3 Best Liquid Mutual Funds to Invest in 2022

PersonalFN Content & Research Team

Apr 13, 2022

Listen to 3 Best Liquid Mutual Funds to Invest in 2022

00:00

00:00

Introduction to Best Liquid Mutual Funds for 2022

Liquid mutual funds are often the most ignored and an after-thought for the majority of investors. This rings especially true for the millennials and the generation Z, who invest in the stock market with an aim to make quick money. In their race to find the next 'big thing', they seldom bother to create a contingency fund. After all, living in the moment is all that matters. Therefore, these new-age investors refrain from investing in liquid funds as the 5-6% returns generated by liquid funds pale in comparison to the 12-15% returns generated by equity mutual funds.

But as Albert Einstein rightly said, 'if you judge a fish by its ability to climb a tree, it will live its whole life believing that it is stupid'. So, this comparison between equity funds and liquid mutual funds is downright cruel. The truth is that even the smartest and the wisest of investors invest religiously in the best liquid funds to safeguard their equity investments. So, instead of thinking of liquid funds as a waste of investment opportunity, think of them as a shield for your equity investments.

[Must Read: All You Wanted to Know About Liquid Mutual Funds]

And whether or not you agree, everyone needs a shield, a contingency plan, even the greatest investor in the world, Mr Warren Buffett. In his annual letter to the shareholders of Berkshire Hathaway, it was revealed that the company holds $144 Billion in cash and cash equivalents, out of which $120 Billion is held in US Treasury bills maturing in less than one year. Now, don't you think that one of the greatest investors of the 21st century could have found a more productive use for $144 Billion? Then, why does he insist on holding billions of dollars in cash, earning less than 1% a year?

The reason is simple...Disaster can strike anytime, and only the ones that are prepared can survive. Remember, your contingency plan must have a contingency plan for its own contingency plan. And contrary to urban myth, a bank fixed deposit is not the ideal way forward. The smartest way to create a contingency plan is to invest in the best liquid funds. So, which are the best liquid mutual funds to invest in 2022? Well, this is exactly what we will answer in this article. But before we do that, let us answer the more pressing question, 'What is a liquid mutual fund?'

What is a Liquid Mutual Fund?

The Securities and Exchange Board of India defines a liquid mutual fund as, 'an open-ended liquid scheme investing its assets in debt and money market securities with a maturity of up to 91 days only.' The debt and money market securities that liquid funds invest in include the following -

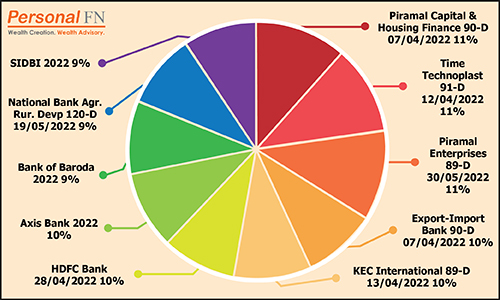

The pie chart below shows the top 10 holdings (as of March 31, 2022) of Quant Liquid Fund, which is one of the top-performing liquid mutual funds of 2022.

Graph 1: Top 10 Holdings of Quant Liquid Fund

(Source: Ace MF, PersonalFN Research)

(Source: Ace MF, PersonalFN Research)

*Portfolio as of March 31, 2022

One thing to remember about liquid funds is that they have to invest in debt and money market instruments maturing in less than 91 days. This one crucial feature (of short-term maturity) makes them immune to interest rate changes in the market. This is why liquid mutual funds are ideal for contingencies or parking your surplus funds for the short term. While the concept of liquid funds is quite simple to comprehend, investors do have certain myths when it comes to liquid funds. Let us clear these myths one by one to establish a sound and correct understanding of liquid funds.

Myths Surrounding Liquid Mutual Funds

-

Liquid Funds Are Risk-Free: This is the biggest myth when it comes to liquid mutual funds. Let us set the record straight - Liquid mutual funds are not risk-free. In fact, liquid funds investing in debt papers with poor credit ratings are extremely risky. A classic example of this was the IL&FS default in September 2018. ICRA downgraded the short-term credit rating of the commercial papers of IL&FS to D (default) from A4. Its corporate bonds were downgraded to BB from AA+. This sent shockwaves through the entire debt fund industry.

Investors who had invested in liquid funds thought they would be spared. But they were in for a shock. Liquid funds like Principal Cash Management Fund, whose exposure to IL&FS was roughly Rs 102 crore, fell by 5.72% in a single day (as of September 24, 2018). So, to reiterate, liquid funds are not 100% safe. But don't lose hope. There is a way out. You should invest in only those liquid funds having maximum exposure to papers issued by the government and public sector entities. This way, you are protected against default risk.

-

The NAV of Liquid Mutual Funds Does Not Fluctuate: This is another big area of confusion among liquid fund investors. While the fluctuations in the NAV of liquid mutual funds are way less compared to equity funds, but it exists. In fact, there have been times when the NAV of liquid funds has corrected sharply. For example, the NAV of Taurus Liquid Fund fell by nearly 7% in a single day in February 2017. The reason was the downgrade of the Ballarpur commercial papers, to which Taurus liquid fund had an exposure of Rs 1,639 crore. So, always remember that the NAV of liquid funds can also experience sharp declines.

-

Liquid Mutual Funds Are Only for Conservative Investors: Many investors believe that liquid mutual funds are ideal for only conservative investors. To this, we ask, 'are aggressive investors resistant to market ups and downs?' The answer is No. So, while conservative investors prefer liquid mutual funds, even aggressive investors can use liquid funds not just for contingency creation but also for smarter investments in equity funds.

[Check out: Systematic Transfer Plan (STP) Calculator]

We are referring to a systematic transfer plan (STP). An STP gives you the option to invest a lumpsum amount in a liquid fund and then route a fixed sum every month in the equity fund of your choice. This is a win-win situation for the investors as they can avoid investing a lumpsum amount in equity funds at market tops and earn returns on balance in liquid funds.

[Read More: 4 Benefits of Using an STP Option Smartly]

How Much to Invest in Liquid Funds?

The next thing that investors struggle with the most is in deciding how much to invest in liquid mutual funds. The simple answer is that 50% of your contingency fund should be invested in liquid mutual funds. So, how much contingency fund should you have? The rule of thumb says that you should set aside at least 12-24 months' worth of mandatory expenses (including EMIs) as a contingency fund. So, if your monthly expenditure is Rs 25,000, then your contingency fund should be worth Rs 3 Lakh to Rs 6 Lakh.

[Read More: Are you holding an Adequate Emergency Fund amidst the 3rd Wave of the Covid-19 Pandemic]

Now there is a reason why we recommend investing only 50% and not 100% of the contingency fund in liquid funds. Redemption from a liquid mutual fund takes one working day to process, whereas you can redeem from your bank fixed deposits (albeit with a penalty) in a matter of minutes with internet banking. Hence, you should invest 50% of your contingency fund in a bank savings account or a fixed deposit, with the remaining 50% invested in liquid mutual funds.

Now there are ways in which you can earn higher returns from your bank savings account as well as using the sweep-in-FD facility. So, you fix an amount of, say, Rs 20,000 with your bank. Anytime your account balance exceeds Rs 20,000, the surplus amount will be shifted to a fixed deposit, where it will earn higher returns. So, you get the basic savings account rate on Rs 20,000 and a fixed deposit rate on your surplus balance.

[Read More: Arbitrage Funds Vs Liquid Funds Vs Savings Bank Account]

How are Liquid Mutual Funds Taxed?

Liquid mutual funds follow debt taxation. So, the holding period for liquid funds from a tax angle is 3 years or 36 months. if you sell your liquid fund units before 3 years, you pay a short term capital gains tax in line with your income tax slab. Assuming you fall in the 30% tax bracket, then your short term capital gains tax on liquid fund is 30%. On the contrary, if you sell your liquid fund units after 3 years, you qualify for long term capital gains tax, which is taxed at 20% after indexation. Indexation significantly reduces the tax payable and is one of the reasons for the superiority of liquid funds over bank fixed deposits.

[Read More: Liquid Funds Vs Short-Term Deposits: Which is Better?]

Now before we reveal the list of the best liquid funds to invest in 2022, it is important for you to note that there might be a few surprises on our list. This is because one of our most crucial parameters while recommending the best liquid funds is the funds exposure to papers issued by private institutions. As a rule, we avoid liquid funds with high (more than 20%) exposure to private issuers. This helps our readers and investors avoid default risk, which is highly prevalent in debt mutual funds. With this, let us finally look at the three best liquid mutual funds to invest in 2022.

Three Best Liquid Mutual Funds to Invest in 2022

*NAV as on April 13, 20222

**AUM as of March 31, 2022

*Please note, this table only represents the best performing Liquid Funds based solely on past returns and is NOT a recommendation. Mutual Fund investments are subject to market risks. Read all scheme related documents carefully. Past performance is not an indicator for future returns. The percentage returns shown are only for an indicative purpose. Speak to your investment advisor for further assistance before investing.

Quantum Liquid Fund is one of the safest liquid funds in India as it invests a 100% of its corpus in debt instruments like treasury bills, commercial papers and debentures issued by government and public sector entities. Almost 48.12% of the fund's corpus is invested in Reserve Bank of India's 91-Day Treasury Bills. The fund carries low risk and its average credit rating is AAA. The best part is that the fund has zero exposure to debt instruments issued by private companies, which drastically reduces its default risk. The fund has generated a return of 3.33% in the last one year as of April 12, 2022.

Parag Parikh Liquid Fund is a fairly new entrant to the liquid fund space. It was launched on May 11, 2018. Despite being a new fund, it has managed to accumulate an impressive Assets Under Management of Rs 1,327 crore as of March 31, 2022. Like Quantum, Parag Parikh Liquid Fund is heavy-weight on RBI treasury bills and holds nearly 65% of its assets in RBI T-bills. However, it does hold 1.3% of its assets in CPs and term deposits of Axis Bank and HDFC Bank. The fund has generated an impressive return of 3.34% in the last one year as of April 12, 2022.

JM Liquid Fund is a veteran liquid fund having being launched in December 1997. The fund does carry higher risk compared to Quantum Liquid Fund and Parag Parikh Liquid Fund as it invests heavily in CPs and CDs issued by private issuers like Godrej & Boyce Manufacturing Ltd, L&T Finance, and Piramal Capital & Housing Finance Ltd etc. This is one of the reasons why the fund has managed to generate an above-average return of 3.42% against its peers in the last one year as of April 12, 2022.

This concludes our discussion on The Best Liquid Funds to Invest in 2022. If you wish to have super compressive and detailed research reports on the best liquid funds to invest in 2022, consider subscribing to PersonalFN's premium research service, DebtSelect.

PersonalFN's DebtSelect service provides insightful and practical guidance on which mutual fund schemes to Buy, Hold, and Sell. At PersonalFN, we apply a host of qualitative and quantitative parameters using the S.M.A.R.T score matrix.

S - Systems and Processes

M - Market Cycle Performance

A - Asset Management Style

R - Risk-Reward Ratios

T - Performance Track Record

The stringent process has helped our valued mutual fund research subscribers to own some of the best mutual fund schemes in their investment portfolio with a commendable long-term performance track record.

PersonalFN's service is apt if you are looking for insightful guidance and recommendations on some worthy funds having high growth potential in the years to come.

If you are serious about investing in a rewarding mutual fund scheme, subscribe now!

Warm Regards

PersonalFN Content & Research Team

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds

DISCLOSURE AS PER SECURITIES AND EXCHANGE BOARD OF INDIA (RESEARCH ANALYSTS) REGULATIONS, 2014

About the Company including business activity

Quantum Information Services Private Limited (QIS) was incorporated on December 19, 1989.

QIS was promoted by Mr Ajit Dayal with an objective of providing value-based information/views on news related to equity markets, the economy in general, sector analysis, budget review and various personal products and investments options available to the Public. It was the first company to start equity research on an institutional level.

'PersonalFN' is a service brand of QIS and was started in the year 1999. In 1999, the Company registered the Domain name www.personalfn.com for providing information on mutual funds and personal financial planning, financial markets in general, etc. and services related to financial planning and research in various financial instruments including mutual funds, insurance and fixed income products to customers. It offers asset allocation and researched investment recommendations through its financial planning services.

Quantum Information Services Private Limited (QIS) is registered as Investment Adviser under SEBI (Investment Adviser) Regulations, 2013 and having Registration No.: INA000000680. In terms of the second proviso to Regulation 3 (1) of SEBI (Research Analysts) Regulations, 2014 the Company is not required to obtain Certificate of registration from SEBI.

Disciplinary history

There are no outstanding litigations against the Company, its subsidiaries and its Directors.

Terms and condition on which its offer research report

For the terms and condition for research report click here.

Details of associates

-

Money Simplified Services Private Limited;

-

PersonalFN Insurance Services India Private Limited;

-

Equitymaster Agora Research Private Limited;

-

Common Sense Living Private Limited;

-

Quantum Advisors Private Limited;

-

Quantum Asset Management Company Private Limited;

-

HelpYourNGO.com India Private Limited;

-

HelpYourNGO Foundation;

-

Natural Streets for Performing Arts Foundation;

-

Primary Real Estate Advisors Private Limited;

-

HYNGO India Private Limited;

-

Suresh Lulla;

-

I V Subramaniam;

-

Murali Ananthan Krishnan.

Disclosure with regard to ownership and material conflicts of interest

-

‘subject company’ is a scheme on which a buy/sell/hold view or target price is given/changed in this Research Report;

-

Neither QIS, it's Associates, Research Analyst or his/her relative have any financial interest in the subject Company;

-

Neither QIS, it's Associates, Research Analyst or his/her relative have actual/beneficial ownership of one per cent or more securities of the subject Company, at the end of the month immediately preceding the date of publication of the research report;

-

Neither QIS, it's Associates, Research Analyst or his/her relative has any other material conflict of interest at the time of publication of the research report except that QIS (PersonalFN) is, as per SEBI (Mutual Funds) Regulations 1996, an associate / group Company of Quantum Asset Management Company Private Limited and Trustees and Sponsor of Quantum Mutual Fund (QMF) and to that extent there may be conflict of interest while recommending any schemes of QMF. However, any such recommendation or reference made is based on the standard evaluation and selection process, which applies uniformly for all Mutual Fund Schemes. The payment of commission (upfront / annualized & trail), if any, for any Schemes by QMF to QIS (PersonalFN) is also at arm's length and as per prevailing market practices.

Disclosure with regard to receipt of Compensation

-

Neither QIS nor it's Associates have received any compensation from the subject Company in the past twelve months;

-

Neither QIS nor it's Associates have managed or co-managed public offering of securities for the subject Company;

-

Neither QIS nor it's Associates have received any compensation for investment banking or merchant banking or brokerage services from the subject Company;

-

Neither QIS nor it's Associates have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months.

-

Neither QIS nor it's Associates have received any compensation or other benefits from the subject Company or third party in connection with the research report

General disclosure

-

The Research Analyst has not served as an officer, director or employee of the subject Company.

-

QIS or the Research Analyst has not been engaged in market making activity for the subject Company.

Click here to read PersonalFN's Mutual Fund Rating Methodology

Subject Company means Mutual Fund Schemes

Quantum Information Services Private Limited CIN: U65990MH1989PTC054667 Regd. & Corp. Office: 103, Regent Chambers, 1st Floor, Nariman Point, Mumbai - 400 021

Email:info@personalfn.com Website: www.personalfn.com Tel.: 022 61361200 Fax.: 022 61361222 SEBI-registered Investment Adviser. Registration No. INA000000680, SEBI (Investment Advisers) Regulation, 2013