3 Best Liquid Funds for 2025 – Top Liquid Mutual Funds for 2025

Rounaq Neroy

Nov 13, 2024 / Reading Time: Approx 25 mins

Listen to 3 Best Liquid Funds for 2025 – Top Liquid Mutual Funds for 2025

00:00

00:00

The year 2024 has been an eventful one. More than 50 countries, including the largest democracies of the world, the U.S. and India, went to polls and we have seen geopolitical tensions escalating in part of the world.

In the Middle East after Hamas attacked Israel and, thereafter, the all-out war announced by Israel to eliminate Iran-backed terror groups, mainly the Hamas and Hezbollah has escalated geopolitical tensions. After top commanders of these terror groups were killed, Iran and Israel have engaged in serious military conflict with certain strategic sites being targeted.

Now with Donald Trump elected as the 47th President of the United States, Iran fears that Israel may be empowered to eliminate these terror groups completely with the support of the U.S. (as allegedly there was also a plot by Iran's Revolutionary Guard Corps to assassinate Donald Trump).

Recently, after Trump's victory, as per a Reuter report, the U.S. has carried out strikes carried out strikes against Iranian-linked targets in Syria. The U.S. has occasionally carried out airstrikes in Iraq and Syria against more than 85 targets linked to Iran's Revolutionary Guard (IRGC) and militias it backs, in a retaliation attack on U.S. troops based in Syria and neighbouring Iran to prevent Islamic resurgence.

Besides, the Russia-Ukraine war escalated in 2024. U.S. President-elect Donald Trump during his campaign repeatedly said he would end the Russia-Ukraine war and initiate peace talks even before he assumes office (upon the inauguration ceremony on January 20, 2025). While some effort is been made in that direction (by calling on European and British soldiers to put in place an 800-mile buffer zone between Moscow and Kyiv's troops, urging Russian President Vladimir Putin not to escalate the war, and assuring support to Ukrainian President, Volodymyr Zelenskyy), how this plays out in reality in time to come remains to be seen. This is because Trump is a mercurial leader, also transactional who is looking to make strategic gains.

Further, it is a publicly known fact that U.S.-China relations are strained. Trump lately has announced China's strong critic and retired Army Green Beret, Mike Waltz, as his National Security Advisor. He has been consistently in favour of strengthening the U.S. military to daunt China's aggression, particularly towards Taiwan.

As you may know, there are tensions between China and Taiwan, China and the Philippines, as well as North Korea and South Korea.

The U.S. and South Korea are allies under the 1953 Mutual Defence Treaty. The U.S. military has also been supporting Taiwan primarily through the sale of arms & ammunition for decades so as to keep China away. The crisis over Taiwan may trigger a war between the U.S. and China, even though the U.S. does not have a treaty obligation to defend Taiwan.

Under Trump 2.0 the geopolitical landscape is likely to change. Trump, while he practices America-centric policies, likes to keep everyone guessing.

Given that, there are implications on trade policies, chances of geoeconomic fragmentation, supply chain disruption, chances of inflation moving up (getting in the way of central bank rate cuts), risk-on assets such as equity experiencing high volatility, and all this may result in global economic uncertainty.

[Read: How Donald Trump's Victory Would Playout on the Indian Equity Market]

Against the backdrop of the above, it would be important to tactically hold some money safe in risk-free avenues.

Are you aware even legendary equity investor, Warren Buffett, also strategically allocates a portion of the portfolio to short-term US treasuries?

Yes, you read that right.

Berkshire Hathaway's recent quarterly report, as of September 2024, reveals that Buffett is sitting on a cash pile worth USD 325.2 billion after slashing holding in Apple Inc. This cash value accounts for around 28% of Berkshire's asset value -- the highest since 1990. It perhaps also hints at Buffett foreseeing crisis or challenges ahead.

That being said, Berkshire Hathaway has always parked cash in the short-term mainly parked in the U.S. Treasuries. This has aided in bolstering the company's interest income (in a rising interest rate scenario), managing catastrophic events (if any), plus tactically deploying this cash when value-buying opportunities are available.

For you, investors, too, it makes sense to follow Buffett's strategy and hold a portion of your investment portfolio in cash and cash-equivalent avenues. But when you tactically hold cash, Buffett advises safer instruments; he prefers safety over yields.

As an investor, you too could hold cash in safer instruments such as a pure Liquid Fund, a short-term deposit with a robust bank, and/or a savings bank account.

Watch this video to know the Best Liquid Funds:

In times when geopolitical tensions are looming and the global economy is expected to witness turbulence, holding some of your investible surplus in Liquid Funds would be worthwhile instead of going gung ho and investing only in equities with irrational exuberance not paying heed to asset allocation.

You cannot get carried away, ought to be wary, and should keep some money safe. Here's why it makes sense to invest in Liquid Funds:

- Offer you liquidity to meet unforeseen situations

- short-term goals

- Help preserve capital

- Make the most of value-buying opportunities in the equity market, whenever available.

Holding some of your hard-earned money in a Liquid Fund shall help you sleep better at night and be in the interest of your financial well-being. Remember, 'Cash is King'.

If you are looking to invest in the best Liquid Funds in 2025 as winds of uncertainty blow, read on...

What are Liquid Funds?

Liquid funds are open-ended debt mutual funds that primarily invest in short-term money market instruments with a maturity of up to 91 days.

Liquid mutual funds invest in money market instruments such as Certificate of Deposits (CDs), Commercial Papers (CPs), Term Deposits, Call Money, Treasury Bills, and so on.

The investment objective of a Liquid Fund is capital preservation and ensuring liquidity through judicious investments in the money market and debt instruments. It benchmarks its performance against the Crisil Liquid Debt Index and/or Crisil 1-year T-bill Index.

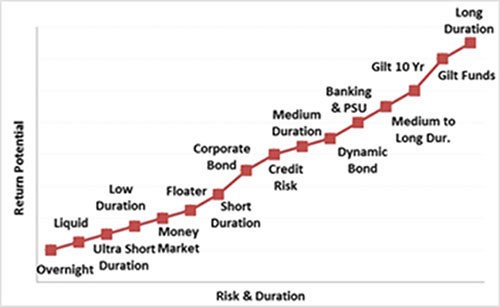

Graph: Liquid Fund Position on the Risk-Return Spectrum

(For illustration purposes only)

(For illustration purposes only)

Given the type of securities Liquid Funds hold, usually they entail low risk. The interest rate and credit risk are relatively low and so is the volatility in the NAV of Liquid Funds compared to the other sub-categories of debt funds.

Liquid funds help prioritise safety and liquidity by investing in shorter-maturity debt & money market instruments.

Thus, on the risk-return spectrum of debt mutual funds, Liquid Funds are placed at the lower end. The low-risk profile of liquid funds is meant to help protect the invested principal.

Having said that, you ought to be careful when choosing Liquid Funds to invest in. Interest rate risk, liquidity risk, default risk, etc., that apply to debt investments impact a Liquid Fund. It's important to learn from the debt fund crisis of the past -the IL&FS episode, the DHFL crisis, and so on.

Don't live by the following myths while investing in Liquid Funds...

Myth #1: Liquid Funds are risk-free -- No, the fact is there is some element of risk when you invest in Liquid Funds. They are not completely risk-free or safe as opposed to parking money in a savings bank account or short-term deposit with a robust bank. Also, during inflationary times, it is possible that the return may not keep up. Having said, when you invest in a Liquid Fund the main objective is safety and not high returns.

If a Liquid Fund offers high or better returns, it is possible that it is invested in debt papers of private issuers and has compromised on quality to generate slightly better returns, and in such a case the risk is elevated.

[Read: Does Your Liquid Fund Follow the Principle of Safety? Know Here...]

Myth #2: NAV of a Liquid Fund only goes up (does not fluctuate) -- No, this isn't true. The NAV is mark-to-market, so can fluctuate for multiple reasons.

That being said, compared to some other sub-categories of debt funds and more volatile equity funds, the fluctuation in the NAV is far less.

As they have the mandate to hold short maturity instruments (of up to 91 days or less) viz. Certificate of Deposits (CDs), Commercial Papers (CPs), Term Deposits (TDs), Call Money, Treasury bills (T-bills), etc. Liquid Funds tend to show less sensitivity to interest rate changes and experience fewer fluctuations, even in a rising interest rate environment.

Only if the portfolio characteristics are compromised, i.e. of low quality, the NAV of a Liquid Fund could be volatile. This is why it is important to understand the portfolio characteristics of a Liquid Fund.

Don't simply zero in on any Liquid Fund out there. Your focus ought to be on preserving capital rather than seeking capital appreciation, providing a small but steady income stream.

Myth #3: Liquid Funds are for conservative investors only -- Again, not true! Liquid Funds serve different objectives. When you turn conservative as equities seem expensive or are volatile owing to the headwinds in play, deploying money to a Liquid Fund is sensible.

On the other hand, when equities look attractively priced, there are favourable undercurrents, and therefore it's time to go aggressive, you could switch your money from a Liquid Fund into an equity fund. So, this way Liquid Funds are for both, conservative and aggressive investors. All you ought to do is follow an astute approach.

How to Select the Best Liquid Funds for 2025?

Well, here's what you need to do:

-

✓Evaluate the investment ideologies of the fund houses

-

✓Shortlist schemes from fund houses that follow robust investment processes and systems

-

✓Assess the fund manager's experience

-

✓Study the Scheme Information Document (SID) carefully

-

✓Ensure the expense ratio is on the lower side (whereby you earn slightly better returns than a savings bank account)

-

✓Check the historical performance (risk and returns) of Liquid Funds under consideration across time periods, but avoid making a judgment based on only that (as past returns aren't indicative of future performance)

-

✓Check the portfolio of the Liquid Fund carefully (for the type of debt & money market instruments held, their credit ratings, the average maturity, Yield-To-Maturity (YTM), and the Modified Duration (MD) of the portfolio)

Also, watch out for negative observations by independent credit rating agencies.

A Liquid Fund should prioritise safety and liquidity, and not engage in yield hunting to generate higher returns. Note, that generating higher returns is not the primary investment objective of a Liquid Fund; it is the preservation of capital.

The fund manager should also make adequate provisions to deal with unforeseen liquidity crunch and redemption pressure.

Following the principle of safety when it comes to holding cash-and-cash equivalents, you would be better off with Liquid Funds that invest predominantly in Government securities (G-Secs), quasi-government securities, AAA/A1+ rated Public Sector Undertakings (PSU) debt, and T-bills, where there is no private corporate credit risk, the portfolio is highly liquid, it is marked-to-market daily (whereby the declared NAV is real), the AUM trend is stable, and the portfolio is disclosed regularly.

Furthermore, after you have made the best choice preferably choose the Direct Plan. Under the Direct Plan, a lower expense ratio is charged than a regular plan, which may earn you a tad extra return.

What Kind of Returns You Can Expect from Liquid Funds?

In the last one year, where the RBI has maintained a status quo on policy interest rates (in consonance to keep inflation within its target range of 4.0% within a band of +/-2.0% while supporting growth), focused on the withdrawal of its accommodative stance, and then in the October 2024 bi-monthly monetary policy meeting changed the stance to 'neutral', Liquid Funds as a sub-category of debt funds have delivered around 7.12% absolute returns (as of November 11, 2024)--higher than a conventional savings bank account interest rate and the average inflation rate.

Table 1: Category Average Returns of Liquid Mutual Funds and Benchmark Indices

| Liquid Funds |

Abs Returns (%) |

CAGR (%) |

| 1 Month |

3 Months |

6 Months |

1 Year |

2 Years |

3 Years |

| Category Average Returns |

0.60 |

1.80 |

3.60 |

7.12 |

6.58 |

5.60 |

| CRISIL Liquid Debt Index |

0.60 |

1.80 |

3.62 |

7.30 |

6.68 |

5.73 |

| Crisil 1 Yr T-Bill Index |

0.61 |

1.85 |

3.63 |

7.24 |

6.32 |

5.31 |

Data as of November 11, 2024

Direct Plan and Growth Options considered. Category average for a total of 36 Liquid Funds.

Returns are on a rolling basis and in %.

Past performance is not an indicator of future returns.

*Please note, that this table only represents the best-performing schemes based solely on past returns. The securities quoted are for illustration only and are not recommendatory.

Speak to your investment advisor for further assistance before investing.

Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully.

(Source: ACE MF, PersonalFN Research) .

The Best Liquid Funds for 2025

A plethora of Liquid Funds exist, but considering the portfolio characteristics, i.e. the quality and the nature of the underlying securities held, the top 3 Liquid Funds that shall keep your money safe and liquid (amidst the geopolitical environment and potential macroeconomic uncertainty) in 2025 are:

- Union Liquid Fund

- Quantum Liquid Fund

- Parag Parikh Liquid Fund

These schemes follow the principle of safety over returns and are among the best and top 5 Liquid Funds available out there.

Table 2: 3 Best Liquid Mutual Funds for 2025

| Scheme Name |

Absolute (%) |

CAGR (%) |

Risk Ratios |

| 1 Month |

3 Months |

6 Months |

1 Year |

2 Years |

3 Years |

SD Annualised |

Sharpe |

| Union Liquid Fund |

0.60 |

1.82 |

3.65 |

7.34 |

6.68 |

5.66 |

0.09 |

1.89 |

| Quantum Liquid Fund |

0.58 |

1.74 |

3.50 |

7.04 |

6.38 |

5.41 |

0.07 |

1.67 |

| Parag Parikh Liquid Fund |

0.57 |

1.72 |

3.46 |

6.92 |

6.27 |

5.34 |

0.06 |

1.83 |

| Category Average |

0.60 |

1.80 |

3.60 |

7.12 |

6.58 |

5.60 |

0.10 |

1.64 |

| Crisil 1 Yr T-Bill Index |

0.61 |

1.85 |

3.63 |

7.24 |

6.32 |

5.31 |

0.22 |

0.80 |

| Crisil Liquid Debt Index |

0.60 |

1.80 |

3.62 |

7.30 |

6.68 |

5.73 |

0.06 |

2.50 |

Data as of November 11, 2024.

Returns are on a rolling basis and in %., calculated using the Direct Plan-Growth option.The risk-free rate is considered as 6% p.a.

Past performance is not an indicator of future returns.

*Please note, that this table only represents the best-performing schemes based solely on past returns. The securities quoted are for illustration only and are not recommendatory.

Speak to your investment advisor for further assistance before investing.

Disclaimer: Quantum Liquid Fund is a scheme from Quantum Mutual Fund, a group company of Quantum Information Services Pvt. Ltd.

PersonalFN is not in receipt of any commission directly or indirectly for suggesting the scheme.Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully.

Here are some details of why these schemes are the best in the Liquid Mutual Funds category...

-

Best Liquid Fund for 2025 #1: Union Liquid Fund

Launched in June 2011, Union Liquid Fund (ULF) aims to provide reasonable returns commensurate with lower risk and a high level of liquidity through a portfolio of money market and debt securities.

Table 3: Top-10 holdings of Union Liquid Fund

| Security Name |

Asset Type |

Rating |

Holding (%) |

| Punjab National Bank (20-Dec-24) |

Certificate of Deposit |

AAA & Equiv |

2.78 |

| 91 Days Treasury Bill - 30-Jan-2025 |

Treasury Bills |

SOV |

2.76 |

| HDFC Bank Ltd. (12-Dec-24) |

Certificate of Deposit |

AAA & Equiv |

2.32 |

| Canara Bank (16-Dec-24) |

Certificate of Deposit |

AAA & Equiv |

2.32 |

| 91 Days Treasury Bill - 23-Jan-2025 |

Treasury Bills |

SOV |

2.30 |

| Sikka Ports & Terminals Ltd. -91D (20-Nov-24) |

Commercial Paper |

AAA & Equiv |

1.86 |

| Federal Bank Ltd. (04-Dec-24) |

Certificate of Deposit |

AAA & Equiv |

1.86 |

| Reliance Jio Infocomm Ltd. -91D (06-Dec-24) |

Commercial Paper |

AAA & Equiv |

1.86 |

| Small Industries Development Bank of India (11-Dec-24) |

Certificate of Deposit |

AAA & Equiv |

1.85 |

| Reliance Jio Infocomm Ltd. -74D (16-Dec-24) |

Commercial Paper |

AAA & Equiv |

1.85 |

Data as of October 31, 2024(Source: ACE MF, PersonalFN Research)

Union Liquid Fund holds a well-diversified portfolio of around 93 debt securities across issuers with a maturity profile of largely up to 3 months.

ULF has held its assets mainly in Certificate of Deposits (CDs), Commercial Papers, Treasury Bills (T-bills), and cash-and-cash equivalents in line with its investment mandate.

By and large, ULF has consistently invested in highly rated-instruments. As per its portfolio as of October 2024, ULF holds 78.8% of its assets in AAA and equivalents, and 18.3% in sovereigns (essentially T-bills).

CP and CDs comprise, 38.0% and 40.8% respectively, and 0.1% is held in an unrated Alternative Investment Fund (AIF), specifically the Corporate Debt Market Development Fund, and the rest is in cash-and-cash equivalents as per the latest portfolio as of October 2024.

The current Yield-to-Maturity (YTM) of the ULF is 7.15%. YTM is the returns the fund expects to generate if the underlying instruments are held until maturity and may vary as the fund manager buys and sells the securities in the portfolio.

The weighted average expense ratio of Union Liquid Fund is 0.17% as of October 31, 2024, one of the lowest in the industry.

ULF is managed by Mr Parijat Agarwal, Head - Fixed Income of Union Asset Management Company, and Mr Devesh Thacker.

Parijat has over 28 years of experience. He has been managing ULF since June 18, 2021. He has worked with SBI Mutual Fund as Head - Fixed Income, State Bank of Mauritius Limited, where he handled the responsibility of managing the entire Treasury function of the bank and SUN F&C Asset Management as Fund Manager managing Fixed Income and Hybrid Funds. Parijat holds a B.E. (Electronics & Communications), PGDM from IIM Bangalore.

Devesh professional career spans over 24 years. He has been managing ULF since its inception. Before joining Union Mutual Fund in 2011 he worked with Sahara Asset Management Company. He holds a Bachelor of Commerce (Honours) degree and is a Postgraduate from the University of Pune.

As seen in Table 2, ULF has fared better than its category peers across and clocked competitive returns - at times even better than the benchmark index, i.e., the Crisil Liquid Debt Index. ULF is well-suited for investors, who do not mind higher exposure to CDs, CPs and T-bills -- aiming to sort of balance risk and returns.

-

Best Liquid Fund for 2025 #2: Quantum Liquid Fund

Launched in April 2006, Quantum Liquid Fund (QLF) aims to provide optimal returns with a low level of risk while keeping liquidity high through judicious investments in the money market and debt instruments.

Table 4: Top-10 holdings of Quantum Liquid Fund

| Security Name |

Asset Type |

Rating |

Holding (%) |

| 182 Days Treasury Bill - 07-Nov-2024 |

Treasury Bills |

SOV |

15.39 |

| 364 Days Treasury Bill - 21-Nov-24 |

Treasury Bills |

SOV |

15.35 |

| Canara Bank (16-Jan-25) |

Certificate of Deposit |

AAA & Equiv |

9.11 |

| Power Finance Corpn. Ltd. SR-192 B 07.42% (19-Nov-24) |

Corporate Debt |

AAA & Equiv |

8.21 |

| 91 Days Treasury Bill - 09-Jan-2025 |

Treasury Bills |

SOV |

6.09 |

| National Housing Bank 07.05% (18-Dec-24) |

Corporate Debt |

AAA & Equiv |

5.13 |

| National Bank For Agriculture & Rural Development - 91D (08-Nov-24) |

Commercial Paper |

AAA & Equiv |

5.13 |

| Bank of Baroda (05-Dec-24) |

Certificate of Deposit |

AAA & Equiv |

5.10 |

| Small Industries Development Bank of India (11-Dec-24) |

Certificate of Deposit |

AAA & Equiv |

5.09 |

| Export Import Bank of India -182D (24-Jan-25) |

Commercial Paper |

AAA & Equiv |

5.05 |

Data as of October 31, 2024(Source: ACE MF, PersonalFN Research)

QLF prioritises safety and liquidity over returns and invests predominantly in Government Securities, T-bills and Money Market instruments issued by Public Sector Undertakings. It follows a true liquid fund philosophy.

This distinguishes QLF from its peers, which often aim for higher returns by maintaining substantial exposure to instruments issued by private entities, potentially exposing investors to elevated credit risks.

Historically, QLF has adopted an ultra-cautious approach for its portfolio and has never chased yields for additional returns, thereby making it truly a low-risk Liquid Fund. Quantum Mutual Fund, as a fund house, follows robust investment processes and systems.

As of October 2024, the fund held a compact portfolio comprising 14 debt & money market instruments and cash and cash-equivalent assets. The top-10 holdings accounted for 79.6% of the fund's portfolio.

The weightage of 'AAA and equivalents' is to the tune of 49.9% in the fund's portfolio. Besides it has 41.0% exposure to sovereign debt, which reflects its penchant for high-credit quality.

CDs, CPs, and corporate debt accounted for 23.4%, 10.2%, and 16.4%, respectively, while the fund held around 7.8% in cash-and-cash equivalent assets. The fund also has 0.3% allocated to an unrated Alternative Investment Fund, namely the Corporate Debt Market Development Fund.

Due to its focus on safety over returns, QLF may not always rank among the top performers in the liquid fund category. However, it stands out for its strong emphasis on protecting the principal, setting itself apart from its peers. Over the past year, QLF has delivered a competitive average rolling return.

The current Yield-to-Maturity (YTM) of the QLF is 6.85%, slightly lower than some of its peers since it stays away from investing in debt instruments issued by private entities.

As of October 31, 2024, Quantum Liquid Fund's weighted average expense ratio is 0.15%, which is lower than some of its category peers.

QLF is managed by Mr Pankaj Pathak. He has been managing the fund since March 1, 2017. Pankaj has over 14 years of experience in fixed-income investments and research and holds a Post Graduate Diploma in Banking and Finance from the National Institute of Bank Management, Pune and is a qualified CFA (Chartered Financial Analyst).

QLF is ideal if you are looking for an alternative to parking money in a savings bank account, and modest return/income from it over the short-term -- over a few months, say 3 to 6 months or a year.

QLF exhibits significantly lower volatility in performance compared to its high-performing counterparts, as it stays away from taking exposure to debt instruments issued by private entities.

Hence, QLF is well-suited for conservative investors focused on protecting their principal and avoiding undue risk to their invested capital. The expected returns from QLF could be slightly higher than the interest in a savings bank account.

-

Best Liquid Fund for 2025 #3: Parag Parikh Liquid Fund

Launched in May 2018, Parag Parikh Liquid Fund's (PPLF) primary investment objective is to provide optimal returns with lower risk and higher liquidity through judicious investments in money market and debt instruments.

PPLF by consistently holding a quality portfolio since its inception has prioritised the safety of the invested principal and focused on liquidity. It avoids unnecessary credit risk that could jeopardise the safety and liquidity of the portfolio.

Table 5: Top-10 holdings of Parag Parikh Liquid Fund

| Security Name |

Asset Type |

Rating |

Holding (%) |

| 91 Days Treasury Bill - 03-Jan-2025 |

Treasury Bills |

SOV |

5.94 |

| 09.15% GOI - 14-Nov-2024 |

Government Securities |

SOV |

4.01 |

| 91 Days Treasury Bill - 07-Nov-2024 |

Treasury Bills |

SOV |

4.00 |

| Indian Oil Corporation Ltd. -89D (11-Nov-24) |

Commercial Paper |

AAA & Equiv |

4.00 |

| Indian Bank (13-Nov-24) |

Certificate of Deposit |

AAA & Equiv |

4.00 |

| Kotak Mahindra Bank Ltd. (03-Jan-25) |

Certificate of Deposit |

AAA & Equiv |

3.96 |

| Punjab National Bank (07-Jan-25) |

Certificate of Deposit |

AAA & Equiv |

3.95 |

| Axis Bank Ltd. (14-Jan-25) |

Certificate of Deposit |

AAA & Equiv |

3.95 |

| Union Bank of India (17-Jan-25) |

Certificate of Deposit |

AAA & Equiv |

3.95 |

| National Bank For Agriculture & Rural Development (17-Jan-25) |

Certificate of Deposit |

AAA & Equiv |

3.95 |

Data as of October 31, 2024

(Source: ACE MF, PersonalFN Research)

As of October 31, 2024, PPLF's portfolio was invested across 41 securities, and its top 10 holdings comprised 41.7% of the total assets.

In terms of credit quality, the PPLF holds a major portion of its portfolio in AAA and equivalent-rated instruments (54.6%) and sovereigns (41.7%). Only 0.2% is held in an unrated Alternative Investment Fund, namely the Corporate Debt Market Development Fund. In October 2024 the allocation to cash & cash equivalents was 3.5% of its overall portfolio.

CDs currently comprise 48.6% of PPLF's portfolio, issued by prominent banks such as Axis Bank, HDFC Bank, ICICI Bank, Kotak Mahindra Bank, State Bank of India, Bank of Baroda, Punjab National Bank, and Union Bank of India among others. CPs are nearly 5.0% of the portfolio, issued by Indian Oil Corporation Ltd. and NABARD. The average maturity profile of the entire portfolio of PPLF is approximately 45 days currently.

PPLF, like the QLF, is one of the rare funds that avoids unnecessary credit risk, mainly investing in very short-term, highly liquid instruments issued by the Government and PSU entities

Due to its focus on safety over returns, PPLF may not always rank among the top performers in the Liquid Fund category. That said, PPLF has delivered a competitive average rolling return.

The current Yield-to-Maturity (YTM) of the PPLF is 6.81%, slightly lower than QLF and some of its peers since it stays away from investing in compromising on the rating quality of the underlying securities in its portfolio and a strong focus on shorter maturity.

The weighted average expense ratio of PPLF is 0.16% (for the direct plan) at present, which is lower than some of its category peers.

Parag Parikh Liquid Fund is managed by Mr Raj Mehta. He has collectively around 11 years of experience in investment research and has been managing PPLF since its inception. Raj started his career with PPFAS Asset Management Pvt. Ltd. as an intern in 2012. Following this, he joined the company as a Research Analyst in 2013. He has been managing the debt component of the scheme for over 5 years now. Raj is a postgraduate in commerce (M.Com) from Mumbai University, a Chartered Accountant, and a CFA Charter holder.

PPLF primarily focuses on high-credit-quality instruments in its portfolio with a predominant emphasis on shorter-maturity Sovereign-rated assets. Thus, the fund is expected to continue its conservative management style, offering a low-risk, low-return option for investors seeking a safer liquid fund with returns comparable to a bank savings account.

In my view, investors need to have a reasonable yield expectation and investment horizon while investing in this fund. PPLF is suitable for conservative investors who have a shorter investment horizon of typically between 30 to 180 days, where safety and liquidity are the main priorities over returns.

Broadly, Who Should Invest in Liquid Funds?

If you are risk-averse, want to keep your hard-earned money safe, park money for the short-term, wish to address contingency needs, and/or keep money aside for the short-term, Liquid Funds would be a worthwhile option over and above having money in the savings bank account.

Holding an optimal sum in a Liquid Fund (say, around 12 months of your regular monthly expense) shall provide you with decent liquidity and stand as a buffer if equities turn volatile, and if wish to use that opportunity to move money from a Liquid Fund into a suitable equity fund.

Also, in case of an emergency, you will not have to depend on anyone-just as Buffett doesn't like to depend even on his friends.

Units of Liquid Funds can be redeemed on a T+1 basis. In some cases, the instal-redemption facility is also available.

The redemption value is disbursed to the linked savings bank account of the investor on a working day following the day of the valid redemption request. Keep in mind that there isn't any exit load applicable for units held in a Liquid Fund or for 7 days or longer.

For an investment horizon of up to a year, Liquid Funds are an ideal choice.

What are the Tax Implications of Investing in Liquid Funds?

All debt funds, including Liquid Funds, with effect from April 1, 2023, the capital gain arising at the time of redemption -- whether short-term (a holding period of less than 36 months) or long-term (a holding period of 36 months and above) -- is also taxed as per investors' tax slab.

[Read: Taxation of Debt Mutual Funds - Here is All You Need to Know]

For NRIs, the capital gains on debt-oriented mutual funds are subject to Tax Deduction at Source (TDS) at the rate of 30% if STCG and 12.5% in the case of LTCG.

If you have opted for the dividend option (now known as the IDCW option), for resident Indians, any dividends from Liquid Funds (under the Dividend Option) are added to the investors' total income and are taxed according to your income-tax slab, i.e., at the marginal rate of taxation.

However, if the dividend amount is more than Rs 5,000, Tax Deduction at Source (TDS) will be first done at the rate of 10%. For NRIs, the dividend/IDCW received is subject to a 20% TDS or at the rate specified under the relevant double tax avoidance agreement, whichever is lower as per section 196A of the Income Tax Act.

Finally, be a thoughtful investor, instead of considering just the historical absolute returns to choose the best Liquid Funds. When in doubt, speak to a SEBI-registered investment advisor.

Happy Investing!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. Registration granted by SEBI, Membership of BASL and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

Mutual Fund investments are subject to market risks, read all scheme-related documents carefully.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and use such independent advisors as he believes necessary.