This Is How Your Credit Score Impacts Your Financial Future

Ketki Jadhav

May 11, 2022

Listen to This Is How Your Credit Score Impacts Your Financial Future

00:00

00:00

Credit bureaus have been functioning in India for over a decade, yet many individuals are unaware of them, and a minority can understand their credit reports. The reason behind the low awareness about credit reports and credit score utility is the low financial literacy ratio.

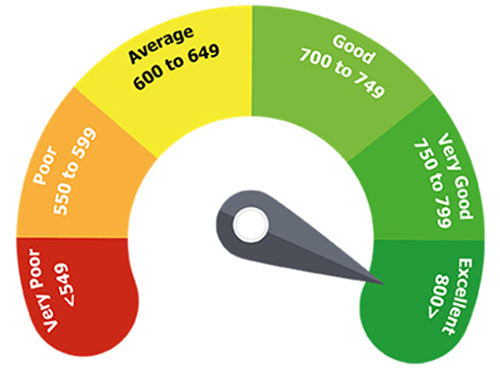

A credit score is a three-digit number ranging from 300 to 900 that depicts an individual's loan repayment capacity. Out of many factors that banks and NBFCs consider while approving or rejecting your loan application, your credit score is the major factor since it gives lenders an idea about your creditworthiness. The higher the credit score, the more banks, and NBFCs will be interested in granting you a loan because a higher score indicates a lower probability of loan default. Therefore, a higher credit score is the key to loan approval, whereas a lower credit score reduces the chances of getting a loan.

The Credit Score Indicator below can help you understand the different ranges of credit scores:

In India, we have four credit bureaus that calculate credit scores:

1. TransUnion CIBIL

2. Equifax

3. Experian

4. CRIF High Mark

The primary purpose of these bureaus is to rate an individual or a business entity after collecting and analysing their respective credit data and repayment history. Banks and NBFCs across the country largely use the CIBIL score from TransUnion Credit Information Bureau (India) Limited (CIBIL).

Your credit score is affected by the following factors:

1. Repayment History: The credit bureaus keep track of the monthly repayments towards your loans, credit card bills, and other credit repayments.

2. Credit Utilisation Ratio: It is a percentage of credit utilised against your available credit limit. It can be calculated by dividing your total outstanding debt balance by your total credit limit.

3. Credit History: Having a good credit history over the years helps you increase your credit score by a few points.

4. Types of Credit Accounts: Managing multiple types of loans, such as secured and unsecured, can positively impact your credit score.

5. Credit Enquiries: the number of times you or the lenders enquire about your credit score also negatively impacts your credit score.

Image source: www.freepik.com

Image source: www.freepik.com

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds

How does your credit score affect your financial future?

Your credit score impacts your financial future in the following ways:

1. Future Loan Approvals:

Your credit score determines how creditworthy you are to your future lenders. Whenever you apply for a new loan to any lender, the first thing they do is check your credit report. If your credit score is more than the lender's threshold limit credit score, they will consider your loan application for the next step. A good to excellent credit score indicates you are a low-risk borrower. Whereas if you do not have the adequate credit score required by the lender, your application will be rejected outright.

2. Faster Loan Processing:

Lenders consider a consumer's profile to be low-risk if you have a good to excellent credit score, which ultimately leads to faster approval of your loan application. Whereas if your credit score is not up to the mark, the lenders will have to consider other factors to analyse the risk in your profile, which can delay the loan process. Also, if you have an excellent credit score, your chances of getting pre-approved and instant loan offer increase.

3. Better Loan Terms:

A credit score not just impacts your ability to take new loans but can also impact the cost of your loans. When you have a good credit score, the lenders will be interested in offering you loans. This, in turn, gives you the power to negotiate with the lenders on loan terms, such as rate of interest, processing fee, any other fees and charges, an extension of loan tenure, etc. Whereas having an average or below-average credit score may result in loan offers with a very high-interest rate.

4. Access to High-End Credit Cards:

A good credit score makes you eligible for high-end credit cards that offer the maximum reward points and cashback offers. These cards generally have a higher credit limit. Moreover, these cards have tie-ups with several merchants, which can help you buy a desired product/service at a discounted price. An average credit score might give you access to credit cards, but these cards might not turn out to be significant for you.

5. Employment Eligibility:

Many employers check the credit score of the candidates they have finalised as their employees. This check is specifically done for positions that involve direct contact with cash. The reason behind credit score checks for employment is to avoid any future complications. So, if your credit report shows delayed and missed payments, the employer can consider your profile as high-risk.

6. Refinancing Eligibility:

If you already have a loan and need a top-up loan or want to refinance your existing loan, the lender will consider your application only if you have timely repaid all your monthly repayments. The lenders usually avoid refinancing loans or providing top-up loans when your credit score is low.

7. Saving Potential:

A low credit score is an indication that your dues are higher than your income. It also implies that you need to pay more attention to your spending pattern and achieve financial discipline. Not being able to make the monthly repayments can cause you to borrow more money, which becomes a never-ending cycle and ultimately makes you fall into a debt trap. In this situation, you will not be able to save any cash for your future financial goals. Whereas having a good credit score means you are timely repaying the dues, resulting in avoiding late payment charges and availing of loans at better loan terms. The money saved can be invested in different investment avenues, which will help you create wealth over time.

8. Peace of Mind:

When you know you are paying your monthly repayments and credit card bills on time, you are following financial discipline and managing your finances well. This will give you peace of mind relating to your finances. Whereas not being able to pay the dues and bills on time will create financial stress, which will affect your health and relationships.

To Conclude:

As discussed above, a credit score is an important parameter that determines your credibility for several aspects of your financial future. To ensure a good financial future, access to loans, and employment eligibility, it is advisable to increase or maintain your credit score by timely repaying your EMIs, maintaining the credit utilisation ratio, and having a good mix of different types of loans, etc.

Warm Regards,

Ketki Jadhav

Content Writer