Term Life vs Traditional Life Insurance: Which Is a Better Option?

Ketki Jadhav

May 07, 2022

Listen to Term Life vs Traditional Life Insurance: Which Is a Better Option?

00:00

00:00

Life is unpredictable, and you never know what tomorrow has in store for you. Unexpected events like premature death can create emotional and financial turmoil in the family. This is why life insurance is an important investment as it compensates against the financial loss suffered in case of a demise of a family member. Choosing the best life insurance plan from hundreds of available options can be a daunting task. Hence, the first step towards buying the right life insurance policy that matches your requirements is to choose the right type of life insurance. The most common types of life insurance plans are Term Plans and Traditional Insurance-cum-Investment Plans. This article compares Term Life Insurance vs Traditional Life Insurance to help you decide which is a better option for you.

What is a Life Insurance?

Life Insurance is a contract between an insurer and a policyholder. An insurer guarantees a sum assured to the beneficiary/nominee on the policyholder's unfortunate demise in return for the premiums paid.

In simple words, Life Insurance provides financial security to your family so that they can continue living the same lifestyle without any compromises due to the financial instability caused due to the loss of an earning member.

The Insurance Regulatory and Development Authority of India (IRDAI) is the apex body that regulates the insurance sector in India.

What is a Term Insurance?

Term Insurance is basic life insurance that everyone must have, as it offers financial protection to your loved ones at an affordable premium. It is a type of life insurance that provides coverage for a certain period called 'term.' In case of the policyholder's unfortunate demise, Term Insurance provides financial protection to the policyholder's family. A policyholder is required to pay a premium for a chosen term. However, failing to do so will result in a policy lapse.

The three major factors affecting the premium are the policyholder's age, sum assured, and the policy term. The policyholder's health and medical history are also considered while calculating the premium. The sum assured is offered to the nominee in the form of a death benefit in case of the unfortunate demise of the policyholder within the policy term. You should know that the policyholder is not a beneficiary in this type of insurance because the sum assured is given to the nominee in case of the death of the policyholder. If the policyholder survives the policy term, he/she gets an option to renew the policy with a new term, but the premium is calculated considering the age and health conditions at the time of renewal. Traditionally, Term Insurance does not offer survival benefits. But, nowadays, many insurance companies are offering ample benefits as add-ons that can be purchased by paying an extra premium.

(Image Source: www.freepik.com)

(Image Source: www.freepik.com)

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds

What is a Traditional Life Insurance?

Traditional Life Insurance Policy not only covers the policyholder's life in case of an unfortunate demise but also offers a maturity benefit at the end of the policy term. Hence, the policy matures once the policy term is over, and the policyholder receives the maturity benefit. In addition to the sum assured, many insurers offer guaranteed returns and bonuses on traditional plans. The returns can be used to fulfil your long-term financial goals, such as your child's education, child's wedding, retirement, vacations, etc. The policy term of these plans is generally 10 to 20 years, and a policyholder can accumulate good returns over this period.

There are several types of traditional life insurance plans available in the market, such as whole life insurance plans, money-back policies, child plans, pension plans, etc.

Term Insurance vs Traditional Life Insurance: What is the difference?

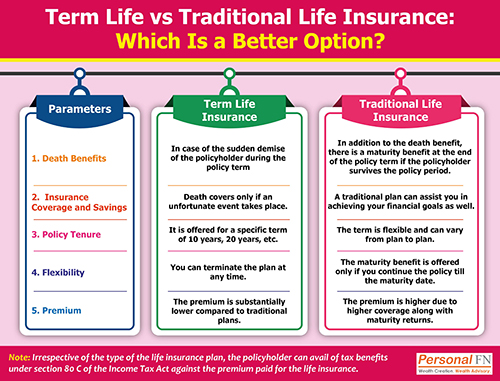

1. Death Benefit:

The major difference between the two plans is the death benefit offered by them. A term plan offers a death benefit in case of the sudden demise of the policyholder during the policy term. However, it does not offer any benefit in case the policyholder survives the policy term. Whereas traditional life insurance offers both; a death benefit in case of the demise of the policyholder or a maturity benefit at the end of the policy term if the policyholder survives the policy period.

2. Insurance Coverage and Savings:

Since term plans only provide a death benefit if an unfortunate event takes place, it is ideal if you are looking only for death cover. Whereas investing in a traditional plan can benefit you to achieve your financial goals like child's education, retirement planning, etc.

3. Policy Tenure:

As the name suggests, term plans are offered for a specific term of 10 years, 20 years, etc. The term of the traditional plan is flexible and can vary from plan to plan. For example, a policy term for a child plan could be 15 to 20 years, whereas the term applicable to Whole Life Insurance Plans is generally until the policyholder reaches 100 years.

4. Flexibility:

You can terminate your term life insurance at any time. Suppose you chose a 20-year term and want to cancel the plan after 5 years. You can terminate/close the policy by stopping the premium payment. However, in the case of traditional life insurance, the maturity benefit is offered only if you continue the policy till the maturity date. If you have to surrender the policy before maturity due to any reason, you will not be eligible to receive the saving portion of the plan as only the premium amount paid by you is credited back to you after certain deductions.

5. Premium:

As term plans offer only death benefits, the premium is substantially lower compared to traditional plans. It enables you to get the maximum sum assured at an affordable premium, which is why term life insurance policies are gaining popularity among millennials. The traditional life insurance policies offer higher coverage along with maturity returns, resulting in higher premiums that might not be affordable to everyone.

6. Tax Benefit:

Irrespective of the type of the life insurance plan, the policyholder can avail of tax benefits under section 80 C of the Income Tax Act against the premium paid for the life insurance.

Which is a better option?

Buying a life insurance policy for the first time can be overwhelming. However, the time you spend on understanding your requirements and doing thorough research to find out the right life insurance policy that suits you the best is worth it.

Although traditional plans may look more beneficial at first due to the maturity returns they offer, they might not be an ideal choice for everyone. In fact, the returns and the insurance cover offered on the traditional insurance-cum-investment plans might not be adequate considering the rate of inflation. It makes sense to buy a term plan for your life insurance needs as it is affordable and provides sufficient life insurance cover. Moreover, the amount saved on premium by investing in a term plan can be further invested in other tax-saving investment avenues. For your long-term investment goals, instead of investing in a traditional insurance-cum-investment plan, it is advisable to invest in carefully selected equity mutual funds. Having said that, before investing, make sure you do thorough research and choose the mutual fund schemes wisely, which will help you make an informed decision.

Warm Regards,

Ketki Jadhav

Content Writer