Time to Redeem Your Investments in Banking & Financial Services Funds?

Listen to Time to Redeem Your Investments in Banking & Financial Services Funds?

00:00

00:00

Ample liquidity in the system and central banks across the world resorting to interest rate cuts as well as maintaining an accommodative stance to support growth is enabling in the stock markets to scale new highs.

Besides, the reduction in the number of new COVID-19 cases in India (compared to the peak of September) and vaccine in sight (with emergency authorisation approval sought by several players), and series of measures undertaken by the government to boost growth are proving to be tailwinds for the Indian equity markets.

However, with rising indices and expensive valuations, domestic fund managers seem to be finding themselves in a catch-22 situation and have become cautious. In November 2020, in every single trading session, domestic mutual funds remained net sellers. Cumulatively, they sold equities worth Rs 28,320 crore in November on a net basis. And interestingly, domestic mutual funds trimmed their exposure to some of the leading and index-heavy private sector lenders, such as Kotak Mahindra Bank, HDFC Bank, ICICI Bank, and Bajaj Finance to name a few.

On the other hand, Foreign Portfolio Investors (FPIs) remained bullish on India even in November 2020 with their net investments reaching to Rs 62,951 crore -the highest so far in any given month of the calendar year 2020. And you would be surprised to know that nearly 48% of these investments went into the Banking and Financial Services sector.

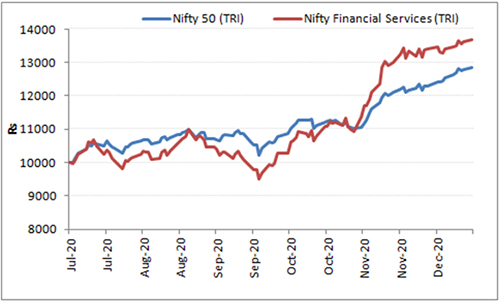

Graph: The financial services sector outshone the bellwether index

Base = Rs 10,000

Base = Rs 10,000

Data as of December 15, 2020

(Source: NSE, PersonalFN Research)

The Banking and Financial Services sector companies have outperformed the bellwether index ever since the moratorium period ended on August 31, 2020. The second-quarter results didn't reflect as much stress for the sector as what was anticipated by many experts at the beginning of the pandemic.

Given the rich valuations, profit booking could be one of the reasons behind fund managers selling the frontline financial stocks, but it's also due to the redemption pressure from investors. According to the monthly data released by the Association of Mutual Funds in India, equity-oriented mutual fund schemes across the board witnessed outflows aggregating to Rs 12,917 crore in November.

Many of you may have a question: Now that mutual funds have sold some leading Banking and Financial Services sector companies heavily, is this the right time to redeem your investments in these funds?

The Banking and Financial Services sector has a dominant representation in broader indices -close to 40% weight in the Nifty 50 Index and 34% in the Nifty 500 index. In the case of Banking and Financial Services Funds, the top-5 stocks carry 55%-60% exposure to this sector - which makes it a high-risk proposition.

Table: How have Banking and Financial Services Funds Fared?

Direct Plan and Growth Option considered.

Data as of December 15, 2020

(Source: ACE MF, PersonalFN Research)

Over the last six months, Banking and Financial Services Funds have done remarkably well as depicted by the table above. However, over 1-year period returns clocked by many funds are in the negative with some even having persistently underperformed the Nifty Financial Services Total Return Index (TRI).

Over longer time frames, i.e. 5 years and 7 years, barring SBI Banking & Financial Services Fund, Aditya Birla SL Banking & Financial Services Fund, ICICI Prudential Banking & Fin Service Fund, and Invesco India Financial Services Fund, the others have failed to generate alpha for investors. Given these conditions, you may consider redeeming investments from schemes that have failed to outperform the benchmark index.

Will Banking and Financial Sector Funds fare well in the future?

(Image source: rawpixel.com)

(Image source: rawpixel.com)

The results reported in the last few quarters suggest that leading private sector financial institutions have managed to maintain their asset quality, raise capital, keep slippages under check, and improved on earnings.

That said, any company-specific unforeseen development could prove catastrophic for the investors of such funds. If the tide turns against the Banking and Financial Services Fund, it would weigh on their performance.

An unforeseen rise in Non-Performing Assets (NPAs) amidst a heightened credit environment and a prolonged lull in the economy may work against Banking and Financial Service Funds. The Reserve Bank of India (RBI) has estimated that banking NPAs may rise to 12.5% by March 2021. In the last week of December, the RBI is expected to release the Financial Stability Report - the report will be crucial since it would comment on the likely NPA situation in the wake of the pandemic.

The data published by RBI for Q2FY21 suggests that credit growth has slipped further to 5.8% in Q2FY21 from 8.9% in the year-ago period. This is not very good for the banking sector in particular. Banks are considered to be a proxy of the overall economic growth of a nation.

Are you wondering how to accelerate the portfolio return if you were to avoid Banking and Financial Services Funds?

Well, there is a strategy for that, based on the 'Core & Satellite' approach to equity investing. It is one of the approaches some of the successful equity investors follow to build wealth -- and particularly useful when Indian equity markets are at their all-time high.

At PersonalFN, we have devised a 'Core and Satellite' approach to building a sound all-weather portfolio of some of the best equity mutual fund schemes strategically.

As per this strategy, a large-cap fund, multi-cap fund, and a value style fund amongst others should make up 65%-70% of your portfolio, which could be termed as 'Core holdings'. The term 'Core' applies to the more stable, long-term holdings of the portfolio.

The term 'Satellite' applies to the strategic portion that would help push up the overall returns of the portfolio, across market conditions. Plus, the 'Satellite' portfolio provides the opportunity to support the 'Core' by taking active calls based on extensive research. The 'Satellite' holdings may account for 30%-35% of your portfolio and comprise of a mid-cap fund, small-cap, and an aggressive hybrid fund.

Note that this allocation to the satellite portfolio should change based on the market outlook. If the outlook is extremely gloomy, you may avoid midcaps altogether and add more exposure to aggressive hybrid funds to add stability.

To build a 'Core & Satellite' portfolio of some of the best equity mutual fund schemes, here are some ground rules:

-

Consider funds that have a strong track record of at least 5 years and have been amongst the top performers in their respective categories

-

The schemes should be diversified across investment styles and fund management

-

Ensure that each selected scheme abides with its stated objectives, indicated asset allocation, and investment style

-

You should not only invest across investment styles (such as growth and value) but also across fund houses

-

The mutual fund schemes should be managed by experienced and competent fund managers and belong to fund houses that have well-defined investment systems and processes in place

-

Not more than five schemes managed by the same fund manager should be included in the portfolio

-

Not more than two schemes from the same fund house shall be included in the portfolio

-

Each scheme that is to be included in the portfolio should have seen an outperformance over at least three market cycles

-

You should restrict the count of mutual fund schemes in your portfolio to seven

And once the portfolio is created, monitor it regularly (bi-annually) rather than timing the market.

You see, a sensibly constructed "Core and Satellite" portfolio of equity mutual funds adduce the following benefits:

-

Facilities optimal diversification

-

Reduces the need to frequently churn the portfolio

-

Reduces the risk profile to your portfolio

-

Enables you to enjoy the benefits of a variety of investment strategies

-

Creates wealth cushioning the downside

-

Holds the potential to outperform the market

Happy Investing!

Warm Regards,

Rounaq Neroy

Editor, Daily Wealth Letter

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds