Things to Do If Your Personal Loan Application Gets Rejected

Ketki Jadhav

Apr 28, 2022

Listen to Things to Do If Your Personal Loan Application Gets Rejected

00:00

00:00

Personal loans are beneficial in emergencies and during financial crunch. These can be availed with minimum documentation and do not require any collateral. Therefore, many individuals prefer personal loans over other types of loans. With many banks and NBFCs, promoting instant personal loans aggressively, getting a personal loan to approve is much easier than before. However, When you apply for it, there can be many eligibility requirements, terms and conditions that financial institutions do not disclose upfront, which at times results in delayed processing of loans or even application rejection!

So, what to do if the bank rejects your Personal Loan application?

Do not panic! Here's what you should do if your personal loan application gets rejected:

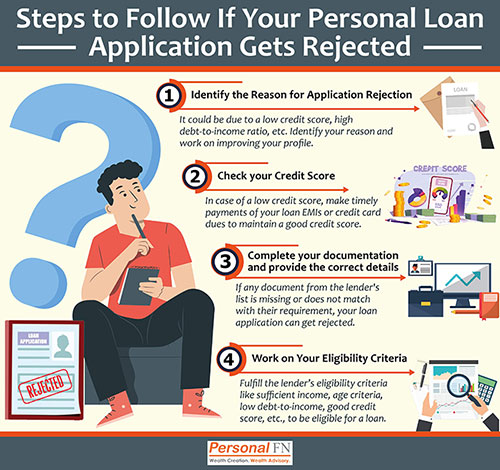

1. Identify the reason for application rejection

When you get to know your personal loan application is rejected by the lender, the first thing you should do is identify the route cause of rejection. The loan application can get rejected due to various reasons. However, once you identify the reason behind it, you can start working on improving your profile to avoid loan rejection in the future.

Let's first see what could be the possible reasons for your personal loan application rejection:

-

Insufficient credit score

-

No credit history

-

Insufficient income

-

Frequent job changes

-

Not fulfilling the age criteria

-

Inaccurate information

-

Insufficient documents

-

High debt-to-income ratio

Apart from these reasons that are in your control, there could be other reasons for rejection that are entirely dependent on the lender's lending policy. It includes unavailability of the branch at your location, your employer not listed with the lender, minimum salary requirement of the lender, etc. In this case, it is advisable to check the eligibility criteria of other lenders ad apply where your eligibility and loan requirements match the best. However, if the rejection reason is in your control and does not have anything to do with the lender's policy, you should start working on improving your profile because an emergency can strike anytime, and you never know when you will need a personal loan the next time.

(Image Source: www.freepik.com)

(Image Source: www.freepik.com)

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds

2. Check your credit score and work on improving it:

A credit score represents your creditworthiness. Generally, a credit score above 700 is considered good; having a credit score above 750 can be an added advantage in faster approval of a personal loan. This is the most important criteria that the lenders use to evaluate your profile, especially in a personal loan, because it is an unsecured loan that does not require any collateral. Therefore, your income and credit repayment history are the major factors considered while approving the loan. A low credit score indicates a high-risk profile, which means the possibility of you defaulting on the loan repayment in the future is higher.

Hence, if your personal loan application is rejected due to an insufficient credit score, you should immediately start working on improving it. To improve your credit score, you should pay your EMIs on time and never default on any loan or credit card dues. The best way is to set standing instructions with your bank for an auto-pay of all your EMIs and credit card repayments. It ensures your monthly repayments get paid automatically from your registered bank account on the due date. Ensure you always keep a sufficient balance in your auto-pay registered bank account so that your standing instruction does not bounce.

3. Complete your documentation and provide the correct details:

While submitting your loan application, the lender asks for a set of documents like your identity proof, address proof, income proof, etc. If any document from the lender's list is missing or does not match with their requirement, your loan application can get rejected. Moreover, the application can also get rejected if there is any discrepancy in the information you provided and your documents. The lender also performs a background check and may contact your employer.

If your personal loan application is rejected due to incomplete documentation, you can resubmit the required documents. However, if the lender thinks you have intentionally altered the documents, misrepresented the information, hid any details, or provided incorrect information, the lender can restrain you from reapplying with the

4. Work on your eligibility criteria:

If your loan application is rejected due to not fulfilling the lender's eligibility criteria, you can work on it if it is under your control.

Rejection due to insufficient income: Lenders have different income criteria that vary from lender to lender. If you do not meet the income criteria of a particular lender, you can apply with some other lender with a lower income requirement. However, if you do not meet the income criteria of any of your preferred lenders, it makes sense to wait until you increase your income up to the sufficient requirement.

Rejection due to frequent job changes: Many lenders do not prefer to lend money to individuals who are not stable at a job. If you frequently change the employers, the lender will consider you as a high-risk profile individual, which can result in loan rejection. Hence, it is advisable to reapply for a personal loan after spending a basic minimum turnover of 18 to 24 months with your current company.

Rejection due to the age criteria: Lenders have age criteria for the borrowers of all types of loans. If you do not fulfil it, your loan will be rejected. So, if you are not meeting the minimum age criteria, it makes sense to wait until you become eligible for the loan. However, offering personal loans to senior citizens could be riskier for the lenders, which is why they put a maximum age limit for borrowing. If you have passed the maximum age limit, you may try with other lenders or a secured loan that can have a higher maximum age limit.

Rejection due to high debt-to-income ratio: Lenders consider your debt-to-income ratio while approving/rejecting your personal loan application. A debt-to-income ratio is a ratio of your monthly EMIs and your monthly income. Having EMIs less than 30% of your monthly income is considered a good debt-to-income ratio. Higher the ratio, the higher the chances of loan application rejection. A higher ratio depicts your liabilities are more than your earnings. For example, if your monthly salary is Rs 50,000 and your existing EMIs cost Rs 30,000, your debt-to-income ratio is 60%. Lenders usually consider it risky if a ratio is more than 45%. If your application is rejected due to a high debt-to-income ratio, it is advisable to reconsider your loan requirement. Therefore, apply only in case of an emergency after you pay off some of your current debts.

To Conclude:

Availing of a personal loan is not as easy as it seems. We understand that a personal loan is usually an urgent requirement, but if your personal loan application is rejected, the points discussed in the article are worth following to ensure your next application does not get rejected. If you apply with the lender with whom your eligibility and requirement match the best, there are fewer chances of loan rejection. However, if you are in a financial emergency and need the funds at the earliest, you should consider other loan options like mortgage loan, loan against securities, gold loan, etc. that have lower interest rates, and unlike a personal loan, these can be availed with an average credit score.

Warm Regards,

Ketki Jadhav

Content Writer