Why Gold Is Scaling New Highs

Rounaq Neroy

Mar 06, 2024 / Reading Time: Approx. 9 mins

Listen to Why Gold Is Scaling New Highs

00:00

00:00

In my last article on gold, published in December 2023, I explained how the precious yellow would fare in the year 2024.

Recently, gold made headlines by touching a record high, both in the Indian Rupee (INR) and U.S. Dollar (USD) terms. In INR, gold touched Rs 65,000 per 10 grams (in Delhi), while in USD, it was 2,163 per ounce (as of March 5, 2024).

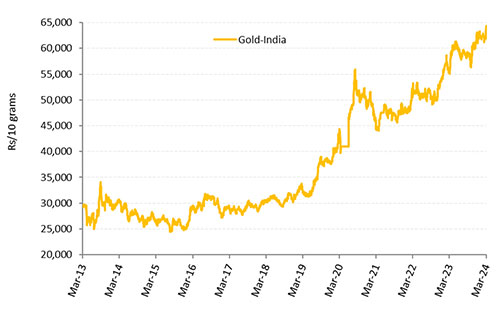

Graph 1: Gold Has Become Bold Over the Long Run

Data as of March 5, 2024

Data as of March 5, 2024

MCX spot price of gold used.

Past performance is not indicative of future returns.

(Source: MCX, data collated by PersonalFN Research)

The graph above shows, gold has become bold in the last decade and exhibited its sheen. So, what's driving up the price of gold? Watch this video:

Well, there have been a variety of factors. But some of the recent key factors are:

-

Intensified geopolitical tensions, whether it is the Russia-Ukraine war, Russia-NATO relations, conflict in West Asia---particularly the war between Israel and certain militant groups of the region, attacks in the Red Sea, the drone attacks on ships in the Red Sea and Indian Ocean, offensive countermeasures taken by North Korea by firing long-range missiles and deepening ties with Russia and China, hostile relations between China and Taiwan, and more.

-

Geoeconomic fragmentation, which increases trade barriers, threatens the supply chain, pushes up the prices of goods and services, and brings policy uncertainty.

-

Elevated CPI inflation, which nudges central banks to increase interest rates in the economy. Due to supply chain issues and climate events, consumers have borne the brunt of high cost of living. While there has been moderation of late, the RBI is of the view that food price shocks could interrupt the disinflation process. The inflation trajectory, going forward, would be shaped by the outlook on food inflation (about which there is considerable uncertainty).

-

Tighter liquidity conditions in the U.S., Europe, and China. Even in India, liquidity and financial market conditions, after remaining in surplus in the first five months of FY24, have turned into a deficit since September 2023 after a gap of four and half years, as per the RBI's assessment. Only after adjusting for the government's cash balances the potential liquidity in the banking system is still under surplus.

-

The burgeoning debt-to-GDP ratio of many economies. The cumulative global debt has touched a record high of USD 313 trillion in 2023, with the developing economies (viz. India, Argentina, China, Russia, Malaysia and South Africa) scaling a fresh peak, according to the Institute of International Finance (IIF). The U.S., Japan, France, Britain, Brazil, India, and China are facing high debt-to-GDP. In some cases, it is higher than the pre-COVID pandemic levels. The IIF has observed appetite for borrowing is growing particularly in emerging markets in 2024, as international sovereign bond issuance volumes have increased. However, the rising debt-to-GDP also signals potential challenges in debt repayments in an elevated interest rate scenario.

-

The likelihood of delayed policy rate cuts by the U.S. Federal Reserve and other major central banks, even though there are signs of economic vigour and some moderation in CPI inflation. Central banks perhaps do not want inflation to de-anchor by reducing the policy interest rates prematurely, particularly when there are renewed flashpoints on the geopolitical front and supply chain disruptions. The major central banks of the world are hoping to see further down (much below the target set for inflation) before making a rate cut announcement.

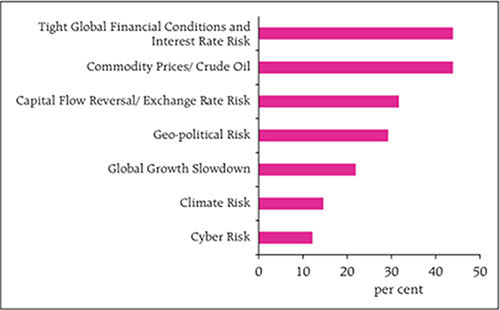

Graph 2: The Potential Risk to Financial Stability

(Source: RBI Financial Stability Report, December 2023)

(Source: RBI Financial Stability Report, December 2023)

All the above factors have an impact of weighing down on economic growth, which, in turn, could have a bearing on corporate earnings. The RBI, too, has taken cognisance of these risks in its latest Financial Stability Report, December 2023.

Other than that, as you may be aware, 2024 will be an election year. General elections are scheduled in India, the U.S., Europe, Mexico, Indonesia, and several other countries. This means there could be some element of political uncertainty and change in dispensation may have a bearing on future economic policies. For these reasons, the volatility in the high-risk asset class, such as equities, has increased.

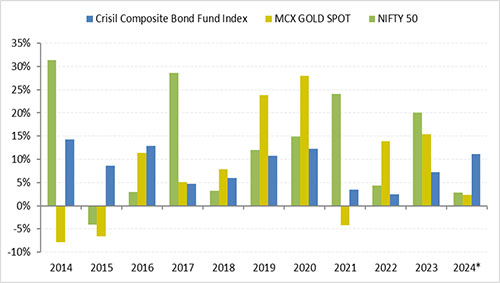

Graph 3: Gold Has proved to be a Hedge in the Investment Portfolio

*Data as of March 5, 2024

*Data as of March 5, 2024

MCX spot price of gold used. Returns expressed are in absolute terms considering domestic currency.

Past performance is not indicative of future returns.

(Source: MCX, ACE MF, Data collated by PersonalFN Research)

The current times warrant a strategic allocation to gold. The graph above shows how gold has displayed its being a safe haven, a hedge, and has been an effective portfolio diversifier during uncertain times.

In times when stock market (equity) returns have disappointed investors, like in the years 2011, 2013, 2015, 2016, 2018, and 2022, the precious yellow metal or gold as an asset class has rewarded investors. Last year, while equities fared well, posting double-digit returns, gold also exhibited sheen against the backdrop of simmering geopolitical tensions and various macroeconomic risks despite higher interest rates in the economy.

That said, note that not all asset classes move in the same direction always. Graph 3 validates the fact that there is no consistent winning asset class year-on-year. Therefore, holding some gold in your investment portfolio could prove to be a hedge.

Going forward if policy interest rates are reduced to support the economy and abetted by lower CPI inflation reading, gold may make fresh highs. This is because gold prices and interest rates, usually, share an inverse correlation.

Similarly, if CPI inflation increases, interest rates in the economy stay elevated, and the global economy slows down, gold may still do well. Want to know if gold move up in 2024, watch this video:

History suggests that in times of severe economic slowdown or recession, gold has exhibited its sheen and fared better than equities, as smart investors prefer gold and high-quality debt instruments.

A fact is that, unlike financial assets, gold is a real asset - meaning gold does not carry credit or counterparty risk. Even a stronger U.S. Dollar, hasn't deterred investors from buying gold.

Recognising the various forms of risks, even central banks as part of their risk management and risk mitigation, would continue to buy gold (as they did in 2023), observes the WGC, which would again prove supportive for gold.

You see, gold is a strategic long-term asset class. The long-term secular uptrend exhibited by gold (as seen in Graph 1) cannot be ignored and highlights the importance of owning gold in the portfolio. In the last decade, gold has clocked a CAGR of nearly +8.1% as of March 5, 2024. Since India's independence, gold has clocked a CAGR of nearly +9.0% as of March 5, 2024.

If inflation cools (due to the monetary policy actions), the real returns (also known as inflation-adjusted returns) on investment in gold will get better.

I suggest tactically allocating around 10% to 15% of your entire investment portfolio towards gold and holding it with a long-term view (of over 5 to 10 years) by assuming moderately high risk.

In 2024 the returns for gold as an asset class may not be in double digits as seen in the years 2019, 2020, 2022, and 2023, but it would potentially prove to be a hedge in your portfolio.

Invest in gold the smart way --in the form of Gold ETFs, Gold Savings Funds, and/or Sovereign Gold Bonds (SGBs).

Don't get dissuaded by the tax implications, wherein your capital gains, irrespective of long-term or short-term, in Gold ETFs and/or Gold Saving Funds are taxed as per income-tax slab, i.e. as per the marginal rate of taxation.

[Read: Why It Still Makes Sense to Invest in Gold Mutual Funds Despite the Change in Tax Rule]

In case you are going with SGB, note that interest earned is fully taxable as per your tax slab (i.e. at the marginal rate of taxation). It is essential to note that there is no Tax Deducted at Source (TDS) on the interest, meaning you must report this income when filing returns and pay advance tax accordingly. At the end of the 8-year maturity period of SGBs, the capital gain arising, irrespective of short-term or long-term is exempt from tax.

So, approach gold sensibly for your financial future.

Happy Investing!

Note: This write-up is for information purposes and does not constitute any kind of investment advice or a recommendation to Buy / Hold / Sell a fund. Returns mentioned herein are in no way a guarantee or promise of future returns. Mutual Fund Investments are subject to market risks, read all scheme-related documents carefully before investing.

We are on Telegram! Join thousands of like-minded investors and our editors right now.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.