Will Interest Rates in India Fall Soon? Know Here

Rounaq Neroy

Apr 18, 2024 / Reading Time: Approx 9 mins

Listen to Will Interest Rates in India Fall Soon? Know Here

00:00

00:00

Interest rates in India have remained elevated for quite some time now (since April 2023). The risk-averse investors, particularly senior citizens, who rely on fixed-income instruments, viz. Bank Fixed Deposits (FDs) and Small Saving Schemes (SSS), have reaped the rewards of a high interest rate regime.

But the question arises: For How Long Will Interest Rates in India Remain High?

At some point in time, the Reserve Bank of India (RBI) would want to cut rates (whereby borrowing cost also reduces) to support growth.

That said, currently there are some challenges in play. These are...

Intensified Geopolitical Tensions - The recent Iran-Israel conflict, the war in Gaza with Hamas, the potential build-up of this in other parts of the Middle East (such as Lebanon, Iraq, Yemen, and Syria), attacks on ships in the Red Sea, the ongoing Russia-Ukraine war, brewing tensions in the Korean Peninsula, China conducting joint military activity with the U.S., Japan, and Philippines -- named 'Military Cooperative Activity' -- in South China Sea (a disputed area where China claims territorial sovereignty), and scruffles between China and India at borders are some of geopolitical events that are keeping policymakers on the alert.

The spillover from these geopolitical hostilities inflicts the risk of geoeconomic fragmentation, supply chain disruptions -- causing uncertainty in commodity prices (particularly food and fuel) - increasing volatility in the financial markets and weighing on global GDP growth and inflation, observes the RBI.

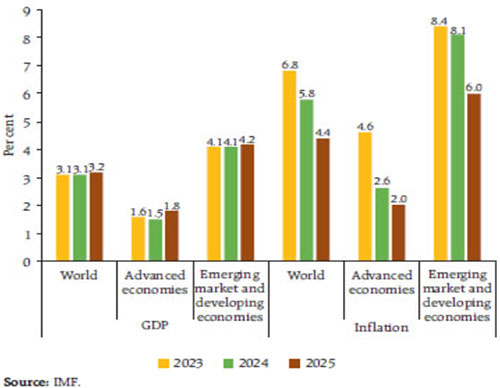

Graph 1: Global GDP and Inflation Growth

(Source: RBI Monetary Policy Report, April 2024)

(Source: RBI Monetary Policy Report, April 2024)

Global GDP growth is expected to trail its historical (2000-19) average of 3.8% owing to various headwinds. Inflation in the Emerging Market Economies (EMEs) such as India is expected to remain higher than in the Advanced Economies (AEs). In other words, AEs would see faster disinflation.

Crude Oil May Boil - The simmering geopolitical tension, particularly in the Middle East (a major oil producer), could cause an international oil price surge. If tensions continue, Brent crude oil, which is already at a 6-month high, would cross USD 100 per barrel. OPEC has already extended voluntary production cuts of 2.2 million barrels per day. Currently, OPEC is producing nearly 30 million barrels of crude oil per day.

For India, which is one of the largest oil importers, the surge in crude oil would not bode well, as it means a wider trade account, current account deficit, and fiscal deficit (in other words, a triple deficit).

Adverse Climate Events and Impact on Agriculture - Global temperatures are on the rise and there are extreme weather events impacting society and the economy.

The frequency and ferocity of weather shocks are increasing and posing challenges for monetary policy, as per the RBI. Currently, several parts of the country are experiencing heatwaves, triggering water scarcity, potential power cuts, and upside risk to food inflation (particularly vegetables and fruits). Food comprises a weight of 46% on the CPI inflation basket. In such a scenario, the agriculture and FMCG sectors would most be affected, and consequentially, rural demand would take a hit.

According to the Indian Meteorological Department (IMD), the southwest monsoon this year is expected to be above-normal (106% of the Long Period Average of 87 cm, with a model error of (+/-) 5.0%), but the favourable La Nina weather conditions are expected only somewhere around August and September. Note, that the Kharif crop sowing is usually done in June and July. Until then, the extreme heat from April to June could prove damaging for crops and impact supplies.

Interruptions to the Disinflation Process - CPI Inflation is one of the key deciding factors for the policy interest rates. While CPI inflation in India has witnessed decent disinflation in the recent few months and is at a 10-month low of 4.85% for March 2024, even now, CPI inflation is above RBI's medium-term target of 4.0%.

The RBI in its recently held April 3-5, 2024, bi-monthly monetary policy statement for 2024-25, envisages that the following factors could weigh up on the inflation outlook:

- Food price uncertainties

- Unpredictable supply-side shocks

- Increasing incidence of climate shocks

- Lower reservoir levels, especially in the southern states and expected above-normal temperatures during April to June 2024

- Cost-push pressures faced by firms

- Firming up of international crude oil prices

- Geopolitical tensions and volatility in the financial markets

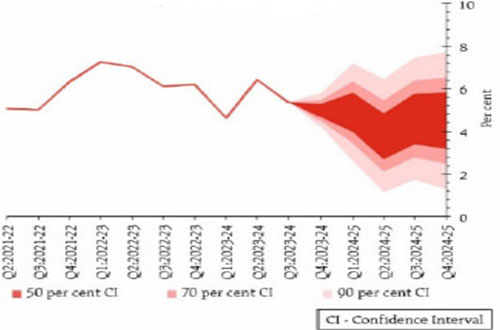

Graph 2: RBI's Quarterly Projection of CPI Inflation

(Source: RBI Monetary Policy Statement 2024-25, April 3 to 5, 2024)

(Source: RBI Monetary Policy Statement 2024-25, April 3 to 5, 2024)

Taking the aforementioned factors into consideration and expecting a normal monsoon, the RBI has projected CPI inflation for 2024-25 at 4.5% -- with Q1 at 4.9%; Q2 at 3.8%; Q3 at 4.6%; and Q4 at 4.5% -- with the risks are evenly balanced.

In other words, there are several upside risks to the path to inflation trajectory.

So, where are interest rates headed?

The path to interest rates is hinged on the path to inflation trajectory.

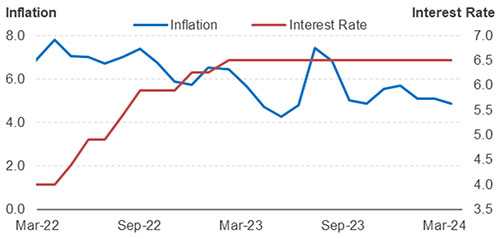

Graph 3: CPI v/s. Interest Rates

Data as of April 12, 2024

Data as of April 12, 2024

(Source: RBI, MOSPI, data collated by PersonalFN Research)

Currently, the robust growth prospects for India provide policy space for the RBI to remain focused on inflation. Therefore, the six-member MPC in the April 2024 monetary policy has decided to continue to be actively disinflationary to ensure the anchoring of inflation expectations and fuller transmission.

The MPC remains resolute in its commitment to aligning inflation to the target. The MPC believes that durable price stability would set strong foundations for a period of high growth. The MPC is also focused on the withdrawal of accommodation to ensure that inflation progressively aligns with the target while supporting growth.

To me, it appears that we are almost near the peak of the interest rate upcycle. The RBI now only wants to see a sustained decline in CPI inflation and return to the target of 4.0% before reducing the policy repo rate.

What Should Be Your Investment Strategy to Invest in Fixed-income Instruments and Debt Mutual Funds Now?

If you are a risk-averse investor or, in general, looking to keep money safe in fixed-income instruments such as Bank FDs and/or suitable small saving schemes, this is an opportune time to invest at a high interest rate.

To invest in Debt Mutual Funds now is the time to take exposure to the longer end of the maturity curve. Medium-to-long duration Debt Funds would be a meaningful choice for a 3 to 5-year investment horizon whereby you benefit from higher yield and unlock the capital growth.

For an investment horizon of 2 to 3 years or so, you could consider some of the best Banking & PSU Debt Funds, Corporate Bond Funds, or in case you wish to take slightly high risk and play the interest rate cycle, then Dynamic Bond Funds.

If your investment horizon is up to or less than a year, it would be better to stick to the best Liquid Funds and/or Overnight Funds that have no exposure to private issuers. Funds that invest in the short maturity segment witness minimal mark-to-market impact when interest rates fall.

[Read: Best Debt Mutual Fund Categories for 2024]

As interest rates in the economy descend in time to come, returns of debt funds would get attractive. This is on account of the positive correlation between interest rates and yields, while an inverse correlation between yield and bond prices.

[Read: Here Is Why Your Fixed Income Portfolio Is Likely to Perform Better]

The returns on Debt Mutual Funds could get better than some of the traditional fixed-income instruments, but please note that they may be subject to credit risk, interest rate risk, reinvestment risk, and liquidity risk among others.

Hence, make sure to choose Debt Mutual Funds prudently. Considering the credit quality of the underlying securities in the portfolio, their rating profile, the average maturity profile, risk ratios, the returns across time periods, performance across interest rate cycles, plus the investment processes and systems followed at the fund house to choose among the best Debt Mutual Funds.

Other than that, consider their personal risk appetite and liquidity needs to make suitable choices.

If you need guidance to select suitable mutual fund schemes, don't hesitate to reach out to a SEBI-registered investment advisor who can back the recommendations with thorough research as per your investment needs.

Happy Investing!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.