SEBI Brings In New Norms to Improve Transparency in Debt Securities Transaction by Mutual Funds

Listen to SEBI Brings In New Norms to Improve Transparency in Debt Securities Transaction by Mutual Funds

00:00

00:00

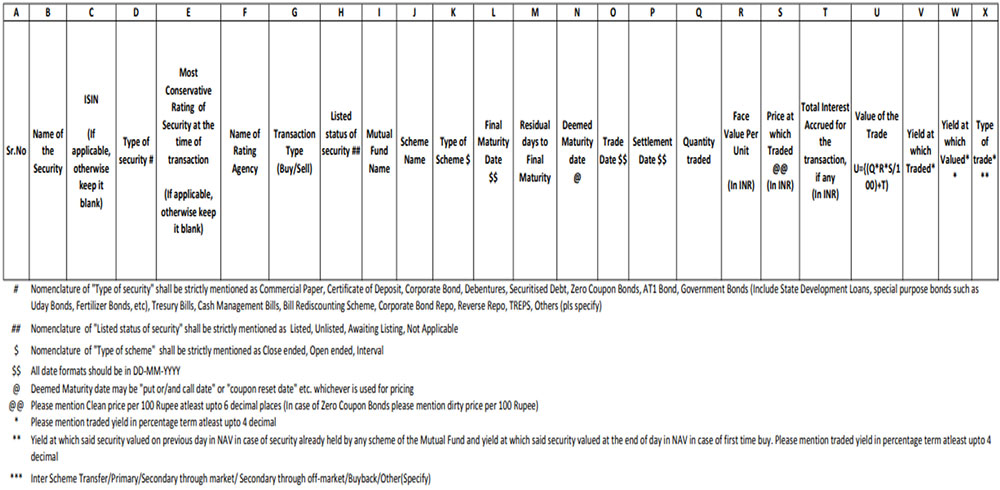

With effect from October 01, 2020, mutual funds will be required to disclose the details of debt and money market securities transacted (including inter-scheme transfers) in its schemes in a new prescribed format. The format, as shown in the table below, includes details such as the name and type of security, credit rating, name of the rating agency, maturity date, settlement date, interest accrued, and yield, among others.

Mutual Funds will have to disclose details of the schemes' transaction on a daily basis with a time lag of 15 days as compared to the time lag of 30 days that is permitted at present. Additionally, the disclosure should be presented in a comparable, downloadable (spreadsheet) and machine-readable format.

Table 1: Format for reporting of all transactions in debt and money market securities

(Source: sebi.gov.in)

(Source: sebi.gov.in)

The revised format is more comprehensive and contains information like rating of the security at the time of transaction, whether the security is listed, put/call option date, yield at which the security was traded, type of trade (inter scheme transfer/primary/secondary market, etc.), which was not available in the previous format.

Moreover, SEBI has asked all debt schemes to disclose portfolio on fortnightly basis within five days of every fortnight with effect from October 01, 2020. Currently, funds disclose portfolio on a monthly basis. However, disclosure of portfolio on a monthly basis may not reveal the complete picture of the portfolio quality, especially in case of shorter duration funds, which invest in securities with short-term maturity.

(Image source: photo created by ijeab - www.freepik.com)

(Image source: photo created by ijeab - www.freepik.com)

For example, the six shuttered debt schemes of Franklin Templeton had faced heightened redemption pressure and increased borrowings in the days leading up to winding-up. If there was a norm for mandatory fortnightly disclosure at that time, it would have made the investors/financial advisers aware about the pressure the fund had been dealing with and they could have taken the necessary preemptive action.

The above-mentioned norms could give investors a better sense of the risk factor and thus enable them to make an informed investment decision. The move could also prevent funds from taking higher credit risk through short-term transactions in a bid to earn high yield. Thus, it would help investors to watch out for early warning signs and save themselves from any potential risk the fund could be exposing them to.

Update on the shuttered Franklin Templeton schemes

Even as SEBI has intensified its pace to fix debt funds, fresh default by Future Group companies has added to the woes of investors in the wound up schemes of Franklin Templeton mutual funds (FTMF). Rivaaz Trade Ventures Pvt Ltd (RTVPL), part of the Kishori Biyani-owned Future Group of companies defaulted on its debt obligation due on August 31, 2020.

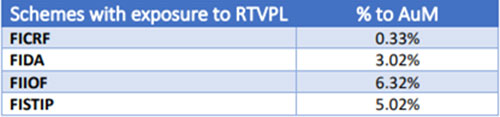

Four of the six schemes of Franklin Templeton MF, namely Franklin India Credit Risk Fund (FICRF), Franklin India Dynamic Accrual Fund (FIDAF), Franklin India Income Opportunities Fund (FIIOF), and Franklin India Short Term Income Plan (FISTIP) which were wound up, have exposure to the NCDs of RTVPL.

The security, which was trading at 75% after applying the standard haircut, will now be valued at zero as per AMFI norms. Consequently, NAVs of the schemes have dropped by up to 6.3%.

Table 2: Scheme-wise exposure details as on August 31, 2020

(Source: Franklin Templeton Mutual Fund)

(Source: Franklin Templeton Mutual Fund)

However, the silver lining is that Reliance Retail recently announced acquisition of retail, wholesale, logistics, and warehousing business of the Future Group for a consideration of Rs 24,713 crore. As a part of the sale, Future Group will be looking at amalgamating some of its business into Future Enterprise Ltd (FEL) and is expected to raise Rs 2,800 crore through a combination of equity shares and warrants. Reliance Retail will hold around 13.1% in FEL (post-merger).

FTMF expects that above-mentioned transaction will enable fulfilling of the NCD obligation. It has stated that the proposed sale is subject to regulatory and other legal approvals.

What should debt fund investors do?

In the current scenario where credit risk has amplified, it is important to be extra cautious while investing in debt funds. Ideally, stay away from funds with high exposure to private issuers.

To select a scheme, essentially assess your risk appetite and investment time horizon, plus factors such as:

-

The portfolio characteristics of the debt schemes

-

The average maturity profile

-

The corpus & expense ratio of the scheme

-

The rolling returns

-

The risk ratios

-

The interest rate cycle

-

The investment processes & systems at the fund house

At PersonalFN, we arrive at top rated funds using our SMART Score Model. If you wish to select worthy mutual fund schemes, I recommend that you subscribe to PersonalFN's unbiased premium research service, FundSelect.

Additionally, as a bonus, you get access to PersonalFN's popular debt mutual fund service, DebtSelect.

If you are serious about investing in a rewarding mutual fund scheme, Subscribe now!

Warm Regards,

Divya Grover

Research Analyst

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds