3 Best Medium to Long Duration Debt Funds for 2025

Rounaq Neroy

Nov 27, 2024 / Reading Time: Approx. 25 mins

Listen to 3 Best Medium to Long Duration Debt Funds for 2025

00:00

00:00

In the last bi-monthly monetary policy meeting held on October 9, 2024 (before the CPI inflation data for October 2024 was released), the RBI maintained a status quo on the policy repo rate for the tenth time in a row.

Five members out of the six-member Monetary Policy Committee (MPC), namely Shri Saugata Bhattacharya, Prof. Ram Singh, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to keep the policy repo rate unchanged at 6.50%, whereas Dr. Nagesh Kumar voted to reduce the policy repo rate by 25 basis points in the monetary policy meeting held in October 2024.

A majority decided so considering the risks stemming from uncertainties relating to the escalating global geopolitical scenario, financial market volatility, adverse weather events and the recent uptick in global food and metal prices.

However, all the members of the MPC unanimously voted in favour of a change in stance from 'withdrawal of accommodation' to 'neutral' and decided to remain unambiguously focused on a durable alignment of inflation with the target, while supporting growth.

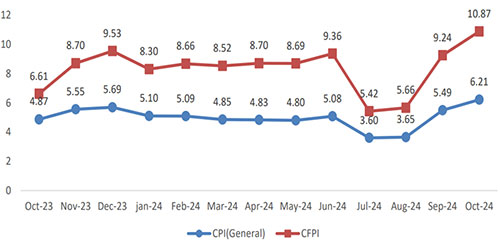

Consequently, when the CPI inflation data for October 2024 was released on November 12, 2024, the reading was at 6.21% (a 14-month high) from 5.49% in the previous month. It exceeded the RBI's target range of 2-6% for CPI inflation.

Graph 1: All India Inflation Trends Based on CPI and CFPI

Data as of October 2024.

Data as of October 2024.

(Source: MOSPI)

Higher CPI inflation was mainly due to higher food prices, which have nearly a 46% weight in the CPI inflation basket.

Even inflation in the fuel & light segment somewhat increased to 5.45% in October 2024 from 5.39% in the previous month.

Thus, the core inflation -- which excludes food and fuel -- also rose to a 10-month high of 3.70% in October 2024 compared to 3.50% in the previous month.

Even housing, which is a primary need, reported higher inflation in October 2024 than in the previous month.

The RBI is of the view that the progress on disinflation is still incomplete. The risks stem from uncertainties relating to heightened global geo-political risks, financial market volatility, adverse weather events and the recent uptick in global food and metal prices. Hence, the MPC has to remain vigilant of the evolving inflation outlook.

In the minutes of the last bi-monthly monetary policy, RBI Governor, Shaktikanta Das, writes:

At this stage of the economic cycle, having come so far, we cannot risk another bout of inflation. The best approach now would be to remain flexible and wait for more evidence of inflation aligning durably with the target. Monetary policy can support sustainable growth only by maintaining price stability.

So, where are Policy Interest Rates Headed?

Well, the path to interest rates is hinged on the inflation trajectory.

Currently, a resilient domestic growth outlook supported by investments and private consumption provides some headroom to the monetary policy to focus on the goal of attaining a durable alignment of inflation with the target.

The MPC has reiterated that enduring price stability strengthens the foundations of a sustained period of high growth.

The MPC is resolute in its commitment to aligning inflation to the 4.00% target within a band of +/- 2% on a durable basis while supporting growth.

Table 1: RBI Monetary Policy Action Since the Summer of 2022

| Month |

Repo Policy Rate |

Policy Action (Basis points) |

Monetary Policy Stance |

| Feb-19 |

6.25% |

-25 |

Neutral |

| Apr-19 |

6.00% |

-25 |

Neutral |

| Jun-19 |

5.75% |

-25 |

Accommodative |

| Aug-19 |

5.40% |

-35 |

Accommodative |

| Oct-19 |

5.15% |

-25 |

Accommodative |

| Dec-19 to Feb 20 |

5.15% |

Status quo |

Accommodative |

| Mar-2020 (an exceptional off-cycle meeting) |

4.40% |

-75 |

Accommodative |

| May-2020 (2nd exceptional off-cycle meeting) |

4.00% |

-40 |

Accommodative |

| Aug-20 to Apr-22 |

4.00% |

Status quo |

Accommodative |

| May-2022 (Off-cycle meeting) |

4.40% |

40 |

Accommodative |

| Jun-22 |

4.90% |

50 |

Focus on withdrawal of Accommodative stance |

| Aug-22 |

5.40% |

50 |

Focus on withdrawal of Accommodative stance |

| Sep-22 |

5.90% |

50 |

Focus on withdrawal of Accommodative stance |

| Dec-22 |

6.25% |

35 |

Focus on withdrawal of Accommodative stance |

| Feb-23 |

6.50% |

25 |

Focus on withdrawal of Accommodative stance |

| Apr-23 to Aug-24 |

6.50% |

Status quo |

Focus on withdrawal of Accommodative stance |

| Oct-24 |

6.50% |

Status quo |

Neutral |

Data as of November 25, 2024

(Source: RBI Monetary Policy Statements)

As seen in the table above, the RBI increased policy rates by 250 basis points (bps) from May 2022 to February 2023 to tackle CPI inflation. Since April 2023, the policy rates have remained unchanged with moderation seen in inflation.

While the change in stance to 'neutral' provides flexibility to the MPC to handle inflation risk, overall it seems that interest rates in the Indian economy have almost peaked.

[Read: Why Senior Citizens Should Consider Investing in Bank FDs Now]

In the December 2024 bi-monthly monetary policy statement 2024-25, it looks unlikely that the RBI would cut the policy repo rate in a hurry.

If CPI inflation comes down, perhaps the February 2025 bi-monthly monetary policy the RBI may cut the policy rates or may even give it a miss and consider cutting rates in the fiscal year 2025-26.

Among the major central banks, the U.S. Federal Reserve, the European Central Bank (ECB), and the Bank of England (BOE), abetted by inflation data of their economies, have already begun cutting rates.

At the current juncture, it would be an opportune time to invest in medium-to-long duration debt mutual funds, wherein you benefit from high yields and unlock capital growth. This is on account of the inverse relation between bond prices and yield.

Note, that since the October 2024 bi-monthly monetary policy statement, the 10-year benchmark G-sec yield has spiked and has remained elevated. Watch this video:

The fact also is the rise in the 10-year U.S. Treasury yield is causing the spike in the government of India's 10-year G-Sec yield.

You could capitalise on the spike in bond yields and sensibly take exposure to Medium-to-Long Duration Debt Funds now.

What are Medium-to-Long Duration Debt Funds?

Medium-to-Long Duration Debt Funds, as characterised by the regulator, invest in debt and money market instruments such that the Macaulay Duration of the portfolio is between 4 to 7 years.

The Macaulay Duration, named after Frederick Macaulay, is the weighted average term-to-maturity of the cash flows from a bond. The weight of each cash flow is determined by dividing the present value of the cash flow by the price.

Macaulay Duration provides an estimate of the volatility or sensitivity of the market value of a bond or portfolio of bonds to changes in interest rates.

Keep in mind that debt funds holding medium to long duration maturity papers have a high sensitivity to interest rates.

Medium-to-Long Duration Debt Funds invest in various debt papers across medium to long maturity debt papers, including corporate bonds/debentures, government securities, and money market instruments.

Typically, money is invested in medium to long-maturity debt papers of private issuers, corporate debt, and government and quasi-government securities, plus hold money market instruments (Certificate of Deposits, Commercial Papers and some cash & cash-equivalents for liquidity purposes).

Apart from the type of debt papers held, you should also pay attention to the average maturity of the underlying debt papers, coupon payments, and the yield.

Knowing the duration of the scheme (average maturity of the debt papers) helps in understanding how sensitive the underlying portfolio will be to changes in interest rates. Keep in mind, that the higher the duration, the higher the sensitivity to the interest rate and resultant risk.

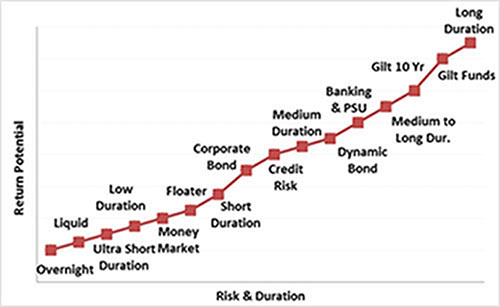

Graph 2: Risk-Return Spectrum of Debt Funds

For illustrative purposes only

For illustrative purposes only

(Source: PersonalFN Research)

On the risk-return spectrum, the Medium-to-Long Duration Debt Funds are placed at the higher end (a couple of notches below Gilt Funds and Long Duration Funds)

In other words, Medium-to-Long Duration Debt Funds are for moderate-to-high-risk investors who wish to strategically take some interest rate risk and credit risk (depending on the type of underlying debt papers held).

In a rising interest scenario, the risk gets accentuated, and the return potential is limited. On the other hand, when the interest rates have plateaued and are expected to fall, that is when the risk in Medium-to-Long Duration Debt Funds is limited and you, the investor, potentially benefit from higher yield and unlock the capital growth.

What Is the Investment Objective of Medium-to-Long Duration Debt Funds?

Broadly, the primary investment objective is to generate income through investments in a range of debt and money market instruments while maintaining the optimum balance of yield, safety and liquidity.

However, there is no assurance or guarantee that the investment objective will be realised.

How Have Medium-to-Long Duration Debt Funds Fared?

The category average returns of Medium-to-Long Duration Funds for 3 years and 5 years have been 5.80% and 6.67%, respectively (as of November 25, 2024).

Table 2: Performance of Medium-to-Long Duration Debt Funds

Data as of November 25, 2024

The list of funds cited here is not exhaustive.

Returns expressed are rolling returns in % and calculated using the Direct Plan-Growth option. Standard Deviation indicates Total Risk and Sharpe Ratio measures the Risk-Adjusted Return. They are calculated over 3 years assuming a risk-free rate of 6% p.a.

Past performance is not an indicator of future returns.*Please note, that this table represents past performance.

The securities quoted are for illustration only and are not recommendatory.

Speak to your investment advisor for further assistance before investing.

Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully.

The returns of Medium-to-Long Duration Debt Funds were muted when the interest rates began to rise from the summer of 2022 until the time the RBI maintained a status quo on them.

It is in the last one year that Medium-to-Long Duration Debt Funds have delivered decent returns against the risk taken.

However, not all funds are worth your hard-earned money, and therefore, prudent selection matters.

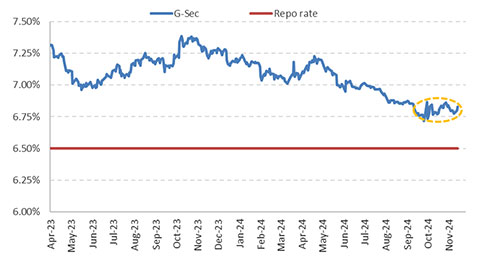

Since the October 2024 bi-monthly monetary policy, the 10-year G-sec yield has spiked by 17 bps.

Going forward, it seems that bond yields would see limited upside given that we are almost near the peak of the current interest rate upcycle (see Graph 3). On the contrary, yields are expected to fall tracking a decline in the U.S. treasury yields, and when the RBI, in time to come, reduces the policy interest rates.

Graph 3: The 10-year G-sec Yield After Inching Up Have Moved Flat

Data as of November 25, 2024

Data as of November 25, 2024

(Source: Investing.com, PersonalFN Research)

This scenario makes it favourable to invest in Medium-to-Long Duration Debt Funds and unlock the growth potential, as yields and bond prices have an inverse relation.

Having said that, as the yield gap between the U.S. and India narrows, heightened volatility cannot be ruled out. Also, the inclusion of Indian bonds in JP Morgan's Government Bond Index-Emerging Markets and Bloomberg's bond index from mid-2024 means high integration with global bond markets and vulnerability.

Hence make sure you are choosing among the best Medium-to-Long Duration Funds for your mutual fund portfolio.

Which Are the Best Medium-to-Long Duration Debt Funds to Invest in 2025?

Among the plethora of Medium-to-Long Duration Debt Funds, the three best ones to invest in 2025 are:

1. Nippon India Income Fund

2. ICICI Pru Bond Fund

3. Kotak Bond Fund

Here are some details as to why these funds are among the best in the Medium-to-Long Duration Debt Funds sub-category.

Best Medium-to-Long Duration Debt Fund for 2025 #1: Nippon India Income Fund

Nippon India Income Fund (previously called the Reliance Income Fund until Nippon AMC bought Reliance Mutual Fund) is also one of the old debt funds, launched in January 1998, has featured among the top-performing Medium-to-Long Duration Debt Funds.

This scheme is from a mutual fund house that follows a robust investment process and systems.

The primary investment objective of the scheme is to generate optimal returns consistent with a moderate level of risk. This income may be complemented by a capital appreciation of the portfolio. Accordingly, investments are predominantly made in debt & money market instruments.

NIIF follows a two-pronged strategy: Core and Tactical. The core strategy is to reflect a medium to long-term view of interest rates and the yield curve. The tactical strategy is to benefit from short-term opportunities in the market. The strategy is implemented through high-grade assets like G-Secs/ SDLs/ Corporate Bonds to generate alpha by actively using G-Secs, IRF and IRS curve.

In line with its objective, Nippon India Income Fund (NIIF) has taken a dominant exposure (80% to 90%) to Government securities (G-secs), i.e. sovereign-rated papers.

Corporate debt comprises a small proportion (up to 10%) of the total assets, which again are mainly in AAA and equivalent-rated instruments. The rest is in cash & cash equivalents to take care of liquidity needs. The fund has no investment in instruments rated AA and below, except for a minor 0.2% allocation in an Unrated Alternative Investment Fund, namely the Corporate Debt Market Development Fund.

As regards the maturity profile of the portfolio, NIIF follows its investment mandate. Nearly 50% to 100% of its assets are in longer maturity debt papers: 7 to 10 years, 10 to 15 years, and above years maturity buckets.

As per the latest portfolio (as of October 31, 2024), NIIF has 23.1% deployed in the 7 to 10 years maturity, 20.6% in 10 to 15 years maturity bucket, 19.3% in above 15 years maturity bucket, and the rest is in 5 to 7 years or lower maturity buckets. Currently, the fund's Average Maturity is nearly 12 years, and has a modified duration of around 7 years. The portfolio, at present, is positioned in such a manner sensing the opportunity at the longer end of the yield curve.

Table 3: Top-10 Holdings of Nippon India Income Fund

| Security Name |

Asset Type |

Rating |

Holding (%) |

| 07.18% GOI - 24-Jul-2037 |

Government Securities |

SOV |

20.65 |

| 07.18% GOI - 14-Aug-2033 |

Government Securities |

SOV |

15.43 |

| 07.09% GOI - 05-Aug-2054 |

Government Securities |

SOV |

12.75 |

| 07.10% GOI - 18-Apr-2029 |

Government Securities |

SOV |

11.47 |

| 07.32% GOI - 13-Nov-2030 |

Government Securities |

SOV |

10.33 |

| Tri-Party Repo (TREPS) |

Cash & Cash Equivalents and Net Assets |

Cash & Equiv |

7.00 |

| 07.30% GOI - 19-Jun-2053 |

Government Securities |

SOV |

6.55 |

| 07.10% GOI - 08-Apr-2034 |

Government Securities |

SOV |

6.41 |

| LIC Housing Finance Ltd. -SR-TR-421 7.90% (23-Jun-27) |

Corporate Debt |

AAA & Equiv |

3.80 |

| National Bank For Agriculture & Rural Development SR 25C 7.44% (24-Feb-28) |

Corporate Debt |

AAA & Equiv |

2.52 |

Data as of October 31, 2024

(Source: ACE MF, data collated by PersonalFN Research)

NIIF holds a concentrated portfolio of only 12 quality debt securities with conviction. The top 10 debt securities comprise 96.9% of the NIIF's assets, as per the portfolio as of October 2024.

The fund's prudent investment strategy has helped it achieve a decent Yield-to-Maturity (YTM) of 6.89% (which may change as the fund manager buys and sells securities). Since inception, the fund has clocked a compounded annualised return of 8.04% (as of November 25, 2024)

NIIF has clocked respectable returns over a longer time periods. Over 3 years and 5 years -- which is an ideal time frame for investing in Medium-to-Long Duration Debt Funds -- the fund has clocked an appealing compounded annualised return of 6.11% and 7.38%, respectively, (as of November 25, 2024), by managing the risk well (as denoted by the Standard Deviation).

Thus, on a risk-adjusted basis, NIIF has fared well if one considers the Sharpe Ratio and Sortino Ratio of 0.11 and 0.26, respectively (as of November 25, 2024).

The fund has outperformed many notable peers on returns, managing risk, and risk-adjusted returns. The fund has also done better than the CRISIL Composite Bond Index.

The overall performance of NIIF is influenced by the quality of the underlying debt papers held in the portfolio and their maturity profile. The fund is well positioned to potentially benefit as interest rates begin to decline. Keep in mind that, yields and bond prices have an inverse relation.

NIIF is currently managed by Mr Vivek Sharma (since February 2020) along with Mr Kinjal Desai. Both hold credible experience and educational qualifications.

Best Medium-to-Long Duration Debt Fund for 2025 #2: ICICI Pru Bond Fund

Launched in August 2008, this is one of the top-performing Medium-to-Long Duration Debt Funds that adopts a prudent investment approach. It has a track record of over 16 years now and since its inception has clocked a compounded annualised return of 8.2% (as of November 25, 2024).

ICICI Pru Bond Fund's (IPBF's) primary objective is to generate income through a diversified mix of debt and money market investments, balancing yield, safety, and liquidity.

The fund avoids investing heavily in high-risk instruments, thus protecting investors from unnecessary credit risk.

Typically, IPBF allocates 50% to 100% of its assets to debt instruments such as G-secs and corporate bonds. It also holds some of its assets in money market instruments such as Certificate of Deposits (CDs) and Commercial Papers (CPs).

The fund's careful investment strategy has helped it achieve a high yield and provide investors with excellent risk-adjusted returns. Over 3 year and 5 years -- which is an ideal time frame for investing in Medium-to-Long Duration Debt Funds -- IPBF has clocked an appealing compounded annualised return of 6.01% and 7.54%, respectively (as of November 25, 2024), by managing the risk well (as denoted by the Standard Deviation).

IPBF has consistently demonstrated strong performance, often ranking among the top in its category. The fund has outperformed many notable peers, as evidenced by its superior Sharpe ratio of 0.11 and Sortino ratio of 0.22 (as of November 25, 2024). The fund has consistently exceeded the category average and outperformed the index.

In the last one year, the fund has held nearly 60% to 87% of its assets in G-secs, in corporate debt 10% to 32%, and over 5% to 20% in money market instruments and cash & cash equivalents.

IPBF has focused on investing in sovereign-rated G-secs and high-rated corporate bonds (AAA and equivalent). The fund has no investment in instruments rated AA and below, except for a minor 0.3% allocation in an Unrated Alternative Investment Fund, namely the Corporate Debt Market Development Fund.

IPBF, in line with the investment mandate, typically maintains a portfolio duration of 4 to 7 years. Currently, the fund's Average Maturity of the portfolio is around 7 years.

Table 4: Top-10 Holdings of ICICI Pru Bond Fund

| Security Name |

Asset Type |

Rating |

Holding (%) |

| 07.10% GOI - 08-Apr-2034 |

Government Securities |

SOV |

40.74 |

| GOI FRB 22-Sep-2033 |

Government Securities |

SOV |

9.92 |

| LIC Housing Finance Ltd. -TR-433 07.71% (09-May-33) |

Corporate Debt |

AAA & Equiv |

5.49 |

| HDFC Bank Ltd. SR-US006 7.75% (13-Jun-33) |

Corporate Debt |

AAA & Equiv |

4.55 |

| Summit Digitel Infrastructure Pvt Ltd. 07.87% (15-Mar-30) |

Corporate Debt |

AAA & Equiv |

3.98 |

| HDFC Bank Ltd. SR-Y005 06.83% (08-Jan-31) |

Corporate Debt |

AAA & Equiv |

3.60 |

| 07.02% GOI - 18-Jun-2031 |

Government Securities |

SOV |

2.74 |

| Pipeline Infrastructure (India) Ltd. SR-3 07.96% (11-Mar-29) |

Corporate Debt |

AAA & Equiv |

2.56 |

| 07.18% GOI - 14-Aug-2033 |

Government Securities |

SOV |

2.24 |

| LIC Housing Finance Ltd. -TR-353 07.75% (23-Nov-27) |

Corporate Debt |

AAA & Equiv |

0.93 |

Data as of October 31, 2024

(Source: ACE MF, data collated by PersonalFN Research)

As of October 2024, sensing the opportunity at the longer end of the yield curve (as interest rates in the economy have almost peaked), IPBF has a dominant exposure (nearly 66%) to debt papers in the 7 to 10 years maturity bucket, followed by around 11% in the 5 to 7 years maturity bucket, and is holding around 7% in the 3 to 5 years maturity bucket.

Currently, IPBF has 37 debt securities in the portfolio, a Yield-to-Maturity (YTM) of 7.29% (which may change as the fund manager buys and sells securities), and a Modified Duration of around 5 years. The fund's top 10 holdings are 76.7% of the fund's total assets.

The overall performance of IPBF is influenced by the coupons and maturity of its portfolio holdings, as well as the credibility of the issuers. The fund's performance is closely tied to interest rate movements across the maturity curve due to its investments in various maturity instruments.

Its strategic diversification across various maturities allows it to navigate challenging interest rate environments effectively, providing investors with solid returns at manageable risk levels. This positions the fund well for future performance, particularly in periods of declining interest rates.

IPBF is currently managed by Mr Manish Banthia (since January 2024) and Mr Ritesh Lunawat (since January 2024). Both hold credible experience and educational qualifications.

Best Medium-to-Long Duration Debt Fund for 2025 #3: Kotak Bond Fund

Launched in November 1999, this is also one of the old debt funds adopting a prudent investment approach by prioritising investments in high-rated instruments with medium to long durations while conscientiously avoiding undue credit risks.

The primary investment objective of Kotak Bond Fund (KBF) is to create a portfolio of debt instruments such as bonds, debentures, Government Securities and money market instruments, including repos in permitted securities of different maturities, so as to spread the risk across different kinds of issuers in the debt markets.

In line with the objective, KBF has always held a predominant exposure (over 70%) to G-secs at most times, around 20% in AAA-rated corporate bonds, 0.3% is in Bharat Highway InvIT, 0.23% is in unrated Alternative Investment Fund (namely the Corporate Debt Market Development Fund), and the rest is in cash-and-cash equivalents.

KBF holds over 34 securities in its portfolio across maturities, with a majority in longer maturity buckets of 7 to 10 years, 10 to 15 years, and above 15 years maturity papers. The fund has increased its allocation to these maturity buckets since November 2022.

Currently, the fund's Average Maturity of the portfolio is around 12 years, while the Modified Duration of the fund is around 6 years. This could lead to high volatility (due to the interest rate sensitivity) but also offers the potential for superior returns when interest rates begin to decline.

Having said that, it is important to note that while KBF offers the potential for higher returns, it does carry some risks. The fund is exposed to both interest rate risk and some credit risk.

A positive point is that at present majority of its holdings are in sovereigns and AAA-rated and equivalent papers. It has no exposure to AA and low-rated papers.

Table 5: Top-10 Holdings of Kotak Bond Fund

| Security Name |

Asset Type |

Rating |

Holding (%) |

| 07.18% GOI - 24-Jul-2037 |

Government Securities |

SOV |

20.55 |

| 07.18% GOI - 14-Aug-2033 |

Government Securities |

SOV |

8.44 |

| 07.32% GOI - 13-Nov-2030 |

Government Securities |

SOV |

6.69 |

| 07.25% GOI - 12-Jun-2063 |

Government Securities |

SOV |

6.63 |

| 07.02% GOI - 18-Jun-2031 |

Government Securities |

SOV |

6.44 |

| Punjab National Bank (02-Apr-25) |

Certificate of Deposit |

AAA & Equiv |

5.46 |

| 07.30% GOI - 19-Jun-2053 |

Government Securities |

SOV |

5.12 |

| GOI FRB 22-Sep-2033 |

Government Securities |

SOV |

5.10 |

| 07.37% GOI - 23-Oct-2028 |

Government Securities |

SOV |

4.60 |

| HDFC Bank Ltd. SR-US006 7.75% (13-Jun-33) |

Corporate Debt |

AAA & Equiv |

3.43 |

Data as of November 25, 2024

(Source: ACE MF, data collated by PersonalFN Research)

As per the October 2024 portfolio, the top 10 holdings comprise 72.4% of the assets of KBF.

Since its inception in November 1999, KBF has delivered a compounded annualised return of 8.3% (as of November 25, 2024). Over 3 year and 5 years KBF has clocked an appealing compounded annualised return of 5.97% and 7.59%, respectively (as of November 25, 2024), by managing the risk well (as denoted by the Standard Deviation). Even during periods of rising interest rates, KBF has remained stable and performed well.

In the last 1 year, KBF has clocked an absolute return of 8.83% (as of November 25, 2024), better than the Crisil Composite Bond Fund Index and the category average returns.

KBF has offered respectable risk-adjusted returns, reflected in its higher Sharpe Ratio of 0.08 and Sortino Ratio of 0.18, compared to -0.02 and -0.04 respectively for the Crisil Composite Bond Fund Index.

The current YTM of KBF is a decent 7.04%, but keep in mind this may change as the fund manager buys and sells securities.

KBF looks to be well-positioned for subsequent bond market rallies. The fund has the potential to generate respectable yields, benefiting investors throughout an entire interest rate cycle. The fund has consistently ranked among the top performers in its category over longer periods -- and much of this performance is without exposing investors to undue credit risk.

The fund's well-diversified debt portfolio, spread across top-rated issuers, effectively mitigates overall risk. By successfully navigating past interest rate fluctuations, KBF has generated decent yields for investors and is expected to continue doing so.

KBF has been managed by Abhishek Bisen since January 2013, whose education background is a B.A. (Management) and MBA (Finance) from IIM-Calcutta and has experience in the bond markets spanning over two decades.

Who Should Invest in Medium-to-Long Duration Debt Funds?

Medium-to-Long Duration Debt Funds are suitable for investors with a slightly aggressive risk profile, who do not mind taking interest rate risk, and have a minimum investment horizon of 3 to 5 years. Currently, you may allocate around 25% of your debt mutual fund portfolio to some of the best Medium-to-Long Duration Debt Funds. Over a period of 3 to 5 years, Medium-to-Long Duration Funds would reward you, the investor, well provided a prudent selection is made.

So, if you are a conservative investor, prioritising the complete safety of their principal amount and are unable to tolerate near-term volatility and interest rate risk associated, then Medium-to-Long Duration Funds may be inapt for you. In such a case you if your risk appetite is low and have a short-term investment horizon of up to a year, you may consider some of the Best Liquid Funds.

[Read: 3 Best Liquid Funds for 2025]

What Are the Tax Implications of Investing in Medium-to-Long Duration Debt Funds?

All debt funds, including Liquid Funds, with effect from April 1, 2023, the capital gain arising at the time of redemption -- whether short-term (a holding period of less than 36 months) or long-term (a holding period of 36 months and above) -- is also taxed as per investors' tax slab.

[Read: Taxation of Debt Mutual Funds - Here is All You Need to Know]

For NRIs, the capital gains on debt-oriented mutual funds are subject to Tax Deduction at Source (TDS) at the rate of 30% if STCG and 12.5% in the case of LTCG.

If you have opted for the dividend option (now known as the IDCW option), for resident Indians, any dividends from Liquid Funds (under the Dividend Option) are added to the investors' total income and are taxed according to your income-tax slab, i.e., at the marginal rate of taxation.

However, if the dividend amount is more than Rs 5,000, Tax Deduction at Source (TDS) will be first done at the rate of 10%. For NRIs, the dividend/IDCW received is subject to a 20% TDS or at the rate specified under the relevant double tax avoidance agreement, whichever is lower as per section 196A of the Income Tax Act.

To sum-up...

At a time when interest rates seem almost peak out in the current interest rate upcycle, Medium-to-Long Duration Debt Funds seem well poised and suitable for your portfolio -- provided you have a moderate-to-high risk appetite and an investment time horizon of 3 to 5 years.

It would be best to invest in these funds in a staggered manner to mitigate the interest risk. The level of risk shall depend on how well the fund manager understands and plays the interest rate cycle and the quality of debt papers held. Therefore, avoid simply looking at past returns and mutual fund star ratings.

Be a prudent and thoughtful investor. When in doubt, speak to a SEBI-registered investment advisor.

Happy Investing!

Note: This write-up is for information purposes and does not constitute any kind of investment advice or a recommendation to Buy / Hold / Sell a fund. Returns mentioned herein are in no way a guarantee or promise of future returns. Mutual Fund Investments are subject to market risks, read all scheme-related documents carefully before investing.

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.