SEBI Tweaks Valuation Norms for Perpetual Bonds. Know What it Means for Mutual Fund Investors

Listen to SEBI Tweaks Valuation Norms for Perpetual Bonds. Know What it Means for Mutual Fund Investors

00:00

00:00

In a relief to debt mutual funds and its investors, SEBI has relaxed guidelines on the valuation of perpetual bonds.

Few days back, SEBI had issued a circular asking mutual funds to treat AT-1 bonds (Perpetual bonds) as having 100-year maturity. This sent shockwaves in the bond market because it was expected to result in a mark-to-market loss for investors in schemes that held perpetual bonds. Besides that, the finance ministry objected to the new rule and asked SEBI to revoke the circular.

What are AT-1 bonds?

AT-1 bonds (Additional Tier -1 bonds) are a type of unsecured bonds issued by banks to meet their capital requirements under the Basel III norms. They are called perpetual bonds because unlike regular bonds, these do not have tenure for maturity. AT-1 bonds carry a 'call option' which enables the issuer to redeem it at a pre-fixed interval (usually 5 year or 10 year).

However, banks are not obliged to use the call option and have the flexibility to write down the face value of bonds. In addition, banks can even skip paying interest in a year if its capital ratio falls below a certain limit. Besides, if the bank is facing losses, RBI may ask the bank to write off the AT-1 bonds. This was witnessed last year when Yes Bank wrote off its AT-1 bonds worth Rs 8,400 amid crisis as a part of the RBI's rescue plan, culminating into substantial losses for the investors.

Though AT-1 bonds carry high risk; it compensates investors with the potential of attractive yields.

Image by ijeab - www.freepik.com

As per a note by the finance ministry, mutual fund houses are the largest investors in AT-1 bonds holding over Rs 35,000 crore of the total AT-1 issuance of about Rs 90,000 crore. For valuation purpose, mutual funds currently use the call date as the bond's maturity date.

Though SEBI's move is aimed at protecting the interest of investors in schemes holding perpetual bonds, if these bonds are treated as having a 100-year tenure, there could be a sudden and significant spike in yields. Basically, the longer the maturity, the higher is the yield. As you may be aware, yield and bond prices are inversely proportional; therefore, the spike in yield could cause the NAV of schemes to reduce.

Why is the government against fixing the tenure at 100 years?

The government in a note to SEBI expressed concerns that the circular could affect their capital sourcing plans because perpetual bonds are the banks' preferred mode of raising capital. In case of public sector banks (PSB), the circular is likely to increase their reliance on the government for capital.

One of the reasons the mutual funds invest in perpetual bonds is the attractive yield; the new valuation norms could make them averse to investing in these bonds.

The government also described the clause on the valuation of perpetual bonds as disruptive, which could translate to depressed valuation of AT-1 bonds and lead to panic selling among investors.

SEBI relaxes norms

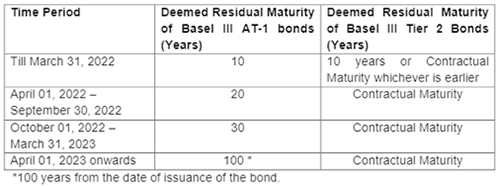

Subsequently, based on the recommendation of the mutual fund industry, SEBI has decided that the deemed residual maturity for the purpose of valuation of existing as well as new bonds issued under Basel III framework will be as below:

(Source: SEBI circular)

Further, if the issuer does not exercise the call option, then the valuation and calculation of Macaulay Duration will be done considering maturity of 100 years from the date of issuance for AT-1 Bonds and Contractual Maturity for Tier 2 bonds. In addition, if the non-exercise of call option is due to the financial stress of the issuer or if there is any adverse news, this will have to be reflected in the valuation.

All other provisions mentioned in the previous circular will remain the same which are as under:

a) Close-ended scheme

Since close-ended debt scheme are required to invest only in securities which mature on or before the date of the maturity of the scheme, such debt schemes will not be permitted to invest in perpetual bonds.

b) Limiting exposure

Mutual funds under all its schemes will cap exposure at 10% of such instruments issued by a single issuer. Further, a mutual fund scheme cannot invest more than 10% of its NAV of the debt portfolio of the scheme in such instruments; and more than 5% of its NAV of the debt portfolio of the scheme in such instruments issued by a single issuer.

With this, the regulator has allowed sufficient time to the mutual fund industry to limit/reduce their exposure in such bonds and avoid any potential disruption in the bond market. That said, with no change in the exposure limit on such bonds, some funds having higher allocation to perpetual bonds may witness some short term volatility.

Notably, it may not provide much relief to banks as they may find it difficult to find investors other than mutual funds.

What should investors do?

It is important for you to understand your preferences, time horizon, and risk appetite, and make the right choice when selecting mutual funds.

As an investor, first determine if you are looking for safety of capital or returns. If your preference is safety, then stick to funds that focus on Government and Quasi-government securities. Debt funds chasing higher yield by investing majorly in instruments issued by private issuers can be ignored because they may expose you to credit risk.

You should ideally avoid investing in schemes that have significant exposure to long duration securities in short to medium term categories such as, short duration debt funds, medium duration funds, Banking & PSU Funds, etc. Moreover, steer clear of funds having significant exposure to moderate and low rated instruments.

Watch this short video on the lessons an investor can remember while investing in Debt Mutual Funds.

The interest rates are at multi-year low due to rate cuts by the RBI to support economic growth. However, going forward government's spending programme and higher borrowing target are expected to push bond yields higher.

The longer duration instruments are more sensitive to interest rate changes as compared to shorter duration instruments. Remember that Debt funds with exposure to medium to longer duration instruments tend to be more volatile in a scenario where there is an upwards movement in interest rates.

Debt funds that have exposure to longer maturity instruments may be highly volatile going forward, while those focusing on shorter maturity instruments (such as liquid fund) and following an accrual strategy may still be better-placed to tackle the interest rate risk.

Therefore, invest in medium to long duration funds only if it matches your investment horizon and if you have the ability to handle short-term volatility. For short-term goals, you can consider investing in the debt fund category such as, liquid fund, short duration funds, ultra short duration fund, etc.

PS: If you are looking for quality mutual fund schemes, I recommend subscribing to PersonalFN's premium research service, FundSelect.

PersonalFN recommendations go through our stringent process that assesses both quantitative and qualitative parameters, providing you with Buy, Hold, and Sell recommendations on equity and debt mutual fund schemes.

Currently, with your subscription to FundSelect, you could also get Free Bonus access to PersonalFN's Debt Fund recommendation service DebtSelect. Read full details here...

Warm Regards,

Divya Grover

Research Analyst

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds