Are Corporate Bonds Turning Attractive Now?

Listen to Are Corporate Bonds Turning Attractive Now?

00:00

00:00

The recent COVID-19 induced lockdown and slow economy, made RBI adopt certain liquidity measures to deal with the situation along with drop in rate, in turn favoured issuance of corporate bonds.

A recent reporting from the Bloombergquint stated that “Bond issues from Indian corporates jumped 75% in the April-August”. The Reserve Bank undertook expansionary monetary policy measures to ensure the availability of adequate liquidity in the system.

COVID-19 has imparted scars on monetary and credit aggregates towards the end of the fiscal year 2019-2020 and beginning of FY2021. But as seen below from the SEBI data till June 2020 quarter it was down though.

Graph 1: Rising/decreasing number of issues of corporate bonds

(Source: SEBI Corporate bond page)

The Corporate Bonds form an integral part of India’s liquidity system. Corporate bonds are debt securities issued by private and public corporations. Companies issue corporate bonds at a pre-specified coupon, in order to raise money for a variety of purposes, such as building a new plant, purchasing equipment, or growing the business.

Corporate bonds tend to rise in value when interest rates fall, and they fall in value when interest rates rise. Usually, the longer the maturity, the greater is the degree of price volatility. By holding a bond until maturity, one may be less concerned about these price fluctuations (which are known as interest-rate risk), because one can expect to receive periodic coupons along with the par, or face, value of the bond at maturity. Provided the bond issuer meets the obligation and does not default on its commitments.

The demand for corporate bonds as an investment is mostly confined to institutional investors who are in turn constrained by prudential norms for investment as in the case of the insurance companies and mutual funds.

Corporate Bonds market update

Corporate bond yields largely track Government-secyields.The financial conditions started easing out substantially and systemic liquidity remains in large surplus, due to the conventional and unconventional measures by the Reserve Bank since February 2020. These measures assured liquidity of the order of Rs 9.57 lakh crore.

The government spending remained subdued in July. During 2020-21 (up to July 31), Rs1,24,154 crore was injected through open market operation (OMO) purchases. In order to distribute liquidity more evenly across the term structure and improve transmission, the Reserve Bank conducted ‘operation twist’ auctions involving the simultaneous sale and purchase of government securities for Rs 10,000 crore on July 2, 2020.

However, yields registered some uptick in March 2020 with the unfolding of distress in a major private bank and COVID-19. The transmission to bank lending rates improved further, with the weighted average lending rate (WALR) on fresh rupee loans declined by 91 bps during March-June 2020.

The spreads of 3-year AAA rated corporate bonds over G-Secs of similar maturity declined from 276 bps on March 26, 2020 to 50 bps by end-July 2020. Even for the lowest investment grade bonds (BBB-), spreads dropped by 125 bps by end-July 2020. Lower borrowing costs have led to record primary issuance of corporate bonds of ₹2.1 lakh crore in the first quarter of 2020-21.

This was addressed by the announcement of various liquidity measures by the Reserve Bank on the back of a sizeable reduction in the policy rate. Overall, the 5-year AAA-rated corporate bond yield eased by 108 bps to 7.02 per cent during 2019-20a year ago.

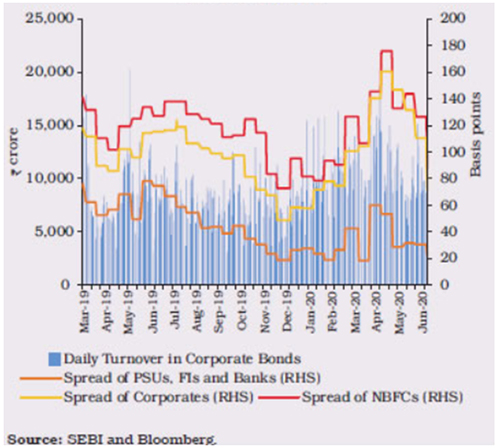

Graph 2: Turnover in corporate bond market and yield spread

(Source: RBI's Annual Report)

Primary corporate bond issuances increased by 6.6 per during 2019-20 as softening of yields encouraged corporates to mobilise higher resources from the corporate bond market, particularly public sector entities.

Private placements remained the preferred choice for corporates, accounting for 97.8 per cent of total resources mobilised through the bond market.

In order to provide an alternative source of financing for public sector entities at lower cost and help deepen bond markets by diversifying investor base with increased retail participation, the Government of India (GoI) launched the Bharat Bond Exchange Traded Fund (ETF) in December 2019 - the first ETF for corporate bonds in India - under which ₹12,395 crore were mobilised.

Outstanding corporate bonds increased by 6.1 per cent y-o-y to ₹32.5 lakh crore or 16.0 per cent of GDP at end-March 2020 and for June quarter it has grown by 16%. Investments by FPIs in corporate bonds decreased to ₹1.73 lakh crore at end-March 2020 as compared to ₹2.19 lakh crore at end-March 2019.

Graph 3: Corporate bonds outstanding amount surging

(Source: SEBI Corporate bond page)

Where are corporate bonds heading?

COVID-19 has likely put a burden on debt servicing, especially private issuers. The extended lock down has disrupted their business line proceedings and revenues resulting in an increased pressure, and chances of default.

After the recent spate of eventsthat occurredwhich dented the fund houses and hurt the investors hard, the government asked fund houses to increase their portfolio allocation of some categories of debt mutual funds to government securities. The fund houses have complied and current dent caused has made them cautious.

[Read: Lessons Learnt from the Debt Fund Crisis]

Now after RBI announced loan moratoriums and further decided not to classify them as NPA. Moreover, it provided a window for loan recasting in order to boost the economy by infusing liquidity.

On the backdrop of the uncertainty surrounding the inflation outlook and taking into consideration the extremely weak state of the economy amid an unprecedented shock from the ongoing pandemic, the Monetary Policy Committee of the RBI chose to pause the rate cuts and remain watchful of incoming inflation data.

This stance has actually pushed private entities for more credit borrowingto sustain their business, although their balance sheets may not look healthy to service debt obligations. In a thirst of fresh funds, some moderate to low rated private entities may be willing to offer attractive yields to bond investors. Given the interest rates are trending at a multi-year low, investments in corporate bonds offering higher coupon may look attractive, but probably comes with an elevated credit risk.

What should debt fund investors do?

Government securities carry higher credit rating compared to the corporate debt instruments. While those looking to earn high yields, may find corporate debt instruments having moderate to high rating attractive, one should not forget the higher credit risk associated with them.

Remember, investing in debt funds is not risk-free.

While investing in corporate bond funds, investors need to understand that the ratings of any corporate debt instruments cannot be the same across. A downgraded paper may be assigned a good rating if its credit quality has improved, but that does not mean that you should invest in schemes with toxic papers.

The most important thing investors can do is to choose your investment options wisely based on the following parameters:

-

Your investment tenure,

-

Your risk profile,

-

Your financial circumstances

-

The fund house's characteristics, that highlights investments systems and the process followed,

-

The experience of the fund manager,

-

Assess if the credit quality and the maturity profile of the investment papers held is congruent with your risk profile

However, do note that the past performance of corporate bond fund is in no way indicative of the future performance of the scheme. So thoroughly analyse all aspects before investing.

Corporate Bond funds are suitable for investors having moderate-to-high risk appetite. They are ideal for short-term investment goals ranging from a few days months to as many as two to three years or more.Lastly, while investing in debt mutual funds prefer the safety of capital over returns.

PS: If you wish to select worthy mutual fund schemes, subscribe to PersonalFN's unbiased premium research service, FundSelect.

Additionally, as a bonus, you get access to PersonalFN's popular debt mutual fund service, DebtSelect.

If you are serious about investing in a rewarding mutual fund scheme, Subscribe now!

Warm Regards,

Aditi Murkute

Senior Writer

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds