Is It Worthwhile Investing in Debt Mutual Funds As the Indian Economy Sags?

Listen to Is It Worthwhile Investing in Debt Mutual Funds As the Indian Economy Sags?

00:00

00:00

IL&FS crisis that unfolded in September 2018 exposed the flaws of India's shallow credit markets. Two years hence, the COVID-19 pandemic has just exacerbated the credit risk. Corporates (across sectors) with strong financial muscle and balance sheet strength may manage to sail through rough waters, but the ones lacking adequate financial muscle and with highly leveraged balance sheets may find it difficult.

The RBI's Financial Stability Report 2020 (released in July) cautioned that Gross Non-Performing Assets (GNPAs) of Banks may increase from 8.5% in March 2020 to 12.5% by March 2021 under the baseline scenario. And if the macroeconomic environment worsens further, the ratio may escalate to 14.7% (a 22-year high) under very severe stress. The stress test showed that under an extreme stress scenario, banks could fail to fulfil the minimum capital adequacy requirement by March 2021. This is scary considering that large borrowers attribute 78% of GNPAs.

The central bank has observed that the unprecedented COVID-19 pandemic and its pan-global impact is taking a toll on lives and livelihood. This pandemic has the potential to amplify financial vulnerabilities, including corporate and household debt burdens, in the case of severe economic contraction.

Graph 1: India's GDP growth has shrunk to the worst in four decades

Data as of June 2020 quarter for GDP at constant prices of 2011-12

(Source: www.tradingeconomics.com)

India's GDP has already contracted sharply by -23.9% in Q1FY21. This reading is likely to weigh on the GDP growth for the full fiscal year 2020-21.

While unlocking from COVID-19 may abet economic growth, COVID-19 cases continue to rise. According to Dr Randeep Guleria, the AIIMs Director and the key member of the central government's special task force on COVID-19, few parts of India are already witnessing the second wave of COVID-positive cases. He also opined that the pandemic may continue in 2021 as well since the universal dosage of vaccine would take time.

As per the most optimistic GDP estimates for FY21, the Indian economy may witness around -10% contraction; whereas the most pessimistic estimate hints at -14.8% fall during the current fiscal.

Moody's, an international rating agency, has already slashed India's sovereign rating to 'Baa3' (with a negative outlook) -the lowest investment grade, just a notch above junk. The view of the independent rating agency is majorly influenced by the sustained slowdown in the economy and probable inability of policymaking institutions for implementing policies to revive growth. Besides, the government's fragile financial position and financial sector stress have been the other major reasons for the downgrade.

Due to front-loading of expenditure to combat COVID-19 pandemic, India's fiscal deficit in the first four months through July 2020 has overshot the annual budgeted estimate (of Rs 7.96 trillion) of the current fiscal year. This is 103% of the budgeted target; while last year fiscal deficit for the same period stood at 79% of the budgeted target. Given the odds, this year the government has also increased the market borrowing to Rs 12.0 trillion from Rs 7.8 trillion. According to CARE Ratings, the full-year fiscal deficit may balloon to 8% in 2020-21.

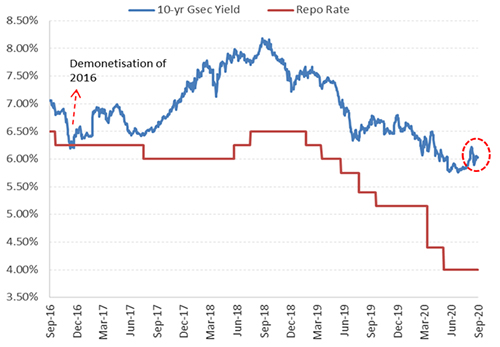

Graph 2: The 10-year G-sec yield has hardened

Data as of September 15, 2020

(Source: Investing.com, PersonalFN Research)

On the backdrop of the above, the 5.79% 10-year g-sec yield has hardened. Currently, the difference between the 10-year G-Sec yield and repo rate is around 200 bps compared to the long-term average of 80 bps.

Many investors are wondering whether or not to invest in debt funds, and rightly so.

Some proponents of debt funds have been expressing an optimistic view about Indian debt markets and pinning their hopes to the recent regulatory changes, apart from unrealistic hopes of recovery. They typically draw attention to five things that changed for the debt funds in the aftermath of IL& FS fiasco.

-

The market regulator allowed mutual funds to create side-pockets, which to an extent curbed distress selling.

-

The new mandate on liquid funds to invest 20% of their portfolio in cash & equivalent assets, has offered them a lot more stability.

-

Valuation guidelines on downgraded debt instruments brought uniformity

-

Sectoral caps enhanced the safety profile

-

And now that the frequency of portfolio disclosure has been changed from once a month to once a fortnight, the transparency has improved.

Well-intended regulatory changes might be adequate to safeguard investors against fallouts happening on account of occasional misinterpretation of the situation by the fund manager. But are they enough to shield investors from the systemic risk and the risks arising from bad investment decisions?

The answer is no!

(Image source: freepik.com; photo courtesy pressfoto)

In the current scenario, the risk has certainly intensified. The longer end of the yield curve would be more sensitive and expose you to higher risk. The RBI, between March and May 2020, slashed policy rates by 115 basis point (bps) thereby taking the quantum of total rate cuts to 250bps since February 2019. In the last monetary policy owing to an uncertain inflation outlook, the RBI maintained a status quo on policy rates, but the stance of policy was kept "accommodative stance as long as it is necessary to revive growth and mitigate the impact of COVID-19 on the economy".

Retail inflation for August 2020 has stayed flat at 6.69% as compared to 6.73% in July; but on a cumulative basis, it has remained above 6% (the upper limit of RBI's comfort range) between April and August. This might clip RBI's ability to slash policy rates further, especially when the credit offtake is very low and there's ample liquidity in the system.

What should investors do?

In the current scenario where interest rates seem almost bottomed out, you would do better going with very low or short-duration funds, where safety over the returns should be the focal point.

A pure Liquid Fund and/or an Overnight Fund that do not have high exposure to private issuers may be considered. But here too, you need to be extremely selective. Do not invest in funds that compromise on portfolio quality for returns, pay low attention to risk management and the ones not following sound investment systems and processes.

Many debt mutual funds irrespective of their maturity profiles are dealing with downgrades of papers held in their portfolio. Franklin Templeton discontinuing six of its schemes abruptly has highlighted how hazardous it would be for your portfolio to invest in debt funds merely relying on brand value. Do not assume debt mutual funds schemes to be risk-free. To select a scheme it's imperative to evaluate your risk appetite and investment time horizon, and also other factors such as:

The portfolio characteristics of the debt schemes

-

The average maturity profile

-

The corpus & expense ratio of the scheme

-

The rolling returns

-

The risk ratios

-

The interest rate cycle

-

The investment processes & systems at the fund house

Our friends at Quantum Mutual Fund have highlighted the secret behind their debt management strategy, which has helped them provide safety and liquidity to investors when it comes to investing in Quantum funds. Don't Worry, Quantum Liquid Fund always aims for Safety and Liquidity.

Looking at the widespread contagion of credit risk and mismanagement of fund houses, I believe the aforesaid sub-categories of debt funds (i.e. a Liquid Fund and/or Overnight Fund) would be befitting for the safety of principal over return. And if the investment time horizon is over a year, you may consider Banking & PSU Debt Funds that allocates 85-90% of its assets in instruments issued by major Banks and PSUs.

It is time to distance yourself from other debt funds --particularly those holding a predominant portion in debt papers issued by private issuers and low-rated instruments in the hunt for higher yield.

Alternatively, if you prefer to keep your capital safe, opt for bank fixed deposits, but there as well, choose the bank carefully.

Happy Investing!

Warm Regards,

Rounaq Neroy

Editor, Daily Wealth Letter

PS: If you wish to select worthy mutual fund schemes, I recommend subscribing to PersonalFN's unbiased premium research service, FundSelect.

Additionally, as a bonus, you get access to PersonalFN's popular debt mutual fund service, DebtSelect.

Each fund recommended under FundSelect goes through our stringent process, where they are tested on both quantitative as well as qualitative parameters.

Every month, PersonalFN'sFundSelect service will provide you with insightful and practical guidance on equity mutual funds and debt schemes - the ones to Buy, Hold, or Sell.

If you are serious about investing in a rewarding mutual fund scheme, Subscribe now!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds