What Should be Your Debt Mutual Fund Strategy in 2022 Amid Expectation of Interest Rate Hike by RBI?

Divya Grover

Dec 29, 2021

Listen to What Should be Your Debt Mutual Fund Strategy in 2022 Amid Expectation of Interest Rate Hike by RBI?

00:00

00:00

Debt mutual fund returns turned unattractive in 2021 as RBI held interest rates at a multi-year low to support economic growth amid the pandemic. Barring a few exceptions, a majority of debt mutual fund schemes clocked returns comparable to the repo rate.

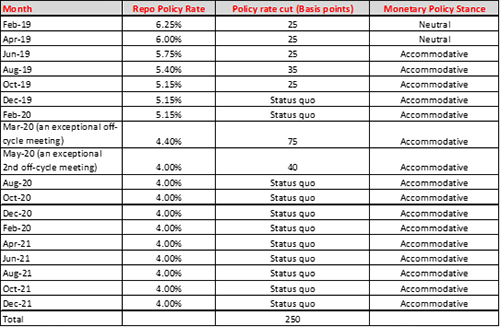

Since 2019, RBI has cut interest rates by 250 basis points as the economy was gripped by a prolonged slowdown. This includes a sharp 135 bps cut between March 2020 and May 2020 that RBI undertook to mitigate the impact of COVID-19 on the economy.

The RBI's Monetary Policy Committee left the policy repo rate and reverse repo rate unchanged at 4% and 3.35%, respectively, during its December 2021 meeting. Meanwhile, it also maintained its accommodative stance to support economic growth. This was the ninth consecutive time that the RBI left interest rates unchanged.

Earlier, there was some expectation of a hike in interest rate towards the end of the calendar year 2021 as the Indian economy revived at a steady pace during the year on the back of easing of lockdown restrictions, pick up in most business/industrial activities to pre-COVID levels, growing vaccination drive, and improving consumption trends.

However, the RBI maintained its status quo amid the uncertainty posed by the 'Omicron' variant of COVID-19.

Table 1: RBI's series of policy rate cuts to address growth concerns

Data as of December 8, 2021

(Source: RBI Monetary Policy Statements)

Will RBI hike interest rates in 2022?

Though RBI has retained India's GDP growth projection at 9.5% for the financial year 2021-22, the rapidly rising Omicron cases in India could act as a major headwind to the economy. That said, despite the prevailing threat of Omicron to the economy, RBI may not have much leeway to keep the interest rate at the current multi-year low levels for long due to sticky inflation trends.

Retail inflation came in higher at 4.9% in November compared to 4.5% in October led by increase in food prices. Core inflation (which excludes food, fuel, and light), which had moderated to 5.85% until September 2021, has increased to 6.20% in November 2021, the highest in five months.

Inflation is expected to witness further uptick driven by elevated international energy and commodity prices and waning favourable base effect. Unseasonal rains in many parts of the country have posed a risk to food & beverage inflation. Besides, a series of hikes in prices of petrol, diesel, LPG, and CNG, has led to higher readings in the fuel & light inflation category.

If Omicron causes another round of partial/local lockdowns in India and even in the other parts of the world, the supply disruptions might push inflation up.

Besides, the US Federal Reserve has hinted at three rate hikes in 2022 and tapering of stimulus measures amid rising inflation. The Bank of England has already hiked interest rate from the record lows.

Given the risks emanating from inflationary pressures and the expectation of a hike in interest rate in developed economies, the RBI may have to take steps to withdraw excess liquidity in the coming months and subsequently hike interest rates.

(Image source: www.freepik.com - photo created by rawpixel.com)

Notably, the RBI has been rebalancing the liquidity surplus by shifting it out of the fixed rate overnight reverse repo window into the variable rate reverse repo (VRRR) auctions of longer maturity. VRRR is a measure that the RBI takes to absorb excess liquidity from the banking system. It has proposed to enhance the 14-day VRRR auction amounts on a fortnightly basis.

The higher inflation projection and measures to withdraw excess liquidity indicate that the interest rate cycle may have bottomed out.

However, rate hikes will depend on the future course of the pandemic. If the Omicron variant wrecks havoc, policy normalisation in India would not begin anytime soon. But if the new variant of COVID-19 turns out to be benign, as suggested by the initial reports, RBI may look at withdrawing liquidity more aggressively and consider some hike in interest rate towards the beginning of the next fiscal year. Else, it will wait till the second half of 2022 when the economic growth gathers a firmer ground, and there is further clarity on the movement of inflation.

The investment strategy to follow while investing in debt mutual funds now:

As the economic activities have revived after the relaxation of most COVID-19 restrictions, interest rates seems to have bottomed out. The RBI will have to start normalising rates to ensure a positive real rate of interest for depositors amid rising inflation. Therefore, a hike in interest rate by RBI seems imminent next year.

However, there is uncertainty regarding when it will happen, as well as the extent and pace of the rate hike since RBI will strive to support economic recovery at the same time respond to risks emanating from inflation and tapering of stimulus by the US. This could keep the debt market volatile in the next 6-12 months.

With the expectation of interest rates facing more of an upside pressure, generating returns from longer duration debt instruments may not be an easy task for the debt mutual fund managers (since bond prices and interest rates are inversely related). Once interest rates start showing sharp upside movement, the funds having higher exposure to longer duration instruments may witness a decline in NAV.

Table 2: Debt mutual funds returns turned tepid in 2021

| Category |

YTD Return (%) |

| Banking and PSU Fund |

3.79 |

| Corporate Bond |

3.90 |

| Credit Risk Fund |

9.78 |

| Dynamic Bond |

4.40 |

| Gilt Fund with 10 year constant duration |

1.98 |

| Liquid |

3.31 |

| Low Duration |

4.98 |

| Medium Duration |

5.84 |

| Medium to Long Duration |

3.39 |

| Overnight Fund |

3.16 |

| Short & Mid Term |

2.89 |

| Short Duration |

5.17 |

| Ultra Short Duration |

4.24 |

| Crisil Composite Bond Fund Index |

3.34 |

| Crisil 1 Yr T-Bill Index |

3.41 |

| Crisil 10 Yr Gilt Index |

1.15 |

YTD as of December 28, 2021

(Source: ACE MF)

It would be prudent to invest in debt mutual funds that are less inclined towards longer duration instruments and keep their focus on the shorter end of the yield curve. Debt mutual funds that invest in the short maturity segment witness minimal mark to market impact when interest rates rise. Accordingly, investors should consider investing in funds having a higher allocation to shorter maturity instruments as they would carry less interest rate risk once interest rates change direction and start moving upwards.

The lower residual maturity helps the fund to follow an accrual strategy where it can earn from coupon payments and roll over the assets on maturity. The accrual strategy also helps reduce the impact in a rising interest rate scenario.

Depending on your financial goals, risk profile, and investment objective, you can consider investing in debt mutual fund categories such as, Liquid Funds, Ultra Short Duration Funds, Dynamic Bond Funds, Corporate Bond Funds, and Banking & PSU Debt Funds.

Notably, most debt mutual fund schemes, other than those mandated to invest in long term securities, have already reduced average maturity profile to around 3 years or less and therefore the impact of rate hike on such schemes could be less. So, if you have invested in such schemes you don't need to rejig your portfolio.

But it is important to look at the credit profile of the schemes you are investing in. Even though economic sentiments have improved, avoid investing in schemes that hold higher allocation to moderate to low rated instruments as it can expose you to higher credit risk. Stick to debt mutual funds where the fund manager does not chase yields but instead focuses on government and quasi-government securities.

Lastly, remember that though debt mutual funds are relatively stable compared to equity mutual funds the returns are not guaranteed. Therefore, it is important to understand the various risk involved viz. interest rate risk and credit risk before selecting a debt mutual fund for your portfolio; avoid selecting schemes based on its recent performance.

PS: If you are looking for quality mutual fund schemes (including Equity-linked Saving Schemes) to add to your investment portfolio, I suggest you subscribe to PersonalFN's premium research service, FundSelect. PersonalFN's FundSelect service provides insightful and practical guidance on which mutual fund schemes to Buy, Hold, and Sell.

Currently, with the subscription to FundSelect, you could also get Free Bonus access to PersonalFN's Debt Fund recommendation service DebtSelect.

If you are serious about investing in a rewarding mutual fund scheme, subscribe now!

Warm Regards,

Divya Grover

Research Analyst

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds