Should You Buy SGBs on Dhanteras from the Open Market at a Premium Now?

Rounaq Neroy

Oct 29, 2024 / Reading Time: Approx. 9 mins

Listen to Should You Buy SGBs on Dhanteras from the Open Market at a Premium Now?

00:00

00:00

Sovereign Gold Bond (SGBs) has been one of the smart ways of buying gold. It earns you, the investor, a fixed interest of 2.50% p.a. (called the coupon rate) payable semi-annually on the nominal value until the maturity period of 8 years plus the opportunity to benefit from capital appreciation over the holding period. Note, that one SGB is equal to one gram of gold.

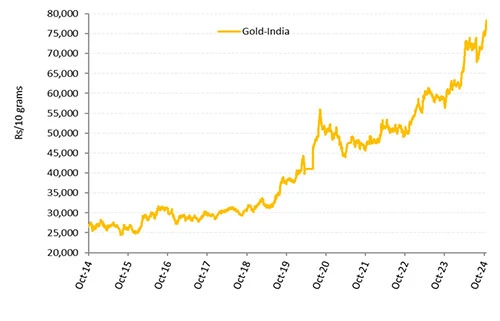

Gold in INR terms touched Rs 77,997 per 10 grams (as of October 24, 2024), thus clocking a stunning 23.9% on a year-to-date (YTD) basis.

Graph: Gold Has Displayed Its Sheen

Data as of October 24, 2024

Data as of October 24, 2024

MCX spot price of gold used.

Past performance is not indicative of future returns.

(Source: MCX, data collated by PersonalFN Research)

If you are considering adding, SGB to your investment portfolio this Dhanteras or during one of one the auspicious muhurats, then read on.

SGBs were launched by the Modi-led-NDA government in November 2015 as a part of the Gold Monetisation Scheme, and since then, abetted by the price appreciation, gold has more than doubled investors' wealth.

So far, the Reserve Bank of India (RBI) -- which is the issuing authority for SGBs on behalf of the RBI and announces the issuances of these bonds in four tranches in the financial year -- has issued 67 tranches of SGBs between FY16 and FY24.

For 2024-25, the RBI has made no announcement so far on the issuance.

The last issue of SGB (2023-24 Series IV) was in February 2024 at an issue price of Rs 6,263 per gram.

However, considering that gold is appreciating plus the fact that SBGs offer 2.5% interest p.a., there is still a lot of interest in SGBs among smart investors.

The SGBs series launched thus far and having around 6 to 7 years left for maturity are still garnering interest from some investors in the secondary market (as SGBs are available for trading in the cash segment of the stock exchanges, the BSE and NSE).

This is reflected in the trading premium some of the SGB series are commanding compared to the reference rate for SGB, which is the India Bullion and Jewellers Association's (IBJA) 999 purity gold rate.

For example, the IBJA 999 purity gold rate (exclusive of GST) as of October 24, 2024, was Rs 7,825 per gram, whereas the gold rate for the last SGB 2023-24 Series IV (maturing in February 2032) was Rs 8,561.09 per gram -- that's a premium of 9.4%. A fact is almost all SGB series are trading at a premium currently on the NSE.

This evinces the faith of most investors to appreciate even more going forward. To know if you should buy gold on Dhanteras 2024, watch this video:

But Will Gold Indeed Continue to Exhibit Its Sheen?

Well, the following factors are expected to prove supportive for the precious yellow metal:

-

The escalating geopolitical tensions in many parts of the world, particularly the Middle East, the ongoing war between Russia and Ukraine, strained relations between the U.S. and China, between China and Taiwan, China and the Philippines, between North Korea and South Korea

-

High likelihood of major terror attacks as well as an increase in cyber-attacks

-

The uncertainty around who wins the upcoming U.S. Presidential election (scheduled for November 2024) and the specific effects of the policies

-

Chances of geoeconomic fragmentation due to geopolitical tensions

-

The possibility of supply chain disruptions poses a major upside risk to inflation, particularly imported inflation

-

Prospects of a weak U.S. Dollar (USD)

-

Chances that global economic growth may slowdown

-

Burgeoning global debt, which includes borrowing of the government, corporates, and households. As per the IMF, the global public debt is very high and will approach 100 per cent of GDP by 2030

And against this geopolitical setting and economic environment, central banks of the world are also continuing to add sizeable amounts of gold as a part of their reserve management, which in turn would work in favour of gold.

The central banks of BRICs are planning to keep 40% of reserves in gold. Among the BRICs and globally, India and China -- traditionally the largest consumers of gold in the world -- are also adding gold to their reserves. In 2024, the RBI has so far brought home a little over 100 tonnes of its gold that was stored in the UK.

As per the World Gold Council (WGC), central bank gold purchases (as a part of their reserve management strategy) would be supportive of gold.

Having said that buying gold, at a significant premium to the current spot rate of the IBJA, in my view, is a very risky proposition.

You see, most investors prefer following a 'hold to maturity' strategy when it comes to SGB, leading to illiquidity of SGBs due to low volumes compared to other traded securities. Thus, you may not be able to sell it on the exchange before maturity.

Also, even if you follow a 'hold to maturity' strategy the risk is still quite high; the margin of safety narrows when you pay the premium. If gold prices do not appreciate as much, the question is how will you make up for the premium paid?

Instead, a Better Avenue Is to Invest in a Gold ETF and/or a Gold Savings Fund

Gold ETF can help you to benefit from the upside potential of gold better.

A Gold ETF is a passively managed mutual fund scheme that aims to track the domestic price of physical gold by making direct investments in gold.

It offers investors an innovative and cost-efficient way to invest in gold without having the hassle of physically holding it. On purchase of a Gold ETF, units are allotted to you, the investor.

The units purchased are backed by 0.995 finesse of physical gold. The physical gold is held in vaults by an appointed custodian for the Gold ETF by the mutual fund house on your, the investors' behalf. Besides, this gold with the custodian is insured and valued periodically, as per the guidelines stipulated by the Securities and Exchange Board of India (SEBI).

Thus, the investor can own gold without having to worry about making charges (as in the case when purchasing gold in a physical form), storage hassles, risk of misplacing, theft, etc.

The investment objective of a gold ETF is to generate returns broadly in line with the domestic price of gold and gold-related instruments subject to a tracking error.

By and large, when gold appreciates and the NAV goes up, you, the investor benefit. To read more about gold ETFs and how you can purchase gold ETF units, click here.

The other option is to invest in Gold Saving Funds. It is a Fund of Fund scheme investing in underlying Gold ETFs, which benchmarks the performance against the prices of physical gold. It strives to produce parallel returns that closely resemble the underlying Gold ETF.

Hence, the investment objective of a Gold Savings Fund is to generate returns that closely correspond to returns generated by the underlying Gold ETF.

To invest in a Gold Savings Fund, you are not required to have a Demat account. To buy units in a Gold Savings Fund, approach the fund house or your mutual fund distributor. You can also do a SIP in gold with a Gold Savings Fund.

Strategically Allocate to a Gold ETF and/or a Gold Savings Fund

This Dhanteras -- which is one of the most auspicious muhurats for gold buying -- or during Diwali you may consider strategically allocating around 10% to 15% of your entire investment portfolio to gold and holding it with a long-term view (of over 8 to 10 years) by assuming a moderately high risk.

In times of escalating geopolitical tension, increase in public debts, and economic uncertainty, gold would prove its trait of being a safe haven, a hedge, and a store of value. With this tactical allocation, gold will prove its worth as an effective portfolio diversifier.

Be thoughtful in your approach.

Happy Investing!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in the securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.