Do Mutual Funds Protect their Investors?

Apr 15, 2024

Author: Ajit Dayal

The ICICI Bank / ISEC delisting, and swap ratio is a violation and failure of governance on multiple fronts as explained in my earlier column but it is also a test case for the claims of a very successful market positioning of AMFI: 'mutual fund sahi hai'.

It should be noted that AMFI is an association of manufacturers of mutual fund houses - and not an association of mutual fund investors. Furthermore, Quantum AMC - which I am affiliated with - is required by law to be a part of AMFI though, as many of you are aware, many of the standard operating practices of the AMFI members were shunned by Quantum AMC as we felt these were either unethical or immoral practices. Two examples come to my mind:

(1) paying opaque distribution commissions to intermediaries for gathering AuM from many unsuspecting investors, and

(2) handing over to distributors the exit loads when investors redeemed from a scheme rather than ploughing back that money to each scheme.

Here is a list of Quantum Firsts which SEBI etched into law and AMFI had little choice but to follow the 'sahi' path.

Always putting investors first, even above our growth in AUM

|

Quantum Mutual Fund |

SEBI Imposes Rule on MF Industry |

| Refused to follow the opaque Entry Load Model |

Mar 2006 |

Jun 2009 |

| Pioneered Direct to Investor, despite Slow Internet Speed and No Smart Phones |

Mar 2006 |

Jan 2013 |

| One Scheme / product per asset class |

Mar 2006 |

Oct 2017 |

| Exit Load swept into funds for the benefit of Unit Holders |

Mar 2006 |

Nov 2012 |

| Single Plan with Single Expense Structure for Retail and Institutional Investors |

Mar 2006 |

Sep 2012 |

| Introduced the practice of following Total Return Index (TRI) as benchmark for Equity Fund |

Mar 2006 |

Jan 2018 |

| Path to Profit (Investor Education & Awareness Program) |

Aug 2009 |

Sep 2012 |

| 100% Independent Board of Trustees |

Oct 2010 |

? |

| Mark to Market valuation in Liquid Fund, irrespective of the maturity |

Jul 2012 |

April 2020 |

| TER based on AUM Slabs |

Feb 2017 |

April 2019 |

| Introduction of SMILE Facility - Donation to NGOs |

Mar 2017 |

- |

| ZERO Upfront Distributor Commission and uniform trail commission across all partners on Regular Plan |

Apr 2017 |

Sep 2018 |

Some may argue that morality and ethics are subjective and a 'personal view'.

So be it - let's see how the actions of mutual funds stands up to scrutiny on a monetary basis.

The ICICI Bank / ISEC delisting, and swap ratio is a good litmus test to see whether mutual funds have their investor's interests at heart.

Mutual Funds are a phenomenal vehicle.

Before we jump into that analysis, a few quick points:

-

I believe mutual funds are a fantastic vehicle for millions of retail investors,

-

Mutual fund regulations and structures set up by SEBI over the past three decades have ensured that the vehicle and structure of a Trust which has a scheme for every product or style of investing, with a Board of Trustees to ensure that the beneficiaries, the unit owners always control and own the assets in a 'scheme'. (I must admit, though, that I dislike the word 'scheme' as it reminds me of the negative connotation of 'scheming' or planning to cheat.)

-

SEBI continues to monitor the mutual fund industry for froth and the recent directive by SEBI to AMFI to ensure that there is a stress test disclosure for small cap funds is a case in point. What AMFI has done with that SEBI directive is material for a future column.

-

The biggest financial win for Prime Minister Modi is not that the stock market Index has surged - that is a mathematical formula. PM Modi's single-handed win is that tens of millions of investors have been inspired by his India Shining statements and have rushed headlong into mutual funds. More than the cute 'mutual fund sahi hai' slogan of AMFI, it is the 24x7 energy of Prime Minister Modi that has inspired millions to participate in Superpower India.

Hence, any loss of faith in mutual funds by India's growing population of mutual fund investors because of lax oversight by the fund houses should be seen as a debasing of that spectacular achievement of Prime Minister Modi.

The size of the damage.

To recap from an earlier article on the unfair swap ratio accepted by the Board of ISEC and canvassed for by an army of ICICI Bank representatives that:

-

In a nutshell, the minority shareholders own 81.7 million shares of ISEC, about 25%;

-

ICICI Bank values ISEC at Rs 722 per share based on a swap ratio of 1 share of ISEC = 0.67 shares of ICICI Bank;

-

If ISEC was valued the same way as Angel One, a listed company in the same lines of business as ISEC, the price of the ICICI Bank offer to ISEC minority shareholders should be Rs 940 per share - an increase of 30%.

-

If ISEC was valued the same way as 360 ONE, a listed company in the same line of business as ISEC, then the price of the ICICI Bank offer to minority shareholders should be Rs 1,576 per share - an increase of 118%.

| Table 1: Loss to Minority Shareholders from a Suppressed Swapped Ratio |

|

A.

ISEC Derived share price based on Swap Ratio proposed by ICICI Bank and approved by the ISEC Board (INR per share) |

722 |

|

|

B.

ISEC derived share price if valued at 20.4x FY24E Earnings (lowest multiple for peer Angel One) (INR per share) |

940 |

| Loss at current swap ratio (INR per share) |

218 |

| Total number of minority shares in the issue |

81,700,393 |

| Total loss for ISEC Minority shareholders, INR million |

17,811 |

|

|

C.

ISEC derived share price if valued at 34.2x FY24E Earnings (360 ONE peer valuation) (INR per share) |

1,576 |

| Loss at current swap ratio (INR per share) |

854 |

| Total No of minority shares in issue in Millions |

81,700,393 |

| Total loss for ISEC Minority shareholders (INR million) |

69,772 |

Source: Calculations are based on closing prices of Angel One and 360 ONE on March 11, 2024

Note that this is a zero sum game; like playing teen-patti with your friends: what one person loses, another gains.

The loss to minority shareholders of ISEC results in a gain to the shareholders of ICICI Bank.

By not using the 360 ONE valuation, ISEC is undervalued by Rs 69,772 million (Rs 6,977 crore) this means that ICICI Bank bought the company at a lower price and they stand to gain to the extent of Rs 69,772 million.

Keeping this zero-sum game concept in mind, lets see how the mutual fund houses - on a collective scheme basis, adding up all their holdings across each scheme, did.

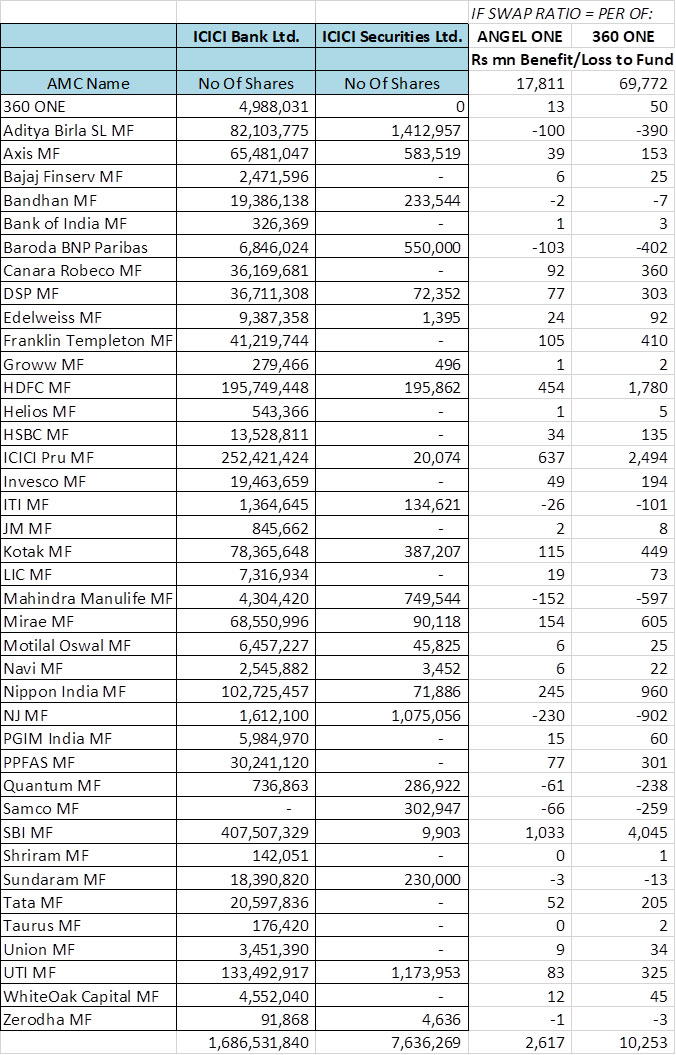

Table 2: What was the benefit or loss to each fund house, on a collective basis, from the fact that the ISEC swap ratio was valued (a) Less than Angel ONE, or (b) Less than 360 ONE? (In Rs Millions)

Holdings as of February 29, 2024

Holdings as of February 29, 2024

Source: ACE MF

As an illustration, let's look at the data for SBI Mutual Fund.

From a Fund House perspective, based on the data in Table 2 above as of February 2024, SBI Mutual Fund had 407,507,329 shares of ICICI Bank and 9,903 shares of ISEC across ALL its mutual fund schemes.

By ensuring that the swap ratio valued ISEC at Rs 722 per share and that the valuation of ISEC was not based on the valuation of Angel ONE, SBI MF - for all its schemes collectively - stands to benefit to the extent of Rs 1,033 million from the undervaluation of ISEC.

By ensuring that the swap ratio valued ISEC at Rs 722 per share and that the valuation of ISEC was not based on the valuation of 360 ONE, SBI MF - for all its schemes collectively - stands to benefit to the extent of Rs 4,045 million from the undervaluation of ISEC.

Note that this calculation is for SBI MF as a fund house - as if it is one master fund.

It is not.

Each scheme has its own gain / loss equation.

In the case of SBI, its Nifty MidCap Index fund owned 9,903 shares suggesting that the loss to this scheme was Rs 22 lakh (using Angel ONE as a benchmark of fair value of ISEC) or Rs 84 lakh (using 360 ONE as a benchmark of fair value of ISEC).

To prevent any loss to its investors, this scheme should have voted against the swap ratio for the delisting. Did it?

The cut-off date for voting was March 20, 2024: only those who owned shares as of March 20, 2024, were eligible to vote.

The databases available in the public domain give portfolio holdings of mutual funds at the end of every month, not on a random interim date of the month.

To make good the faith that investors have placed in the mutual funds to ride the Superpower India theme as espoused by Prime Minister Modi, it will be in the public interest for AMFI to:

-

List the number of shares held by every individual scheme of every mutual fund house that:

(a) only held shares of ISEC as of March 20, 2024, and reveal how they voted;

(b) held shares of both ISEC and ICICI Bank as of March 20, 2024, and reveal how they voted.

SEBI, as a regulator, has built a complex and expensive structure of guardrails and responsibilities around a mutual fund house.

The Fund Managers must be qualified with degrees and have exhibited demonstrated ability to make investment decisions. It will be interesting to see how many of them used simple multiplication and subtraction to arrive at the 'net benefit or loss from ISEC undervaluation' to the schemes that they manage. And if that was reflected in the vote? Or if there was a legitimate belief that ISEC was not undervalued by the low-balled ratio proposed by ICICI Bank as I have proposed in Table 1 above, what is their justification for that view?

One can also inquire if there was another reason for the inspired voting in favour of the delisting by mutual funds.

ICIC Bank has claimed in its explanation to the stock exchange that individual shareholders received calls from representatives of ICICI Bank to encourage the ISEC shareholders to participate in the vote as a step to 'democratise' the voting process. A very noble thought. The equivalent of sending trucks to transport individuals to the poll booth - something frowned upon by the Election Commission of India.

AMFI should get a statement from every fund house whether the CEOs, CIOs, or fund managers received phone calls from representatives of ICICI Bank. Or - as in our vibrant democracy - the rich take off for vacations when it is time to vote!

In summary, the ISEC saga has thrown open a can of worms of corporate mis-governance at multiple levels.

One hopes that AMFI will release the necessary data as of March 20, 2024 along with the voting patterns of each scheme to put to rest the fears that mutual funds are not as ‘sahi’ as they are advertised to be.

(Note: Quantum Mutual Fund, which I am affiliated with, has sent the following communication to relevant parties involved in the ICICI Bank / ISEC delisting saga.)

https://www.quantumamc.com/downloads/pdfs/2024/Final-Letter-ICICI-ISEC.pdf