7 Reasons to Tactically Allocate More to Gold Now

Listen to 7 Reasons to Tactically Allocate More to Gold Now

00:00

00:00

Gold historically has been a worthy avenue in times of economic and financial stress thanks to its unique ability to be highly liquid, carries no credit risk, generate returns, acts as a safety reserve asset, and is scarce, preserving its value over time.

In India, gold benefits from diverse sources of demand: as an investment, a reserve asset, an adornment, and a technology component. In terms of gold jewellery demand globally, India is the second highest consumer in the world.

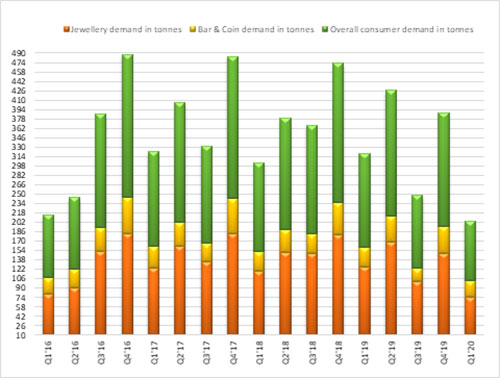

But the onset and scale of the COVID-19 pandemic has caused unprecedented disruption to the gold supply chain and affected the jewellery demand consumption and the overall consumption demand as seen below.

Graph 1: Fall in Demand

(Source: World gold Council)

Lockdown due to the coronavirus kept people away on the auspicious muhurats of Gudi Padva and Akshay Tritiya, followed by the wedding season from March onwards. As there were no takers of physical gold due to the retail line disruption, demand for physical gold dropped.

But despite lackluster demand in physical gold, it still inched up the indices. Total Q1 demand grew marginally to 1,083.8t (+1% y-o-y) globally, as per the World Gold Council data.

Let's look at the factors that have been favourable for gold...

-

Pandemic wildfire:

Over the last couple of months, the aftereffects of this pandemic on the global trade, global economy, and global growth prospects have been devastating; the equity markets have caught the flu and are currently panting for a positive breather. So far the extreme volatility in equities has eroded the wealth of investors . The coronavirus outbreak, which swept the globe during the first quarter, was the single biggest factor influencing gold demand.

-

Debt Markets were contaminated due to credit default ripples

Investors with moderate to low risk-takers had invested in debt markets through mutual funds with low-grade papers and ratings, which led to the biggest liquidity crisis. In fact, fund houses, including investors, have burnt their fingers when the redemption pressure increased due to lockdown induced job losses and deferred salaries.

(Image source: Image by 3D Animation Production Company from Pixabay)

-

Rupee depreciation against the dollar

The Q1 average price of Rs 41,124/10g in Q1 was 26.6% higher y-o-y. The local gold price continued its upward trajectory in Q1 2020 and breached previous historical highs. A weaker rupee combined with a rising dollar gold price resulted in the local gold price closing at an all-time high of Rs 44,315/10g in March in the spot market, which was unavailable later. In the futures market (on MCX), gold continued to display its lustre; the price per 10 gram of gold scaled over Rs 46,500.

-

Monetary policy measures

Persistently low-interest rates has reduced the opportunity-cost of holding gold and highlights its attributes as a source of genuine, long-term returns, particularly when compared to historically high levels of global nega-yielding debt. The central banks across the world reduced interest rates and kept their monetary policy stance accommodative to support growth.

-

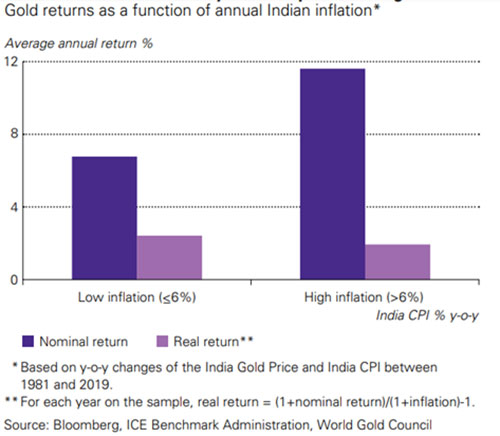

To beat inflation and combat deflation

Fact is Gold is a hedge against inflation. The average annual return of 10% since 1981 has outpaced the Indian consumer price index (CPI). Gold also protects investors against extreme inflation. In years when Indian inflation was higher than 6%, gold's price increased 11.5% on average. Over the long-term, therefore, gold has not just preserved its investors' capital, but helped it grow.

Graph 2: Returns during inflationary pressure

(Source: World gold council)

-

Continued Geopolitical uncertainty

Tensions between the US and China continue to escalate. Brewing trade war tensions due to protectionist policies followed between the US and other countries. Plus, China and India border tensions are on the rise; as well as the pandemonium of US Presidential elections coming up in November 2020.

-

Concerns around economic growth

A record-high global debt-to-GDP of nearly US$ 255 trillion (over 322% of global GDP) - 40 percentage points higher than at the onset of the 2008 global financial crisis according to the Institute of International Finance (IIF), as the world is fighting the COVID-19 pandemic.

India's GDP growth has been on a downward trajectory since Q1 2019 and green shoots of recovery were sparse in Q1. Against such a backdrop, consumer spending on non-essential items declined.

India's GDP growth rate reading for Q4FY20 has plunged to 3.1%. This reading is 100 basis points higher than the market forecast of 2.1%, yet the lowest since the fourth quarter of FY09 -- plus ever since the quarterly data became available in the year 2004. Thus GDP growth during 2019-20 is estimated at 4.2% versus 6.1% in 2018-19.

Gold's versatility is the driving force

Since gold as an asset has a negative correlation with other assets during risk-off periods, protecting the investors' capital against tail risks and other events that have an adverse impact on capital or wealth. When economic conditions are benign, there is slow consumer growth and inflationary pressure, it works in gold's favour.

During these times, however, market participants try to safeguard their capital against extreme losses and choose assets like gold. This increases gold investment demand and drives up the gold prices. Hence, it is one of the most sought-after safe havens.

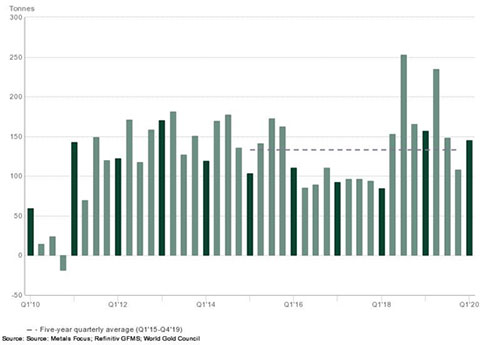

Central banks understand the significant role of gold asset class. Central bank reserves are constructed on three guiding principles: safety, liquidity, and return. The COVID-19 pandemic has reinforced the significance of these principles and, by extension, the importance of smart and sustainable reserve management.

Hence there has been a surge of interest in gold among central banks across the world as foreign reserves for safety and diversification. Thus global gold reserves grew by 145t in Q1, but 8% lower than Q1 2019, but stayed in line with longer-term average levels. Six central banks made net purchases of a tonne or more, compared to the same period last year.

Graph 3: Global gold reserves growth

(Source: World Gold Council)

Taking cognizance of the above data, in many parts of the world gold ETFs witnessed huge inflows in May 2020. As exhibited by the table below, North American and European Funds drove the inflows. Globally, gold ETFs added 154t (net inflows of US$ 8.5bn or +4.3%) in May 2020, boosting holdings to a new all-time high of 3,510t.

Table: How did the world approach Gold ETFs in May 2020?

| Region |

Total AUM (bn) |

Holdings (tonnes) |

Flows (US$mn) |

Flows(% AUM) |

| North America |

100.9 |

1,815.3 |

20,316.9 |

20.1% |

| Europe |

85.4 |

1537.3 |

11,620.6 |

13.6% |

| Asia |

5.6 |

100.9 |

1,138.8 |

20.3% |

| Other |

3.1 |

56.6 |

638.6 |

20.3% |

| Total |

195.1 |

3510.1 |

33,714.8 |

17.3% |

Data as of May 31, 2020

(Source: World Gold Council)

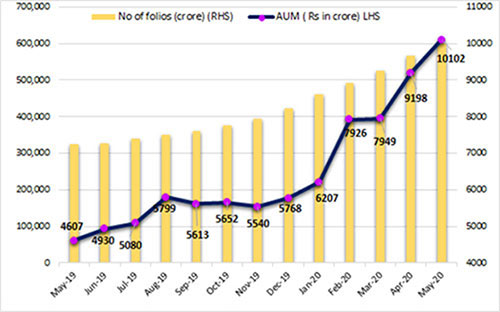

Hence smart investors continued to take refuge under gold, recognising its trait of being a safe haven, a store of value in times when the world is staring at economic uncertainty (caused by the COVID-19 pandemic) and fear of a global recession looms large -- probably worse than the Global Financial Crisis of 2008. In India, the AUM of gold ETFs continued to witness a rise and so did the folio (see Graph 15).

Graph 4: Smart investors buying Gold ETFs

Data as of May 2020

(Source: AMFI, PersonalFN Research)

Road Ahead

Even the World Gold Council (WGC) expects the market risk and economic growth interaction to impact gold prices this year. Mainly, the following factors will keep the focus on gold as per the WGC:

The uncertainty brought about by the novel Coronavirus and its potential impact on public safety and economic growth could be added to the list, says WGC.

In January the WGC estimated demand between 700 and 800 tons in 2020. But in the latest quarterly update, the WGC stated it would be unable to quantify the impact of the virus on Indian demand in its latest update.

Only when normalcy returns in later months (after COVID-19 is successfully contained) and the southwest monsoon is normal, people will buy gold. Until then, demand for gold is likely to remain downbeat.

As per the WGC Outlook 2020, while gold price volatility and expectations of weaker economic activity may result in softer consumer demand in the near term, structural economic reforms in India and China will support demand in the long-term.

What should investors do?

Gold's traditional role as a safe-haven asset means it can demonstrate its qualities during times of high risk. In addition, gold's dual appeal as an investment and a consumer good means it can generate positive returns in good times too.

This dynamic is likely to persist, reflecting persistent political and economic uncertainty, persistently low interest rates and economic concerns surrounding stock and bond markets.

Investing in gold in paper form can prove to be more effective. Avoid a speculative approach while investing in gold. Look at it as a portfolio diversifier and a monetary asset (rather than a mere commodity), which can help you reduce the risk to your overall portfolio. Ideally, invest in gold with a longer investment horizon.

Equity and debt markets are yet to see any signs of revival despite the stimulating relief measures provided to alleviate the economy's slowdown, but investing in gold can prove to be worthwhile in creating wealth.

[Read: What Could Be the Potential Impact of a Lockdown on Your Mutual Fund Portfolio? Know Here...]

Bond prices were at all-time lows, which are inversely proportional to gold as well. In my view, allocate at least 10-15% of your entire investment portfolio to gold and hold it with a long-term investment horizon. Invest in gold the smart way through gold Exchange Traded Funds (ETFs) or gold savings funds.

Remember gold offers an effective hedge during global uncertainty and a shield against inflation. Most importantly in your portfolio, it serves as a diversifier.

Warm Regards,

Aditi Murkute

Senior Writer

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds