RBI Kept Policy Rates Unchanged. Which Debt Mutual Funds Should You Invest In Now?

Listen to RBI Kept Policy Rates Unchanged. Which Debt Mutual Funds Should You Invest In Now?

00:00

00:00

The Reserve Bank of India (RBI) kept the policy rates unchanged at the third bi-monthly monetary policy review conducted between August 4 and August 6, 2021. This was the seventh successive time a status quo and accommodative stance were maintained.

All the six members of the Monetary Policy Committee (MPC) voted in favour of keeping the policy rate unchanged. Except for Prof. Jayanth R. Varma, all members backed to continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

The assessment drawn by the MPC about the present macro-economic environment indicated that demand remains weak despite some improvements. RBI also voiced its concerns over the supply-side bottlenecks and stated that "more needs to be done to restore the demand-supply balance in a number of sectors of the economy".

The RBI decided to prioritise economic revival as the main policy objective and overlook rising inflationary pressure. The tone of the governor's statement suggested that any pre-mature policy response to curtail inflation at this juncture might adversely affect the feeble economic recovery The FY22 GDP growth expectation was retained by the RBI at 9.5% consisting of 21.4% growth in Q1FY22, 7.3% in Q2, 6.3% in Q3 and 6.1% in Q4.

As regards CPI inflation, taking into consideration the upside risk emanating from rising input cost across the manufacturing and services sector, elevated levels of fuel prices with their second-round effects, and logistics cost; the RBI revised its FY22 inflation projection to 5.7% (5.9% in Q2; 5.3% in Q3; and 5.8% in Q4 of 2021-22) from 5.1% stated in the policy review conducted in June 2021. However, the medium-term target for CPI inflation is still retained at 4.00% within a band of +/- 2% while supporting growth. The MPC seemed conscious of its objective of anchoring inflation expectations.

Table: Series of policy rate cuts to address growth concerns

| Month |

Repo Policy Rate |

Policy rate cut (Basis points) |

Monetary Policy Stance |

| Feb-2019 |

6.25% |

25 |

Neutral |

| Apr-2019 |

6.00% |

25 |

Neutral |

| Jun-2019 |

5.75% |

25 |

Accommodative |

| Aug-2019 |

5.40% |

35 |

Accommodative |

| Oct-2019 |

5.15% |

25 |

Accommodative |

| Dec-2019 |

5.15% |

Status quo |

Accommodative |

| Feb-2020 |

5.15% |

Status quo |

Accommodative |

| Mar-2020 (an exceptional off-cycle meeting) |

4.40% |

75 |

Accommodative |

| May-2020 (an exceptional 2nd off-cycle meeting) |

4.00% |

40 |

Accommodative |

| Aug-2020 |

4.00% |

Status quo |

Accommodative |

| Oct-2020 |

4.00% |

Status quo |

Accommodative |

| Dec-2020 |

4.00% |

Status quo |

Accommodative |

| Feb-2020 |

4.00% |

Status quo |

Accommodative |

| April-2021 |

4.00% |

Status quo |

Accommodative |

| June-2021 |

4.00% |

Status quo |

Accommodative |

| Aug-2021 |

4.00% |

Status quo |

Accommodative |

| Total |

|

250 |

|

Data as of August 6, 2021

(Source: RBI Monetary Policy Statements)

Between February 2019 and now, RBI has reduced policy rates by 250bps on a cumulative basis. The policy transmission during the current interest rate cycle has been satisfactory with a cumulative reduction of 217 bps in the Weighted Average Lending Rate (WALR). The willingness of banks to pass on the benefits of lower interest rates to the borrowers, weaker credit growth has also promoted better policy transmission this time. That said, at 6.5% credit growth still appears lacklustre.

The liquidity conditions in the financial system remained very comfortable during the period under review with M3 money supply expanding at 10.8% (against 9.9% recorded in the previous review period). The daily average absorption under the reverse repo window increased from Rs 5.7 lakh crore in June to Rs 8.5 lakh crore in the first week of August. The RBI has been taking a series of measures to ensure that liquidity in the system remains comfortable.

The RBI has decided to increase the absorption under the 14-day variable rate reverse repo (VRRR) by Rs 50,000 crore on an incremental basis, starting from August 13, 2021. The RBI is planning to conduct VRRR auctions worth Rs 4 lakh crore at the end of September 2021. VRRR will absorb the excess liquidity in the system.

Also, RBI has taken the decision to extend the scheme of on-tap Targeted Long Term Repo Operation (TLTRO) by three months, i.e. upto December 2021. This move is expected to offer liquidity support to the stressed sectors of the economy for an extended period.

Furthermore, the RBI plans to carry out more Open Market Operations (OMOs) in August (Rs 25,000 crore each on August 12 and August 26, 2021) under its secondary market G-Sec Acquisition Programme (G-SAP) and Operation Twist (OTs) in line with the evolving macroeconomic and financial conditions to anchor the yield expectations.

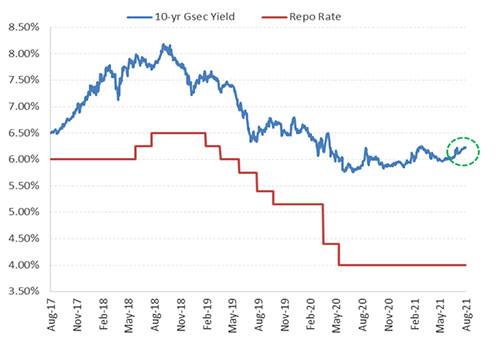

Graph: The 10-year benchmark yields are well- anchored around 6.00%

Data as of August 10, 2021

Data as of August 10, 2021

(Source: Investing.com, PersonalFN Research)

A series of conventional and unconventional measures taken by the RBI to actively manage the liquidity in the system have kept the 10-year G-sec yield well-anchored to around 6.00%, which has comforted the Indian debt market.

The RBI is mopping up excess liquidity at the short end of the yield curve and injecting more liquidity at the long end of the curve. This seems to be an attempt to move gradually towards policy normalization.

That being said, note that policy normalization will be contingent upon several factors including:

-

Magnitude and timing of the third wave

-

The pace of vaccination

-

CPI inflation trajectory

-

Kharif crop acreage and rabi sowing

-

Pick up in the capex cycle

-

Trends in tax collections

-

Government's fiscal position

-

How the global economy fares

Any delay in the economic recovery may result in a continuation of the accommodative monetary policy stance. If growth momentum picks up in the subsequent quarters and inflation remains sticky, RBI's policy approach may turn neutral from accommodative.

The RBI will keep a close watch on all these factors, mainly inflation, in maintaining the macro-economic stability and credibility of the framework.

Considering these scenarios it appears that we are almost at end of the current interest rate cycle, wherein rates have bottomed out. In other Emerging Market Economies (EMEs) such as Brazil, Mexico, and Russia the central banks have already raised interest rates.

The RBI may undertake policy normalization in a calibrated manner, ignoring inflationary pressure is going to become increasingly challenging for the MPC. Rising commodity prices (food and non-food), high shipping charges, and supply chain disruptions in some key products are already pushing CPI inflation up. If CPI inflation continues to move up for consecutive 2-3 months, the RBI may be left with no other option but to gradually increase policy rates sooner. In other words, the policy normalisation period would shorten.

The RBI, however, would ensure that liquidity conditions in the system remain comfortable. If RBI continues to flush out more liquidity through various market operations, and inflation stays higher than the revised estimates, markets may start factoring in a potential repo rate hike sooner rather than later.

(Image source: pixabay.com; photo created by geralt)

(Image source: pixabay.com; photo created by geralt)

How should you approach debt funds after the RBI's third bi-monthly monetary policy review?

Avoid taking exposure to longer duration debt funds. Most of the rally at the longer end of the yield curve has already come about since the time RBI started reducing policy rates. Debt securities with longer maturity papers may not be able to generate attractive returns, as seen in the last couple of years. Moreover, in the current uncertain times, the longer end of the yield curve could be more sensitive than the shorter end. The returns may be moderate on the longer end of the yield curve and could turn riskier (may encounter high volatility) in the foreseeable future.

To approach debt mutual funds, now the shorter end of the yield curve looks more attractive. You'll be better off deploying your hard-earned money in shorter duration debt mutual funds. But approach even short-term debt funds with your eyes wide open--pay attention to the portfolio characteristics and quality of the scheme.

Stay away from debt mutual fund schemes that have exposure to low-rated securities in the hunt for yield amid a time when the credit risk has intensified. Stick with debt mutual funds where the fund manager does not chase yields by taking higher credit risk, but instead focuses on government and quasi-government securities. Amid the pandemic, since the credit risk has intensified, as far as possible, avoid Credit Risk Funds as they are likely to be more vulnerable.

Debt funds have witnessed various credit events in the past which led to an erosion of wealth for investors. It can take a long while for a scheme to fully recover from any setback that defaults and downgrades cause.

So when you invest in debt funds, focus on the safety of capital instead of chasing returns. Check if your debt fund manager is eyeing higher yields by exposing your investment to higher credit risk instruments issued by private issuers. Trusting a rating profile of a fund blindly can expose the portfolio to credit risk.

In the current times, you would do better going with pure Liquid Funds and/or Overnight Fund that does not have exposure to private issuers. Assessing your risk appetite and investment horizon, you may consider ultra-short and short duration debt funds that have impeccable portfolio characteristics. In general, keep in mind that investing in debt funds is not risk-free.

Before investing in debt funds understand the various risks involved viz. credit risk, duration risk, interest-rate risk, liquidity risk, etc., and invest in schemes where the fund's portfolio risk aligns with your own risk appetite and financial objectives.

The important parameters to consider when selecting the best debt fund are:

-

The rolling returns

-

The risk ratios

-

The interest rate cycle

-

The portfolio characteristics of the debt scheme

-

The average maturity profile

-

The corpus & expense ratio of the scheme

-

The investment processes & systems at the fund house

If you are looking for quality mutual fund schemes to add to your investment portfolio, I suggest subscribing to PersonalFN's premium research service, FundSelect. Currently, with the subscription to FundSelect, you could also get Free Bonus access to PersonalFN's Debt Fund recommendation service DebtSelect.

Under DebtSelect, we give high weightage to schemes displaying worthy portfolio characteristics. We avoid debt mutual fund schemes that aim for higher yields by taking undue higher credit risk with substantial exposure in instruments issued by private issuers.

At PersonalFN we follow a S.M.A.R.T Score Matrix, wherein we evaluate:

-

S - Systems and Processes

-

M - Market Cycle Performance

-

A - Asset Management Style

-

R - Risk-Reward Ratios

-

T - Performance Track Record

The stringent process has helped our valued mutual fund research subscribers to own some of the best mutual fund schemes in the investment portfolio with a commendable long-term performance track record.

This service is apt if you are looking for insightful guidance and recommendations on some worthy funds having high growth potential in the years to come.

We will also help you choose some of the best Equity Linked Saving Schemes (ELSS) for your tax-saving with PersonalFN's premium research service, FundSelect.

PersonalFN's FundSelect service provides insightful and practical guidance on which mutual fund schemes to Buy, Hold, and Sell.

If you are serious about investing in a rewarding mutual fund scheme, Subscribe now!

Alternatively, if you prefer to keep your capital safe, opt for bank fixed deposits. But to ensure the security of your hard-earned money, choose the bank carefully.

Happy Investing!

Warm Regards,

Rounaq Neroy

Editor Daily Wealth Letter

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds