Should You Sell Your Mutual Funds Now

Rounaq Neroy

Aug 07, 2024 / Reading Time: Approx. 12 mins

Investors in the Indian equity markets are on a roller coaster of late. Earlier this year, in the run-up to Lok Sabha elections nervousness set and volatility spiked. Later, on June 4, 2024, when the Lok Sabha elections results were declared and Narendra Modi-led-BJP fell short of a majority, the bellwether, BSE Sensex, plummeted by a remarkable -5.7% (or -4389.73 points).

But soon later, when it was clear that a Modi-led-coalition government would be formed with the support of the TDP (headed by Shri N. Chandrababu Naidu) and JDU (led by Shri Nitish Kumar), who secured 16 and 12 seats, respectively, plus all other partners, the market bounced and scaled to a new lifetime high.

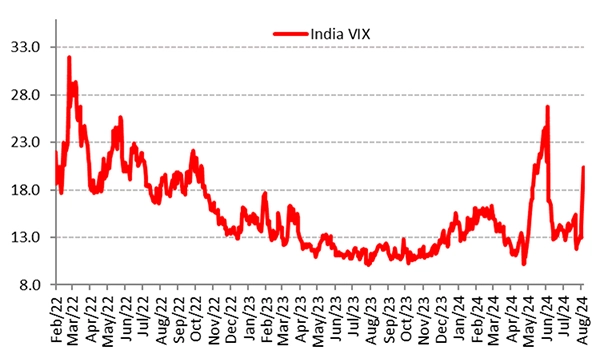

The spike in the volatility, as reflected by India's Volatility Index or VIX, sort of settled down. But once again, volatility in the Indian equity market has intensified.

Graph: India's VIX Has Spiked

Data as of August 5, 2024

Data as of August 5, 2024

(Source: NSE, data collated by PersonalFN Research)

Some of the key reasons for the Indian equity market turning volatile are:

-

Looming geopolitical tensions: The recent high profiling killing of Hamas's political chief, Ismail Haniyeh in Tehran, and Hezbollah's senior commander, Fuad Shukr in Beirut allegedly by Israel, have escalated tensions in the Middle East. Iran has vowed retaliation. There is already an ongoing war between Russia and Ukraine. Taiwan's Ministry of National Defence (MND), on X (formerly Twitter) has stated that 9 Chinese military aircraft and 9 naval vessels were operating around Taiwan between Sunday to Monday. 6 of the aircraft crossed the median line and entered Taiwan's eastern ADIZ. Taiwan's MND has monitored the situation and responded accordingly. China has explored its grey zone tactics and exhibited its prowess, and considering this, according to media reports, Taiwan is readying its citizens for a war. Bangladesh, too, is facing social unrest owing to anti-government violent protests by students over a quota system in civil service government jobs, and Prime Minister, Sheikh Hasina, has fled the country - which reminisces of what happened in Sri Lanka in 2022.

-

There is fear of the U.S. potentially slipping into a recession (as certain indicators, particularly, jobs and housing market concerns point in that direction) and delayed rate cut by the U.S. Federal Reserve in view of sticky inflation, may only shallow the recession.

-

The hike in interest rates by the Bank of Japan (BoJ) to 25 basis points (bps) has also upset the market. BoJ also signalled that further rate hikes are on the cards to deal with inflation. Besides, there is a bond tapering plan. Monthly purchases will be reduced to ¥ 3 trillion (U.S. $19.9 billion) by the first quarter of 2026 compared with the current pace of ¥ 6 trillion, according to the BoJ governor. There is a clear change in the dovish image of BoJ, and interestingly, it comes at a time when Japan's economic growth has been rather uneven, with contractions reported and debt-to-GDP at a staggering all-time high. So, what the market is currently witnessing is the unwinding of the Yen carry forward trade (a term referring to borrowing money at a lower rate and investing in markets and asset classes that offer higher rates). For over 30 years BoJ maintained almost zero interest rates (an ultra-loose monetary policy), and now, given the rate hike, money will no longer be available cheap, which is rattling the market.

-

The risk to the inflation trajectory due to supply chain disruptions, geopolitical tensions, geoeconomic fragmentation, and climate change is also worrying the market, as that may hold back major central banks from cutting interest rates soon to support growth.

-

A fact also is that India is commanding a premium vis-a-vis emerging markets and the world. The Morgan Stanley Capital International (MSCI) India Index Price-to-Equity (P/E) Ratio is over 27x, while the MSCI Emerging Markets Index and MSCI World Index trail P/Es are around 16x and 22x, respectively (as per the latest factsheets). These frothy valuations are also prodding foreign portfolio investors to take money off the table.

Not having seen this sort of intense volatility, the new investors in equities -- those who entered after the COVID-19 pandemic not wanting to miss the high returns -- now appear worried or anxious. Many of these investors have not seen bouts of intense volatility, remarkable corrections, or market cycles. The most common term searched on Google currently is "Should I sell/redeem my mutual funds now."

To answer that question, there ought to be strong reasons for you to sell your mutual funds. You should not be timing the market and approaching mutual funds with the mind of the trader.

You see, while timing your entry and exit in equity mutual funds can appear as an easy way to sail through the volatile nature of the market, it's not easy. One can never tell if the market has bottomed out or whether it will keep rising after reaching a peak. Timing the market is futile and should not matter especially when you are addressing long-term financial goals.

Also note that trading in mutual funds would lower the returns, add to your transaction costs, exit loads, and tax outgo. Modi 3.0 coalition government in the union budget 2024-25 (presented on July 23, 2024) has increased the capital gain tax, for both short term capital gains and long term capital gains.

Keep in mind, that mutual funds are essentially an investment product, and not meant to trade --buy and sell frequently like stocks.

[Read: Do You Invest in Mutual Funds with the Mind of a Trader?]

When you invest in mutual funds, the job of tactical allocation to cash or staying invested in equity is of the fund manager and the Asset Management Company.

As long you own mutual fund schemes that are in congruence with your risk profile, broader investment objective, aligning investment with your financial goals, as well as choosing schemes that are from fund houses that follow robust investment processes and systems, having robust risk management measures in place, and a commendable performance track record, you need not worry about timing the market.

Uncertainty is part of life and market-linked investments.

"Successful investing is about managing risk, not avoiding it," said Benjamin Graham, the father of value investing.

[Read: Are You Setting Your Risk-Return Expectations Right While Investing in Mutual Funds?]

The history of the Indian equity market stands testimony to the fact that despite the negative events, Scam 1992, the Ketan Parekh scam, the dotcom bubble, the downturn of 2002, the global financial crisis of 2008-09, the Dubai debt debacle of 2009-10, the debt crisis in Greece, the slowdown in China, the COVID-19 crash in March 2020, Russia's invasion of Ukraine, Israel-Hamas war, and many such events; the Indian equity markets have trounced and performed well (over the long run).

So, focus on time in the market. By giving sufficient time to your investments, being focused, and following investment potentially you would be able to generate wealth and accomplish your envisioned financial goals.

Now I'm not saying you should never sell. Selling is of course as important as making investments; it is part of the process of generating wealth. But, as I mentioned earlier, there ought to be strong reasons for you to sell your mutual funds (or any investment instrument for that matter).

You can consider selling your mutual funds in the following circumstances:

1. When Your Goal Is Nearing, Or You Have Already Accomplished the Financial Goal/s

This should be the primary reason why you should sell your mutual funds. If your equity funds delivered better than expected returns, you may have ended up reaching your goal before the target date. It could be a good time to take money off the table.

Similarly, when you are just 2-3 years away from the envisioned goal, it is time to gradually trim allocation in equity mutual funds and shift to safer avenues such as pure liquid funds and/or bank fixed deposits. This shall guard the corpus from any potential sharp correction at the end of the goal period.

2. When Your Mutual Scheme Has Consistently Underperformed

Despite giving ample time to a mutual fund scheme to deliver decent returns, i.e. it has underperformed its and many of its category peers, across time frames and market phases, you could cull out that scheme from your mutual fund portfolio and replace it with a better alternative.

At times, even a carefully selected mutual fund may underperform. Thus, a timely mutual fund portfolio review is necessary.

3. Change in Fundamental Attributes of the Scheme Since You First Invested

The mutual fund industry is under constant change. Fund houses too, as a result, are adjusting their product basket. If the fundamental attributes of the scheme have changed (say in terms of investment philosophy/strategy/style of the scheme, change in scheme category, etc.) since the time you first invested, and now if it does not align with your investment objective, risk profile and financial goals, you could consider redeeming or selling that mutual fund scheme to align with your needs.

4. For Portfolio Rebalancing Purpose

Asset allocation is the cornerstone of successful investing. Moreover, asset allocation is not static but ever evolving -- it changes as age progresses, risk profile alters, investment objectives change, and as you approach closer to the envisioned financial goals.

It is important to follow the asset allocation that is best suited for you. Say, originally, when you invested the recommended allocation was 70:30 (equity: debt), but now due to market gains, it has increased to say 80:20, you need to trim it down.

Likewise, if your risk profile has changed and/or you are nearing the financial goal, the asset allocation also needs a reset. For this purpose, you may sell certain schemes and/or reduce weight in them by partial selling or redeeming.

Similarly, if there is too much portfolio overlap in the schemes you hold, you could consider selling or redeeming those schemes. Mutual funds with overlapping holdings reduce diversification potential. Overlapping assets could lead to the potential problem of overexposure and concentration risk, thus amplifying the risk exposure in your portfolio.

[Read: Mutual Fund Portfolio Overlap - What it Is and How to Avoid It]

5. For Financial Emergency

Life is bound to throw curve balls at us and it's important to be financially prepared by making prudent investments. To address emergency needs, while you may have kept a certain sum of money in a liquid fund and/or parking money into a savings bank plus term deposits, and it is not enough, then you could consider selling or redeeming certain mutual funds. Ideally, 12 to 18 months of regular monthly expenses, including EMIs on loans, should be held in liquid funds or in the bank for emergency purposes, so that you do not have to dig into your investment assigned for envisioned financial goals.

These should be some of the five best reasons to sell or redeem your mutual funds. Not trading or frequent profit booking. Watch this video:

Selling mutual funds ought to be a very well-considered decision and mustn't be arbitrary.

You need to ensure that you analyse or review your mutual fund portfolio carefully, seeking the help of a SEBI-registered investment adviser, ensure you have prudently assessed the market conditions, looked at suitable alternatives, are aligning investment as per your goals, evaluating the cost of selling or exit schemes, and taking into account the tax implications.

Selling mutual funds needs to be a meticulously thought-out process, whereby you strategically position the portfolio.

"To invest successfully over a lifetime does not require a stratospheric IQ, unusual business insights, or inside information. What's needed is a sound intellectual framework for making decisions and the ability to keep emotions from corroding that framework." ...remember these pearls of wisdom from the book "The Intelligent Investor" by Benjamin Graham, the father of value investing.

Be a thoughtful investor.

Happy Investing!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

Disclaimer: This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.