ROUNAQ NEROY DEC 20, 2023 / READING TIME: APPROX. 15 MINS

India is a "bright spot" in the global economy and a key contributor to global growth, backed by reforms (as observed by the IMF). Recognising the long-term growth prospects, the investment flows into India continue to remain strong.

Having said that, considering 2024 will be an election year, geopolitical tensions are looming, equity markets are at an all-time high (valuations appear stretched), and there are chances of super El Nino weather conditions next year, it would be meaningful to take a short-term view (of 3 years or so) and invest suitably portion of your portion in certain sub-categories of debt mutual funds that are less risky.

"Be fearful when others are greedy, and greedy when others are fearful." - Warren Buffett.

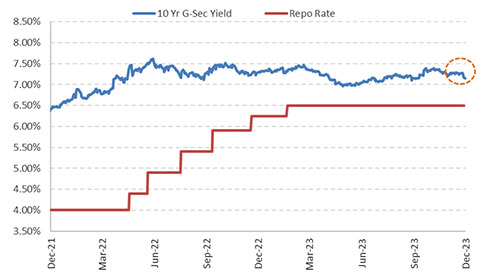

Ever since the U.S. Federal signalled that policy interest rates may be cut next year, the 10-year G-sec yield has softened a bit.

Graph 1: 10-year G-sec Yield Curve

Data as of December 18, 2023

Data as of December 18, 2023

(Source: Investing.com, data collated by PersonalFN Research)

Since April this year, the benchmark 10-year yield is down by 16 basis points (bps) as of December 18, 2023. As you may be aware, interest rates and yields have a positive correlation to one another.

Currently, interest rates are elevated in most developed and developing economies. In the fight to curb inflation, central banks may keep interest rates for longer, observes the IMF. The World Bank President, Ajay Bagga, has opined that interest rates staying higher for longer -- which he believes they will -- could complicate investment across the world.

The path to interest rates is hinged on the inflation trajectory. If the inflation CPI reading moderates, central banks, including the RBI, may be nudged to lower the policy interest rates. And as a result, the benchmark G-sec yield would soften further.

Currently, the following sub-categories of debt mutual funds would be appropriate choices:

-

Liquid Funds- For an investment time horizon of a couple of months to a year, Liquid Funds can be an ideal choice.

Liquid Funds are open-ended debt mutual funds that primarily invest in short-term money market instruments with a maturity of up to 91 days.

Typically, Liquid Funds invest in money market instruments such as Certificate of Deposits (CDs), Commercial Papers (CPs), Term Deposits, Call Money, Treasury Bills, and so on.

Given the type of securities Liquid Funds hold, usually they entail low risk. They usually prioritise safety and liquidity over return.

The interest rate and credit risk are relatively low compared to the other sub-categories of debt funds.

The investment objective of a Liquid Fund is capital preservation and ensuring liquidity through judicious investments in the money market and debt instruments. It benchmarks its performance against the Crisil Liquid Debt Index and/or Crisil 1-year T-bill Index.

But keep in mind there is some element of risk. It cannot be assumed that Liquid Funds are absolutely risk-free. If a Liquid Fund invests in debt papers of private issuers and compromises on quality to generate slightly better returns, the risk could be elevated. Ideally, a Liquid Fund should not engage in yield hunting to generate higher returns.

Hence, you need to be careful when selecting Liquid Funds. Don't just consider the past or historical returns as they are in no way indicative of future performance. Likewise, avoid going by shallow mutual fund star ratings that give emphasis only to quantitative aspects. Instead, pay attention to portfolio characteristics, the investment ideologies at the fund house, the risk mitigation framework, and a host of other qualitative and quantitative aspects.

Want to know the three best Liquid Funds for 2024? Watch this video:

[Read: 3 Best Liquid Funds for 2024]

If you add the best Liquid Funds to your debt portfolio, it may help keep your money safe and address contingency needs. Liquid Funds are a worthwhile option over and above having money in a savings bank account.

Note, that even Buffett, a legendary investor, tactically allocates a portion of his portfolio to short-term US treasuries. In your case, you could follow this strategy by investing in a Liquid Fund.

-

Banking & PSU Debt Funds - If you are looking at an alternative to park your money into a bank fixed deposit and have an investment time horizon of 2 to 3 years, then some of the best Banking & PSU Debt Funds may be a meaningful choice.

Banking & PSU Debt Funds are mandated to invest predominantly (80% of their assets) in top-rated corporate debt instruments issued by Banks, Public Sector Undertaking (PSUs), Public Financial Institutions (PFIs), Municipal bonds, and other such securities. These entities are recognised for their robust credibility and liquidity compared to those from private issuers, making them a relatively safer investment option.

As far as the maturity profile of the debt papers is concerned, Banking & PSU Debt Funds have the flexibility to diversify their exposure across the yield curve. So, there isn't any fixed limit for the portfolio duration.

That being said, a majority of Banking & PSU Debt Funds maintain a duration of 2 to 5 years in their portfolio. The decision is based on the evaluation of various micro and macroeconomic factors, including the interest rate cycle.

The higher duration or maturity profile of the securities held in the portfolio makes Banking & PSU Debt Funds susceptible to interest rates, particularly in an uncertain and rising interest rate environment.

Broadly, the primary investment objective of Banking & PSU Debt Funds is to generate reasonable returns broadly in line with the aforesaid debt and money market securities by maintaining an optimal balance of yield, safety, and liquidity. However, there is no assurance that the investment objective will be realised.

To make the best choice among a plethora of Banking & PSU Debt Funds available, you must pay close attention to portfolio characteristics (who the issuers are, the sector they belong to, the type of debt papers held, the ratings of the respective debt papers, the average maturity, Yield-To-Maturity, and the Modified Duration, etc.), the performance across interest rate cycles, whether the fund is justifying the risk taken (by considering the Standard Deviation, Sharpe Ratio, Sortino Ratio, etc.), the fund management credential, the systems and processes followed at the fund house, ideologies and risk management measures - and not just look at the historical returns or shallow mutual fund star ratings. Keep in mind that mutual fund star ratings aren't foolproof.

Want to know the three best Banking & PSU Debt Funds for 2024? Watch this video:

[Read: 3 Best Banking & PSU Debt Funds for 2024]

By adding some of the best Banking & PSU Debt Funds, you could potentially earn competitive market-linked returns over an investment horizon of 2 to 3 years.

-

Corporate Bond Funds - If you wish to benefit by investing in quality corporate bonds and have an investment time horizon of around 3 years, some of the best Corporate Bond Funds make sense.

They are mandated to invest a minimum of 80% of their assets in the highest-rated corporate bond instruments (AA+ and above rate corporate bonds), alongside debt securities issued by central and state governments and money market instruments.

There is no limit or restriction on the maturity profile of corporate bonds, but typically, they are in the range of 2 to 3 years. The fund manager of a Corporate Bond Fund considers a host of macroeconomic factors, particularly interest rates and yields, for the portfolio duration.

Corporate Bond Funds have moderate sensitivity to interest rate changes. An uncertain and rising interest rate scenario could make them vulnerable to fluctuations. But when interest rates are stable or falling, they stand to potentially benefit.

The broader investment objective of Corporate Bond Funds is to generate optimal returns with high liquidity through active management of the portfolio by investing in high-quality debt securities and money market instruments. However, there is no assurance or guarantee that the investment objective will be realised.

Note, that the performance of Corporate Bond Funds is influenced by the credibility of the issuers they hold in the portfolio, the maturity of their portfolio holdings, and the interest rate movement.

It is worthwhile to go with Corporate Bond Funds that do not engage in yield hunting and jeopardise the liquidity of the portfolio to generate higher returns.

Hence, it becomes important to look at the portfolio characteristics, the risk the fund is exposing its investors to (as denoted by the Standard Deviation), the risk-adjusted returns (as denoted by the Shape Ratio, Soritno Ratio, etc.), and the investment ideologies, processes, and systems at the fund house rather than just past returns and star ratings. The future of the scheme hinges on the quality of the underlying assets or securities a fund holds.

Want to know which are the best Corporate Bond Funds? Read my article: 3 Best Corporate Bond Funds for 2024

-

Dynamic Bond Funds - To play the interest rate cycle with the expertise of a debt fund manager, some of the best Dynamic Bond Funds are meaningful, provided you have an investment time horizon of 3 to 5 years.

Regardless of the direction in which interest rates move, Dynamic Bond Funds are capable of taking advantage of dynamic market conditions and can invest accordingly to create an all-season portfolio that generates optimal returns.

As per the SEBI guidelines, invest across the duration of debt securities. They have the flexibility to shift investments between short-term, medium-term, and long-term debt securities, taking into consideration the interest rate cycle.

If the fund manager of a Dynamic Bond Fund is anticipating interest rates to fall, wherein locking in at higher interest rates is beneficial, higher allocation may be made to longer-duration debt securities. Conversely, in a rising interest rate, the fund manager may allocate more to short or low-duration securities.

Thus, Dynamic Bond Funds take a view of the interest rate cycle and bond yields to actively manage its portfolio.

Typically, money is invested in short-term instruments, such as Commercial Papers (CPs) and Certificates of Deposits (CDs), or medium to long-term instruments, such as corporate bonds and gilt securities.

Broadly, the primary investment objective is to provide optimal returns with high liquidity through an actively managed portfolio of high-quality debt securities across varying maturities (short-term and long-term) and money market instruments. However, there is no assurance or guarantee that the investment objective will be realised.

The performance of Dynamic Bond Funds largely depends on the fund manager's judgement of the interest rate movement. If the manager fails to gauge the movement of interest rates accurately or is unable to time the investment precisely, investors may suffer losses.

The level of risk depends on the kind of underlying securities held in the portfolio. If the fund manager of a Dynamic Bond Fund invests in low-quality debt papers to engage in yield hunting, it may expose its investors to high risk.

Avoid Dynamic Bond Funds that have high credit risk -- engaging in yield hunting to generate better returns -- but, in turn, imperilling the liquidity of the portfolio. Hence, apart from the quantitative parameters (i.e. past returns), also consider the qualitative aspects such as the portfolio characteristics, risk ratios, investment processes & systems, risk management framework, and ideologies followed by the fund house.

It is critical to invest in Dynamic Bond Funds that hold a robust portfolio of securities across maturities and high-quality debt & money market instruments.

Want to know which are the best Dynamic Bond Funds for 2024? Read my article: 3 Best Dynamic Bond Funds for 2024.

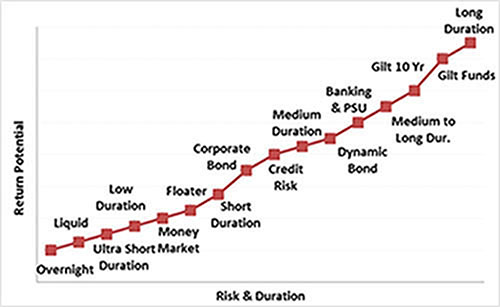

Graph 2: Risk-Return Spectrum of Debt Mutual Funds

For illustration purposes only

For illustration purposes only

(Source: PersonalFN Research)

You see, every sub-category of debt mutual funds occupies a distinctive space on the risk-returns spectrum (as seen in Graph 2). As an investor, you need to choose the one that considers your personal risk appetite and investment time horizon.

Debt-oriented Mutual Funds as they are less volatile than equities and facilitate steady growth of capital. Debt as an asset class plays an important role in one's portfolio. Although you may be a risk-taker or an aggressive investor, it makes sense to allocate a small suitable portion to debt instruments from a portfolio diversification standpoint (as it provides stability and liquidity). But keep in mind investment in debt funds is not 100% risk-free or safe (as in the case of an FD with a robust bank). There have been instances in the past where even the safest categories have incurred heavy losses due to negative credit surprises.

To know how much to allocate to debt and align the investments with your envisioned financial goals, speak to your SEBI-registered investment advisor.

Whichever sub-category of debt mutual funds you choose, be mindful of the tax implications. Watch this video to learn the tax rules for debt mutual funds:

With effect from April 1, 2023, the capital gain arising at the time of redemption -- whether short-term (a holding period of less than 36 months) or long-term (a holding period of 36 months and above) -- is also taxed as per investors' tax slab. The indexation benefit that earlier helped to make the most of the inflation impact on the purchase value of the investment and effectively reduced the LTCG tax liability is now no longer available for Debt Mutual Funds.

[Read: Debt Mutual Funds are Now at Par with Fixed Deposits for Taxation]

For NRIs, the capital gains on debt-oriented mutual funds are subject to Tax Deduction at Source (TDS) at the rate of 20% for LTCG and 30% for STCG.

If you have opted for the dividend option (now known as IDCW option), for resident Indians, any dividends from Corporate Bond Funds (under the Dividend Option) are added to the investors' total income and are taxed according to your income-tax slab, i.e., at the marginal rate of taxation. However, if the dividend amount is more than Rs 5,000, Tax Deduction at Source (TDS) will be first done at the rate of 10%. For NRIs, the dividend received is taxed at the rate of 20%.

Should you start SIP in debt mutual funds?

A Systematic Investment Plan (SIP) makes sense only if the investment time horizon is longer and depends on the sub-category of the Debt Mutual Fund one chooses to invest in. However, by and large, do note that the SIP returns in debt funds could be muted (in contrast to equity mutual funds). In other words, the rupee-cost advantage does not necessarily work to your, the investor's best advantage in case the NAV of the Debt Mutual Fund does not move up or down much.

[Read: Does it Make Sense to SIP in Debt Mutual Funds?]

Be a thoughtful investor.

Happy Investing!

Note: This write-up is for information purposes and does not constitute any kind of investment advice or a recommendation to Buy / Hold / Sell a fund. Mutual Fund Investments are subject to market risks, read all scheme-related documents carefully before investing.

We are on Telegram! Join thousands of like-minded investors and our editors right now.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.