"As in all successful ventures, the foundation of a good retirement is planning." - Earl Nightingale (an eminent author and radio speaker)

In a country like India, which is yet developing and lacks adequate social security, making provisions for your retirement is even more important.

Among all the envisioned financial goals, retirement is among the most important ones. It's the phase of life when your regular income (in the form of salary or business and profession) will stop, thus leaving you to depend on the investments made to meet your retirement expenses.

For retirement planning, there are galore of investment avenues, and the Employee's Provident Fund (EPF) is one of the most popular options among them.

What is the Employee Provident Fund (EPF)?

The Employee Provident Fund is a social security scheme for employees in factories and other establishments. The scheme was launched in 1952 by the Employee Provident Fund Organisation (EPFO) of India, a statutory body which falls under the Government of India's Ministry of Labour and Employment.

In essence, EPF is retirement benefit scheme wherein the employee and employer contribute a certain sum every month that goes towards the employee's provident fund. The amount thus accumulated and the interest accrued thereon can be withdrawn by employees post their retirement to fund their expenses. Apart from provident fund, the scheme also provides pension fund and deposit-linked insurance fund.

The EPFO extends its services to entire India, including the Union territory of Jammu & Kashmir and Union territory of Ladakh. The number of subscribers under EPF has grown manifold since its launch. The number of members stood at 25.88 crore as of March 2021, while the total corpus of EPFO stood at Rs 15,690 billion at the end of the year.

Investments in EPF enjoys Exempt-Exempt-Exempt status. This means that the contributions made by the employee are eligible for tax deductions under Section 80 C of the Income Tax Act, the interest earned on the total investments, and the withdrawal (including partial withdrawals for specific expenses) are exempt from the purview of taxation.

What are the benefits of investing in EPF?

-

Capital appreciation at low risk - The EPF is managed under the supervision of the Government of India, which makes it a safe avenue as it has statutory backing. The scheme invests predominantly in debt instruments to offer capital appreciation without exposing the portfolio to high volatility. The returns are guaranteed as the interest rate on EPF is decided every year by the government.

-

Long-term wealth creation - EPF does not require you to make huge lump sum investment. The contribution towards EPF is deducted on a monthly basis from the employee's salary. The wealth created through monthly contribution to EPF and interest earned on it allows you to amass a sizeable corpus and lead a decent lifestyle in your retirement years. Click here to estimate the size of your EPS corpus at the time of retirement

-

Pension benefit - Around 8.33% of an employer's contribution is directed towards the Employee Pension Scheme. Once the employee retires from the service, he/she is eligible for pension which can be a great help in funding your regular expenses post retirement.

-

Tax-saving - Employee's contribution towards their PF (up to Rs 1.5 lakh) is eligible for tax deduction under Section 80C of the Indian Income Tax Act. In addition, interest earned on EPF account is tax free in case of contribution up to Rs 2.5 lakh every financial year. Moreover, withdrawal of the PF balance, after a continuous service of 5 years, is excluded from income tax.

-

Easy Premature Withdrawal - Members of EPF India are entitled to avail benefits of partial withdrawal. Individuals can withdraw funds from their PF account to meet their specific requirements like pursuing higher education, buying/constructing a house, wedding expenses, or for availing medical treatment.

(Image source: freepik.com - photo created by jcomp)

(Image source: freepik.com - photo created by jcomp)

Join Now: PersonalFN is now on Telegram. Join FREE Today to get 'Daily Wealth Letter' and Exclusive Updates on Mutual Funds

How does EPF work?

With a view to offer social security and a secure retired life to all employees in exchange for their years of hard work and services, the EPF Act, 1952 has mandated all organisations (industries and other establishments) that have 20 or more employees to register under the EPF scheme. An employee can only join EPF if he/she works for a company covered by the EPF & MP Act, 1952.

The Act defines an "employee" as "any person who is employed for wages in any kind of work, manual or otherwise, in or in connection with the work of an establishment and who gets his wages directly or indirectly from the employer, and includes any person employed by or through a contractor in or in connection with the work of the establishment and engaged as an apprentice, not being an apprentice engaged under the Apprentices Act, 1961 (52 of 1961) or under the standing orders of the establishment".

What it means that the principal employer has to ensure that all liabilities towards EPF of employees who are not on the company's payroll (i.e. contractual employee) are taken care off, either directly or through the contractor.

However, EPFO has clarified that student trainees being paid stipend during on-the-job training while pursuing technical/ professional courses will not be considered as employee for the purpose of EPF & MP Act.

Moreover, the Act does not apply to Co-operative Societies / Establishments, employing less than 50 persons and working without the aid of power.

-Guide-Banner-02-01-2022-(Article)_1.jpg)

Where is the contribution made under EPF directed?

Both employer and employee contribute to the EPF in equal proportions (12% of Basic and Dearness Allowance) on a monthly basis. The contributions are payable on maximum wage ceiling of Rs 15,000.

The contribution made by the employer is directed in three different schemes of EPF which are as follows:

-

Employees' Pension Scheme (EPS), 1995

-

Employees' Provident Fund Scheme (EPF), 1952

-

Employees' Deposit Linked Insurance Scheme (EDLI), 1976

The employer's contribution of 12% includes 8.33% to EPS and 3.67% to EPF. Apart from this, the employer contributes an additional 0.5% towards EDLI.

In the case of contribution by employee, the entire 12% is directed towards EPF.

An establishment that has less than 20 employees can voluntarily register for EPF. In such a case, the contribution rate from both employee and the employer will be 10% instead of 12%. The lower contribution of 10% will also apply under the following circumstances:

-

Industries declared as sick industries by the BIFR

-

Organizations suffering an annual loss much more as compared to their net value

-

Organisations involved in coir, guar gum, beedi, brick, and jute industries

-

Organizations operating under the wage limit of Rs 6,500

What is the Employees' Pension Scheme (EPS)?

The Employees' Pension Scheme, 1995 (EPS 1995) aims at providing economic sustenance during old age and survivorship coverage to the member and his/her family. The EPS 1995 is funded by diversion of 8.33% of monthly wages (subject to the wage ceiling which is presently Rs 15,000/- per month) from the employers' share of contribution. The Central Government also contributes 1.16% of monthly wages.

This part of your monthly contribution is targeted towards offering pension on:

-

Member Pension upon retirement /superannuation

-

Member Pension upon disablement while in service

-

Withdrawal Benefit upon leaving service after putting in less than 10 years but more than six months of service

-

Spouse Pension upon death of member

-

Spouse Pension upon death of member as pensioner

-

Children Pension along with spouse pension (up to age 25) for two children at a time

-

Orphan Pension upon death or remarriage of spouse (up to age 25)

-

Disabled Child Pension to children/orphan (life-long)

-

Nominee Pension to the Nominee when no family exists

-

Dependent Parent Pension when no family and nominee exists

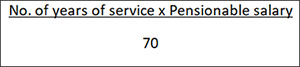

The formula for calculating member pension under EPS is as follows:

What is the Employees' Deposit Linked Insurance Scheme (EDLIs)?

The scheme gives life cover to the employees of the organized sector. It is a group term insurance plan which gets activated on the bereavement of the employee paying a maximum sum assured of Rs 7 lakh to the nominee. The cost of the scheme is borne by the employer. It is important to note that the deceased employee should have been an active member/contributor to the EPF at the time of his/her death to be eligible for the insured amount. Most employers opt out of the EDLI and choose to have a group life insurance cover for their employees; this works out better for the employees and does not increase any cost to the employer.

If the deceased member remained in 12 months of continuous employment prior to the death, the nominee is entitled to minimum benefit under EDLI of Rs 2.5 lakh. The actual benefit amount is based on the employee's last drawn salary which will be calculated as follows:

The average monthly wages drawn (subject to a maximum of Rs 15,000), during the twelve months preceding the month in which the member died, multiplied by 35 times plus 50% of the average PF balance in the account of the deceased during the preceding twelve months or during the period of his membership, whichever is less subject to a ceiling of Rs 1.75 lakh.

How is the EPF Contribution Calculated?

The EPF amount is contributed on a monthly basis. To understand how EPF contribution is calculated let us look at the below example...

Let's assume that you earn Basic + DA of Rs 20,000 per month. Employee's EPF contribution per month will be 12% of Rs 15,000 (ceiling amount) i.e. Rs 1,800. No contribution is made towards EPS by the employee. Employer's contribution will also be Rs 1,800 but it will be split as follows -

| Employer's contribution to EPF |

3.67% of Rs 15,000 |

Rs 550 |

| Employer's contribution to EPS |

8.33% of Rs 15,000 |

Rs 1,250 |

(For illustration purpose only)

In the above example, since the salary earned by the employee is more than wage ceiling, the EPF contribution will be calculated on a maximum of Rs 15,000.

Let us assume another example where the basic + DA is Rs 14,000 (less than the ceiling of Rs 15,000). In this case

Employee's EPF contribution will be 12% of Rs 14,000 i.e. Rs 1,680.

Employer's EPF contribution will be 3.67% of Rs 14,000 i.e. Rs 514

Employer's EPS contribution will be 8.33% of Rs 14,000 i.e. Rs 1,166

Pension contribution is not paid in the case of following circumstances:

- When an employee crosses 58 years of age and is in service (EPS membership ceases on completion of 58 years).

- When an EPS pensioner is drawing Reduced Pension and re-joins as an employee.

In both the cases the Pension Contribution of 8.33% is added to the Employer share of EPF.

If an employee is drawing more than Rs 15,000 (Basic + DA), he/she is not required to become a member of the EPF, if the individual is not already holding the PF membership. Otherwise, if both the employer and employee are willing, he/she can become a member under Para-26 (6) of the PF scheme. The option has to be submitted to the EPF office within 6 months of joining.

In case an employee, who is not existing EPF/EP member joins on or after 01-09-2014 with wages above Rs 15000, then the pension contribution part will be added to employee share, EPF.

In all other cases Pension Contribution is payable. A member joining after 50 years age, if not a pensioner does not have choice of not getting the Pension Contribution on grounds that he will not complete 10 years of eligible service. The social security cover is applicable till he/she is a member.

For International Worker, higher wage ceiling of 15000/- is not applicable from 11-09-2010.

Note:- In case an existing EPS member (as on 01-09-2014) whose Pension contribution was paid erstwhile EPS wage ceiling of 6500/- contribution to contribution above Rs 15000/- wage ceiling from 01-09-2014 he will have to give a fresh consent and an amount of 1.16% on wages above 15000/- will have to be contributed by him in pension Fund (A/C No 10) through the employer.

Under EDLI contribution is made on the maximum wage ceiling of Rs 15,000 and each contribution is to be rounded to nearest rupee. EDLI contribution to be paid even if member has crossed 58 years age and pension contribution is not payable. This is to be paid as long as the member is in service and contribution towards EPF is being made.

How are the employees protected if the employer turns insolvent?

In case an employer defaults on PF contribution, there are various measures in place for recovering the amount such as attachment of bank accounts, realisation of dues from debtors, attachment & sale of properties, arrest & detention of employer, action under Section 406/409 of the Indian Penal Code and Section 110 of Criminal Procedure code, and prosecution under section 14 of the EPF & MP Act, 1952.

If the employer becomes insolvent or when a company is wound up, the PF contributions will be paid in priority over other debts

Can members contribute at a higher rate?

Yes, salaried individuals who receive monthly payments in their salary account have the option to opt for Voluntary Provident Fund (VPF). Under this, employees can choose to contribute towards EPF at a higher rate than the mandated limit of 12%. Employees are allowed to contribute a maximum of their Basic salary along with DA towards their VPF account. The employer is not required to match the contribution in the case of VPF. The VPF account is linked to the employee's EPF account and the interest rate offered on VPF is per the prevailing EPF interest rate.

Once the employee has fixed the VPF contribution, the same cannot be terminated or discontinued before the completion of 5 years. To be eligible to withdraw, the VPF account must be in existence for at least five years. In the case of early withdrawal, the interest earned will be subject to tax deductions.

How long can an employee continue EPF membership?

There is no restriction on membership period. A person can continue his/her membership even after leaving the establishment. However, if no contribution is received into PF account for 3 consecutive years, the account will not earn any interest after 3 years from stopping of contribution.

An employee can continue as a PF member even after attaining superannuation age if he/she continues to work. Do note that an employee who has already attained the age of 58 cannot become a member of the Pension Fund.

The member has the two options in case he/she decides to delay the pension beyond 58 years:

1) Member opts for receiving pension after attaining 59 or 60 years of age but the pension contribution stops after 58 years. In this scenario, the quantum of pension is increased by 4% per year beyond 58 years.

2) Member opts for receiving pension after 59 or 60 years of age but pension contribution continues after 58 years. In this case, the quantum of pension will be higher than the aforementioned case.

What interest rate did you earn on your EPF contribution? How has the EPF interest rate moved historically? How is interest credited?

Historically, EPF interest rates have moved as follows:

| Year |

% Rate of Interest Announced |

Increase / Decrease / Constant |

% Change |

| 2000-01 |

11% |

Decrease |

-1.00% |

| 2001-02 |

9.50% |

Decrease |

-1.50% |

| 2002-03 |

9.50% |

Constant |

0% |

| 2003-04 |

9.50% |

Constant |

0% |

| 2004-05 |

9.50% |

Constant |

0% |

| 2005-06 |

8.50% |

Decrease |

-1.00% |

| 2006-07 |

8.50% |

Constant |

0% |

| 2007-08 |

8.50% |

Constant |

0% |

| 2008-09 |

8.50% |

Constant |

0% |

| 2009-10 |

8.50% |

Constant |

0% |

| 2010-11 |

9.50% |

Increase |

1.00% |

| 2011-12 |

8.25% |

Decrease |

-1.25% |

| 2012-13 |

8.50% |

Increase |

0.25% |

| 2013-14 |

8.75% |

Increase |

0.25% |

| 2014-15 |

8.75% |

Constant |

0% |

| 2015-16 |

8.80% |

Increase |

0.05% |

| 2016-17 |

8.65% |

Decrease |

-0.15% |

| 2017-18 |

8.55% |

Decrease |

-0.10% |

| 2018-19 |

8.65% |

Increase |

0.10% |

| 2019-20 |

8.50% |

Decrease |

-0.15% |

| 2020-21 |

8.50% |

Constant |

0% |

| 2021-22 |

8.10% |

Decrease |

-0.40% |

(Source: epfoindia.gov.in)

So this answers our first question. For the financial year 2021-22, the government had fixed the interest rate on EPF at 8.1%, which is the lowest in over four decades.

The Central Government revises the interest rate given on the EPF every year.

How does the EPFO allocate its assets?

Below is the investment pattern of the EPF -

| Asset Type |

Minimum Investment |

Maximum Investment |

| Government Securities and Related investments |

45% |

50% |

| Debt instruments and Related Investments |

35% |

45% |

| Short-term Debt Instruments and Related Investments |

0% |

5% |

| Short-term Debt Instruments and Related Investments |

5% |

15% |

| Asset Backed, Trust Structured, and Miscellaneous Investments |

0% |

5% |

The EPFO invests around 45-50% of its assets in government securities. The minimum investment limit for the Debt instruments and Related Investments such as corporate debt and Basel III Tier-I bonds issued by scheduled commercial banks is 35% with the maximum ceiling at 45%. It also invests up to 5% in short term debt such as money market instruments.

EPFO invests 5-15% in equities of companies that have market cap of more than Rs 5,000 crore. The equity portion is predominantly allocated in Nifty and Sensex ETFs. The government also recently allowed EPFO to invest up to 5% in asset-backed, trust-structured, and miscellaneous investments including the alternate investment funds (AIFs), real estate investment trusts (REITs), and units of infrastructure investment trusts (InvIT).

What is the Universal Account Number (UAN)?

The Universal Account Number (UAN) is a 12-digit identification number assigned to all EPF members. The UAN mandate was brought into being in October 2014 with an aim to create a single umbrella under which all PF accounts can be easily accessed by members. UAN allows you to access and manage your PF records and also check balance to ensure that employer is crediting your account every month. Once the UAN is created it stays constant throughout the employment years, even when you switch jobs. Through UAN member portal you can complete various tasks such as withdrawing and transferring your PF money any time with having to visit EPFO office. It has also made the process of employee verification by EPFO very simple. Employees can merge as many as 10 old PF accounts under one UAN.

If it is your first job, you will be required to generate UAN. This is a one-time process which can be completed by furnishing documents such as bank details, ID proof, address proof, PAN, and Aadhar.

To activate UAN, members need to follow the steps mentioned below:

Step 1: Visit the EPF website.

Step 2: Select 'For Employees' under the services section

Step 3: Click on the 'Member UAN/Online Service' option available under the services section

Step 4: Click on 'Activate UAN'

Step 5: Enter the details, including UAN, Member ID, Aadhaar number, Date of birth, and Mobile number

Step 6: Request for the authorization PIN

Step 7: Validate the OTP received on your registered mobile number and activate UAN.

Step 8: Once the process is complete, you will receive a password on your mobile number to log in to the UAN member portal and access your EPF account

Note that UAN registration and activation can only be done online.

How to link Aadhaar with UAN?

The EPFO in January 2017 made it mandatory for its pensioners and subscribers to submit their Aadhaar numbers. Further, with effect from January 01, 2022 if your UAN is not linked with the Aadhaar number, your employer/establishment will not be able to deposit your monthly contribution. The important benefit of linking Aadhaar with the provident fund Unique Account Number (UAN) is that it increases transparency and makes the verification process easier.

Linking UAN with Aadhar can be done in a few easy steps either online (through EPFO member portal or UMANG app) or offline.

a) Link Aadhar with UAN - offline

Fill the Aadhar Linking Application form, you will be required to enter details such as UAN, Aadhar number, and few other personal details. You will have to attach self-attested copies of your UAN, Aadhar, and PAN card along with the form and submit it EPFO office or Common Service Centres.

b) Link Aadhar with UAN - online

Go to EPF website and under EPFO member portal and login using your UAN and password. In the 'Manage' section click on the KYC option, you will be directed to a page where you will be required to input your Aadhar number. Thereafter, you will receive an OTP on your registered mobile number and e-mail ID. On successful verification, your Aadhar will be linked with UAN.

You can also complete the process through the EPFO option under UMANG app. Enter the Aadhar details in 'Aadhar seeding' option under the 'e-KYC services' tab and validate the transaction through OTP.

How to check EPF balance online?

Yes, it can. Here are a few steps to be followed to check the EPF balance/Passbook using an UAN:

-

Step 1: Open the web page https://passbook.epfindia.gov.in/MemberPassBook/Login.jsp

-

Step 2: Enter your Universal Account Number of UAN

-

Step 3: Enter your password set for the UAN portal & fill in the captcha code

-

Step 4: Once logged in, select your EPF account number from the list

-

Step 5: The passbook with updated balances will be loaded on the page

How to check EPF balance via SMS or Missed Call

Employees can now check their EPF balance through SMS or by giving a missed call. One such way which comes in handy at times when you do not have an active internet connection is via SMS or missed calls. For this you will need to have an activated UAN number. In case you have a valid UAN, your mobile number too will be registered with the EPF department. Members registered on the UAN portal may get their details available with EPFO by giving a Missed call to 9966044425 from their registered Mobile number. If the UAN of the member is seeded with any one of the Bank A/C number, Aadhar, and PAN, the member will get details of last contribution and PF Balance.

You can also get the latest PF contribution and balance by sending an SMS at 7738299899 from registered mobile number. The facility is available in English (default), Hindi, Punjabi, Guajarati, Marathi, Kannada, Telugu, Tamil, Malayalam, and Bengali. For receiving the SMS in any of the languages other than English, first three characters of the preferred language needs to be added after UAN. For example, to receive in SMS in Hindi then SMS to be send will be 'EPFOHO UAN HIN' to 7738299899.

Steps for using the EPF mobile app:

-

Step 1: Open the mobile app - Umang - on your phone and click EPFO

-

Step 2: Click view passbook and then input your 12-digit UAN number. The system will send an OTP to the mobile number registered with the EPFO

-

Step 3: Once verified, you will be shown a screen which displays your updated EPF balance. You can also download the account statement to your device.

The Mobile App is a good and handy way to check your EPF balance on the go.

What if the company has its own PF trust, can the balance still be checked online?

Some companies run their own PF trusts - the companies deposit your PF money with these trusts for management instead of depositing it with the EPFO. Such companies are called Exempted PF Trusts. These trusts function similar to EPF and follow the same set of rules. Members can check whether their employer is an exempted establishment by visiting the services tab of the EPF portal. Employees can avail details about their PF trusts such as balance, claim status, withdrawals, etc. only through employer via a dedicated portal, salary slips, etc.

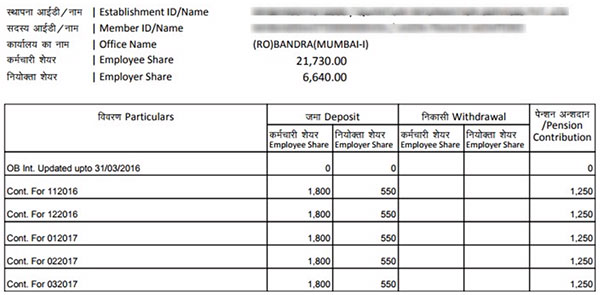

How do you read your EPF e-Passbook?

Now, as we've covered before, the employee contribution is a straight 12% into the EPF.But the employer's contribution is allocated across the EPF and the EPS. The employer also bears 3 additional costs i.e. the EDLIS, the EPF admin charges and the EDLIS admin charges.

Your EPF passbook will tell you your contribution, and also the interest earned and accrued in your EPF account. You should clearly understand the entries in this slip to ensure you are able to track your account correctly.

a) What does the account number stand for?

This will contain alphabets and numbers for example MH/BAN/0011111/000/0000111. The first two entries indicate the regional PF office in which your company contributes your money. For instance, if your company contributes in the regional EPF office at Bandra, Mumbai in Maharashtra, the entry will be MH/BAN as it shows above. The next entries which are digits will reflect the employer code and the employee account number.

b) How do you read the account balance?

Your account balance will usually have the following entries.

-

Opening balance: This is the amount you have accumulated till the beginning of a financial year. In the example above, the opening balance will indicate the fund balance at the start of the corresponding financial year (FY). This amount is further divided into two heads-employee's contribution (the amount contributed by you plus interest) and employer's contribution (the amount contributed by the employer plus interest)

-

Interest: This entry indicates the interest that has been credited to your account for the corresponding FY

-

Contributions: This shows the payments made by you and your employer in the corresponding FY

-

Withdrawals: Any partial withdrawals or advances that you may have taken

Closing balance: This is the sum of all the entries-the opening balance plus interest accrued on the opening balance and on the contributions made in the corresponding FY, plus the contributions made in the financial year. Advances you may have taken would be deducted from this kitty. This closing balance will become the opening balance for the next financial year

When can you withdraw your EPF money?

EPF being a retirement saving scheme, members cannot withdraw from the PF account during their employment. The money can be withdrawn only after retirement i.e. at the age of 58 years. EPFO allows withdrawal of 90% of the EPS corpus after they reach 54 years of age or a year before retirement/superannuation. Additionally, members can withdraw 75% of the corpus after one month of unemployment. The remaining 25% can be transferred to the new EPF account after getting new employment.

The EPF balance can be partially withdrawn before retirement on certain occasions or to meet certain specific expenses, under certain conditions, such as:

a) Education of self or children

-

Minimum 7 years of service should be completed

-

Maximum amount that can be drawn is 50% of their contribution till-date

-

Individuals can withdraw these funds only to finance education post matriculation

-

Members can withdraw balance up to 3 times for this purpose

b) Marriage of self, son/daughter, and brother/sister

-

Minimum 7 years of service should be completed

-

Maximum amount that can be drawn is 50% of their contribution till-date

-

Members can withdraw balance up to 3 times for this purpose

c) Repayment of home loan

-

The amount that can be availed for repayment of home loan will be up to 36 times of monthly basic salary + DA, or total corpus consisting of employer and employee's contribution with interest, or total outstanding principal and interest on home loan, whichever is least

-

The property should be registered in the name of the employee, spouse, or jointly owned

-

You need to have completed at least 10 years of service

-

Members can withdraw from their PF only once for this purpose and they have to submit a certificate from the agency indicating outstanding principal and interest

d) Alterations/Addition/Improvement in house

-

House should be in the name of self, spouse, or jointly owned with spouse

-

You need a minimum service of five years after the house was built/bought

-

You can also withdraw balance for alteration/repair/addition/improvement post completion of 10 years from withdrawal under point II above

-

You can draw up to 12 months' wages + DA, employee share with interest, or actual cost, whichever is least

e) Construction or purchase of house/flat/construction of house including acquisition of site

-

You should have completed at least five years of service

-

The maximum amount you can avail of is - For purchase of site: 24 month's basic wages and DA, For purchase of house/flat/construction: 36 month's basic wages and DA, or Total of employee and employer share with interest, or Total cost, whichever is least

-

You can avail of this once during your entire working life

f) Medical treatment

-

You can withdraw from your EPF for medical treatment of self or family members

-

There is no minimum service criteria in this case, furthermore you are no longer required to submit medical certificate to avail advance under this section

-

The maximum amount you can draw is 6 month's basic wages and DA, or Employee share with interest, whichever is lower

g) COVID-19 advance claim

-

In 2020 the government amended the EPF rules in view of the financial hardships faced by individuals as a result of the COVID-19 pandemic

-

Under this, employees can withdraw 75% of the member's PF contributions, or a sum of their 3 months' wages (Basic + DA), whichever is lower

-

This facility will be available till the pandemic prevails. Furthermore, this facility can be claimed irrespective of the advances availed earlier.

How to add nominee for your EPF account

The EPFO has introduced e-nomination facility for the smooth transfer of benefits to the nominees on the demise of the account holder. The nominee can be family members viz. spouse and children; and you can opt to nominate more than one family member. Filing e-nomination is beneficial as it will result in speedy and paperless payment of EPF corpus, pension, and insurance.

In the absence of nomination, the PF amount is paid to the family members in equal shares. If there is no eligible family member, it is payable to person(s) who are legally entitled to it. In the absence of valid nomination and no family, the pension amount is payable to parents (dependent father followed by dependent mother). An unmarried person can nominate somebody outside of the family. However, once married the said nomination will be treated as invalid and the benefits will be paid to the spouse and children, if any.

Here are the steps to file e-nomination:

Step 1: Visit the Employees' Provident Fund Organisation (EPFO) - website and log in to your account using UAN and password

Step 2: Go to the 'Manage' tab and click e-nomination

Step 3: A tab to provide details appears. Click 'yes' to update the family details

Step 4: Click on 'Add Family Details' and enter the required information such as name, Aadhar number, date of birth, gender, address, bank account details, and photo. You can add more than one nominee as well as the percentage share for each of them

Step 5: Click 'save EPF nomination'

Step 6: Complete the 'e-sign' process using Aadhaar based authentication

Your nomination is registered on the EPF portal.

How to transfer your EPF account when changing jobs?

When you switch jobs, it is important to ensure that you transfer your PF account to your new employer. This can be done by duly submitting Form 13(R). You can also submit claim for transfer online using EPFO's member portal. An individual is required to be enrolled as a member under the new establishment/organisation for transferring his/her PF from his previous account. The UAN has made it simple to track and transfer your funds when you move from one organisation to another at any point of time as it enables linking of multiple EPF accounts (Member ID) allotted to a single member.

Benefits of transferring PF with change in employment/job

-

Transferring the PF amount instead of withdrawing it gives members the benefit of compounding of funds. This enables them to build sizeable savings to lead a comfortable retired life.

-

A service of more than 10 years makes the member eligible for pensionary benefits. Transfer of PF account ensures that the past services does not get lapsed and continues to get added in the subsequent employment.

PF transfer lets the past service transferred into the current member ID. If the total service is more than 5 years then TDS is not charged on PF withdrawal. Clubbing of past service may help the member in crossing the 5-year mark thus saving on TDS.

For online transfer of PF account, members have to ensure the following:

-

Employee should have an active UAN and the mobile number used for activation should also be active as an OTP will be sent to this number

-

Aadhar number and bank account of the employee should have been seeded against the UAN

-

The date of exit for the previous employment must be entered

-

The employer should have approved the e-KYC

-

Only one transfer request against the previous member ID can be accepted

-

Personal details reflecting under the 'Member profile' must be verified and confirmed before applying

Members can check if the PF amount has been transferred from the previous member IDs to the current member ID. To do this, members have to log in to the EPF portal and go to 'view passbook'. After login members can view the passbook of all his/her member IDs. If the PF has been transferred then the same will be shown as a credit entry in the latest passbook, otherwise all the passbooks of the previous member IDs will show some balance. In such a case, the member is required to submit online transfer claim.

Below is the process to transfer PF online:

Step 1: Login to EPF member portal using your UAN and password

Step 2: Click on 'One Member - One EPF (Transfer request) under online services

Step 3: Verify personal information and PF account for present employment

Step 4: Select details of previous accounts (which are to be transferred). PF account details of previous employment will appear on clicking 'Get Details'.

Step 5: You have the option of choosing either your previous employer or current employer for attesting the claim form based on availability of authorised signatory holding DSC. Choose either of the employers and provide member ID/UAN.

Step 6: Click on 'Get OTP' to get OTP on the registered mobile number. Enter the OTP and click submit

Members can track the status of online transfer claim by going to the 'online services' tab of the member portal. Once the claim is submitted the status is shown as 'Pending with the employer'. When the employer approves transfer request, the status changes to 'Accepted by the employer. Pending at field office'.

It is important to note that in the case of a member whose UAN is seeded and is fully KYC compliant need not file any transfer claim on change of employment. In such a case whenever an employee joins a new organisation and the first month's contribution is received then a transfer auto trigger is generated. Soon after, the member's past PF amount get automatically transferred into his new account. This automatic transfer gets through unless it is actively stopped by the member.

Would I be able to claim interest on inoperative EPF account?

An EPF account is classified as inoperative if no contribution has been received for three years after retirement, or permanent migration abroad, or in case of death. As per the current EPFO rules, all accounts will earn interest till the member attains the age of 58 years. The account will turn inoperative only after reaching that age.

If your account has become inoperative and if your still working in an establishment covered under the EPF & MP Act, 1952, you should get the amount transferred to your new account, either online or offline. If you have retired, then you can withdraw the amount.

Is interest on EPF contribution taxable?

Interest earned is exempt from Income Tax. However, the government in its Union Budget 2021 announced that interest on contributions made towards EPF of an employee only remains tax-free for contributions of up to Rs 2.5 lakh a year. The interest earned on contribution of over Rs 2.5 lakh is taxed from the employee yearly. The contribution threshold is Rs 5 lakh if the employer does not contribute towards the EPF of an employee. Employers have to mandatorily provide EPF contributions for employees whose monthly income is under Rs 15,000. Notably, only the excess contribution above the threshold limit is taxed and not the total contribution. Furthermore, employer's contribution to Provident Fund (PF), NPS, and superannuation aggregating to a total sum of ₹ 7.5 lakh a year is exempt from taxes.

What if you need more clarity regarding your EPF including on withdrawal, transfer etc?

EPF usually takes up to 20 days to settle a claim. If the claim is not settled within the said time frame, you have two options.

a) Grievance Redressal: The EPF Organisation has a grievance redressal mechanism in place and it is covered under the Consumer Protection Act. The process of registering your grievance involves logging on to the website epfigms.gov.in/ and click Register Grievance. This is the website for the EPF I Grievance Management System. Since late last year, the EPFO has become a part of the Centralised Public Grievances Redressal and Monitoring System, which allows you to register the grievances and track their status online. It is a centralised system, so all your complaints are also monitored by the head office and they endeavour to respond to all grievances within 30 days.

They settle grievances related to the following:

-

Final settlement / withdrawal of PF

-

Transfer of PF accumulations

-

Scheme Certificate

-

Issue of PF slip / PF Balance

-

Payment of Insurance Benefit

-

Cheque Returned / Misplaced

-

Others, for a grievance that is other than the ones listed above.

b) Right to Information

What is the grievance handling mechanism in the EPFO?

There is two-tier organizational structure of customer Service Division for handling and redressal of public grievances.

At the Head Office level, this division is headed by Additional Central Provident Fund Commissioner and assisted by Regional Provident Fund Commissioner, Assistant Provident Fund Commissioner and Public Relation Officer.

The Regional Provident Fund Commissioner of the regions and Officer-in-Charge of Sub-Regional Offices head the Customer Service Division in their respective offices and they are available for redressal of the grievance of the members on all working days. Each field office has a full-fledged facilitation centre and is manned by a Public Relation Officer. Apart from this, all Zonal Additional central Provident Fund Commissioners in the country monitor the grievance handling system and attend grievances.

'Nidhi Aapke Nikat' (PF Near You) is a new form and structure of Grievance Redressal mechanism is being held in all the offices of EPFO on 10th of each month across all the field offices of EPFO. This programme is a new initiative on the part of the EPFO to be more broad-based in its approach towards its stakeholders. This serves as an occasion for employers and employees to air their views and opinions regarding the organisation and provide actionable feedback.

Since launch of 'Nidhi Aapke Nikat', has witnessed active participation of around 2,000 employers and more than 3,000 employees. You can be a part of this forum too and voice your concerns to help them improve on the services that they are currently offering to you.

You can even reach out to the EPFO with your grievances through the social media. EPFO has debuted on Facebook (www.facebook.com/socialepfo) and Twitter (www.twitter.com/socialepfo) where you can raise your queries.

The government has also launched an online public grievance handling mechanism-EPFiGMS (Employees Provident Fund Internet Grievance Management System). Any grievances received from any source and through any mode (by e-mail/post/reference from any source) are registered by the office in EPFiGMS (Employees Provident Fund Internet Grievance Management System).

By using this system anybody with a grievance can register his grievance 24x7. Once registered a unique number is allotted to help keep track of the progress of the grievance redressal. Every grievance entered into the EPFiGMS system is monitored on a daily basis, both at the Head office level and the Field office level.

The grievances raised are of the following nature:

-

Settlement of PF/Pension/Insurance Claims

-

Transfer of PF accounts

-

Non enrolment of employees

-

Difficulty arising out of old PF accounts

-

Difficulties relating to Universal Accounts Number (UAN).

Grievances are raised by employers or employees directly. In addition grievances are also referred to by the office of Hon'ble Prime Minister, Hon'ble Minister of Labour & Employment, Cabinet Secretariat, MPs, MLAs, other VIPs and Department of Personnel and Grievances (DPG)

The EPFO have issued strict timelines to ensure that improvements in grievance redressal are undertaken. Moreover, monitoring is done on a continuous basis and pending grievances are escalated to higher levels depending upon the periodicity of pendency.

If the Grievance Redressal Management doesn't work, the RTI can come to your rescue. Filing an RTI. You can visit the website www.rtionline.gov.in/index.php to raise an RTI query. If you are a first time user, make sure to register yourself by filling in the required fields to generate a username and password.

Once you register, you would be able to raise a query by using your username and password and paying the requisite fees.

Conclusion: From a Financial Planning perspective...

For a salaried person, contributions to the EPF offer a lot of benefits:

a) Safe returns: This is one of the safest debt instruments available in the country. It is government backed and guarantees safety of principal and interest earned. It can help you accumulate a significant corpus for your retirement, as the contributions happen month on month for your entire working life. This makes it suitable for very long term financial goals.

b) Friendly tax treatment: This is an E-E-E instrument - meaning your contributions are deductible under Section 80C, interest earned is tax free and maturity proceeds are also tax free, provided contributions to the fund have been for more than 5 years of service.

c) Interest earned on EPF is the equivalent of a high pre tax rate: The EPF is paying 8.1% this year, this is much higher than other taxable fixed income investments. In addition, the interest rate is guaranteed and risk-free.

Apart from the main features, it also allows withdrawals as detailed in an earlier question and you can also avail a loan against your EPF, using it as security.

However, keep in mind; this is a very long-term instrument. If you have short term financial goals, don't try to fund it by withdrawals from your EPF. If your goals are in fact primarily short term, as is the case with young couples, or parents funding their children's educations in a few years, you might want to consider only investing the minimum amount in your EPF, and channelizing your remaining funds towards a more liquid instrument, keeping your risk appetite and goal time horizon in mind.

The EPF must not be viewed as a standalone retirement product. With growing inflation and everyday expenses, you simply cannot depend on your EPF corpus for retirement. Hence, there is a need to build your retirement corpus through other wealth creating products.

The biggest advantage of investing in EPF and/or PPF has been their favourable tax status. Investors get tax benefits on the amount they deposit and the amount they withdraw along with tax-free interest that accrues on their investments. However, the interest rate earned, though tax-free, may not be sufficient to build a sustainable retirement corpus.

EPF or PPF can be one of the options you may consider when building a retirement fund. This will create a debt-exposure in your portfolio. But when building your retirement portfolio, allocate proportionally to other asset classes such as equity. Our research indicates investing in equity is known to have generated high inflation-adjusted returns leading to long-term wealth creation.

Planning for retirement can keep you financially independent even during your golden years.

When you are retired, this will supplement your income to take care of day-to-day expenses and any medical emergencies. It is important to have a comprehensive retirement amount in mind that you need to live comfortably in the second innings of your life. To arrive at a hypothetical corpus amount, you must thoughtfully consider certain estimations and presumptions.

Use our simple Retirement Calculator here, to estimate the corpus you require at the time of retirement. In addition to this, you can calculate the investment amount needed to achieve this retirement goal. Our comprehensive Retirement Calculator is simple to use and will make an accurate estimate of your retirement needs. You can then create a financial plan based on this calculated information to create your nest egg.

The right mix of assets and a disciplined investment approach will help you build your retirement savings.

Unbiased financial knowledge is the key to succeed in achieving all your investment goals before and after retirement.

Warm Regards,

Divya Grover

Research Analyst