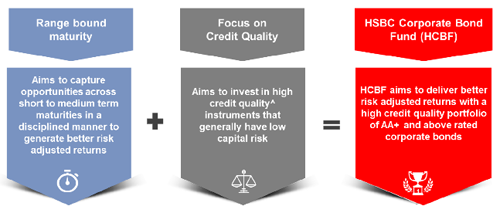

Image 3: Proposed investment strategy

(Source: HSBC Corporate Bond Fund NFO Note).

(Source: HSBC Corporate Bond Fund NFO Note).

Remember the debt instruments in the market can be broadly categorised as those issued by corporates, banks, financial institutions, and those issued by state / central governments. The risks associated with bond market investment are subject to credit risk, interest rate risk, and liquidity risk.

COVID-19 has likely put a burden on debt servicing, especially private issuers. The extended lock down has disrupted their business line proceedings and revenues resulting in an increased pressure, and chances of default.

The RBI announced loan moratoriums and further decided not to classify them as NPA. Moreover, providing a window for loan recasting in order to boost the economy by infusing liquidity.

On the backdrop of the uncertainty surrounding the inflation outlook and taking into consideration the extremely weak state of the economy amid an unprecedented shock from the ongoing pandemic, the Monetary Policy Committee of the RBI chose to pause the rate cuts and remain watchful of incoming inflation data.

This stance has actually pushed private entities for more credit borrowing, although their balance sheets may not look healthy to service debt obligations. Investment in corporate bond funds may look attractive, but probably comes with an elevated credit risk.

Hence the fortune of the HSBC Corporate Bond Fund relies on how the fund manager assess the aspects during portfolio construction and the kind of credit risk they are willing to expose investors to at this point. Thus, the fortune of HCBF will be hinged on the credit quality of securities held in its portfolio. One should consider their risk appetite while investing in Corporate Bond Funds.

Editor's note: The last few years have not been among the best for equity mutual funds. While most funds have underperformed or are struggling to match the returns of the benchmark, there are few funds that have the potential to constantly generate alpha for its investors. And we have identified five such high alpha generating funds, in our latest report 'The Alpha Funds Report 2020'. Do not miss our latest research finding. Get your access to this exclusive report, right here!

Warm Regards,

Aditi Murkute

Senior Writer

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds