Here’s How You Can Plan the Down Payment for Your Home Loan with Mutual Funds

Ketki Jadhav

Dec 27, 2022 / Reading Time: Approx. 4.5 mins

Listen to Here’s How You Can Plan the Down Payment for Your Home Loan with Mutual Funds

00:00

00:00

Owning a house is a dream of millions of people in India. As they say, 'Ghar baar baar nahi banta', most individuals go out of their budget to buy the house of their dreams, which makes them opt for a home loan. Technological advancement and innovations in finance have made availing of online home loans much easier than before. However, when you apply for a home loan, the financial institutions ask for a down payment, which many potential home loan borrowers can not easily afford. Besides, even if you can afford to make the minimum required down payment, it is advisable to pay a higher home loan down payment to reduce the debt burden.

If you aspire to buy a house in the near future and looking for ways to reduce your debt burden amidst the rising interest rates, this article elucidates why you should pay a maximum down payment and how you can plan to achieve it with mutual funds.

A down payment is a sum of money that a borrower has to pay upfront in the initial stages of buying a product or service. It is generally calculated as a portion (percentage or fixed amount) of the total purchase price, and the buyer usually takes a loan to finance the balance amount.

When speaking of home loan down payment, banks and Housing Finance Companies (HFCs) typically ask for a 10% to 20% down payment, considering your income, repayment capacity, property value, and many more factors.

If you are eager to buy a house and have no money for a down payment, you may get tempted by banks and HFCs offering home loans with zero-down payments. While it seems like an alluring idea to get a new house without dropping any money, there are several downsides, such as high-interest rates, higher interest outgo, and no equity built up, among others.

If you are buying a house that you are going to live in, it cannot be considered an investment; hence, it is best to keep the home loan EMIs affordable. Besides, the Reserve Bank of India (RBI), has yet again increased the Repo Rate, which may result in more increase in the home loan interest rates.

A higher down payment implies a better repayment capacity. Hence, if you are paying a higher down payment, financial institutions can offer favourable loan terms. So, rather than increasing the debt and consequently EMIs, it makes sense to increase the home loan down payment, without excessively stressing your budget so that your total interest outgo is reduced.

Making a higher down payment enables you to possess more equity in the property, which eliminates the need for borrowing a large home loan. Bear in mind, the lower the loan amount, the earlier you get debt free.

Let us see with the help of an example how paying a higher down payment can reduce your debt burden and saves your interest outgo:

Suppose you are buying a house that costs Rs 1 Cr.

Calculation with 10% down payment:

| Total Cost of Buying a Property |

Rs 1 Cr |

| Loan Amount |

Rs 90,00,000 |

| Down Payment |

Rs 10,00,000 |

| Loan Tenure |

20 years |

| Interest Rate |

8.20% |

| Interest Amount |

Rs 93,36,886 |

| Monthly Home Loan EMI |

Rs 76,404 |

| Total Amount Payable |

Rs 1,83,36,886 |

Now, suppose instead of paying a minimum down payment, you pay a 35% down payment, i.e., Rs 35,00,000.

Image source: www.freepik.com

Image source: www.freepik.com

Join Now: PersonalFN is now on Telegram. Join FREE Today to get 'Daily Wealth Letter' and Exclusive Updates on Mutual Funds

Calculation with 35% down payment:

| Total Cost of Buying a Property |

Rs 1 Cr |

| Loan Amount |

Rs 65,00,000 |

| Down Payment |

Rs 35,00,000 |

| Loan Tenure |

20 years |

| Interest Rate |

8.20% |

| Interest Amount |

Rs 67,43,305 |

| Monthly Home Loan EMI |

Rs 55,180 |

| Total Amount Payable |

Rs 1,32,43,305 |

As you see in the above example, by increasing your down payment by Rs 20 lakhs, you can save Rs 50,93,581 on the total payable amount.

Therefore, if you think you are not ready to make the minimum down payment that will help you reduce your debt burden and interest outgo, it is advisable to postpone the purchase and make a solid financial plan to pay a higher down payment.

Since property values are skyrocketing, coming up with such sums is not as easy as it sounds. However, with a robust financial plan, you can achieve the targeted amount of a home loan down payment without compromising on your other goals.

While you can invest money in fixed-income products like fixed deposits and bonds, they might not be able to generate adequate returns to fulfil your goal within the horizon you are planning to make a purchase. But, investing in mutual funds through a mix of lump sum and SIP modes of investment can help you accumulate the required sum of money over the time available.

You can use your existing investments made in bank fixed deposits, savings accounts, recurring deposits, debt mutual funds, bonds, debentures, etc., to make a lump sum investment in equity mutual funds. However, make sure you do not liquidate investments made for specific goals, such as retirement, child's education, contingency fund, etc., as it can create financial stress if/when the time to use these funds come near.

Suppose you want to make a 30% down payment in the next 7 years for a purchase of a house that costs you Rs 1 Cr today. However, considering the 8% inflation rate, the cost of the property will go up to Rs 1,71,38,243. So, you must be ready with approximately Rs 52 lakhs for a 30% down payment when making the property purchase.

Your existing investments across different asset classes can be liquidated to further invest towards your goal of owning a house totalling up to Rs 10 lakhs. It makes sense to invest it in equity mutual funds in lumpsum, which will help you reach your target comfortably.

For the remaining sum of money, an SIP route of mutual fund investment is suggested to steadily build a corpus over time and generate inflation-beating returns. You can use online tools like SIP calculators that are easily available on several financial websites. It can assist you in determining the exact investment amount required to achieve your envisioned goal. Let us say apart from Rs 10 lakhs in a lump sum, you can comfortably contribute Rs 15,000 per month from your income for the next 7 years without compromising on your other goals.

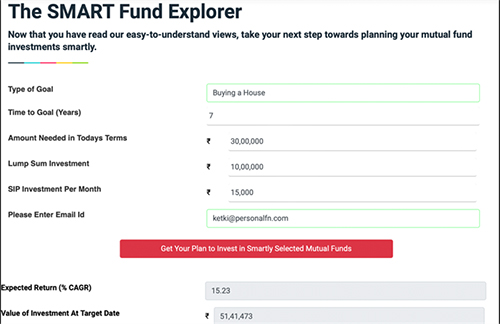

PersonalFN's SMART Fund Explorer can help you plan your mutual fund investments smartly with a mix of lump sum and SIP investments. You can simply provide details like the type of goal (buying a house), time to a goal (7 years), the amount needed in today's terms (Rs 30 lakhs), lump sum investment (Rs 10 lakhs), and SIP investment (Rs 15,000).

Here's how the SMART Fund Explorer looks after you input the required details:

Considering the details entered, PersonalFN's SMART Fund explorer will provide you with a decent expected rate of return on the investments and the value of an investment at the target date. As you scroll down, the explorer will offer you two mutual fund investment options (A and B) that you can choose based on your risk appetite. Furthermore, you can also get instant access to the list of the best suitable mutual fund schemes as per your selected plan by enrolling on PersonalFN's SMART Fund Explorer.

At PersonalFN, we are committed to providing you with unbiased and honest views and opinions on various personal finance issues that can impact your investments and finances. We have been providing personalised Financial Planning solutions to our clients in India and to NRIs to help them meet their financial goals and objectives.

To conclude:

Availing of a home loan with zero or bare minimum amount of down payment can substantially increase the cost of your loan. Whereas increasing the amount of your home loan down payment with a robust financial plan can help you save a considerable interest outgo. However, before making a huge down payment, it is advisable to assess your financial situation and ensure you do not liquidate investments made for other goals, as it can disturb your future and make you financially stressed.

Warm Regards,

Ketki Jadhav

Content Writer