How the Proposed Systematic Lumpsum Withdrawal Option Can Benefit NPS Subscribers

Rounaq Neroy

Jun 13, 2023 / Reading Time: Approx. 7 mins

Listen to How the Proposed Systematic Lumpsum Withdrawal Option Can Benefit NPS Subscribers

00:00

00:00

To plan for one of the most important financial goals, i.e. retirement, the National Pension System (NPS) -- a government-backed scheme regulated by the PFRDA -- is one of the meaningful avenues. Systematic investments or contributions made into the NPS account during the earnings phase (also known as the wealth accumulation phase) can help one build a respectable corpus or a nest egg for retirement.

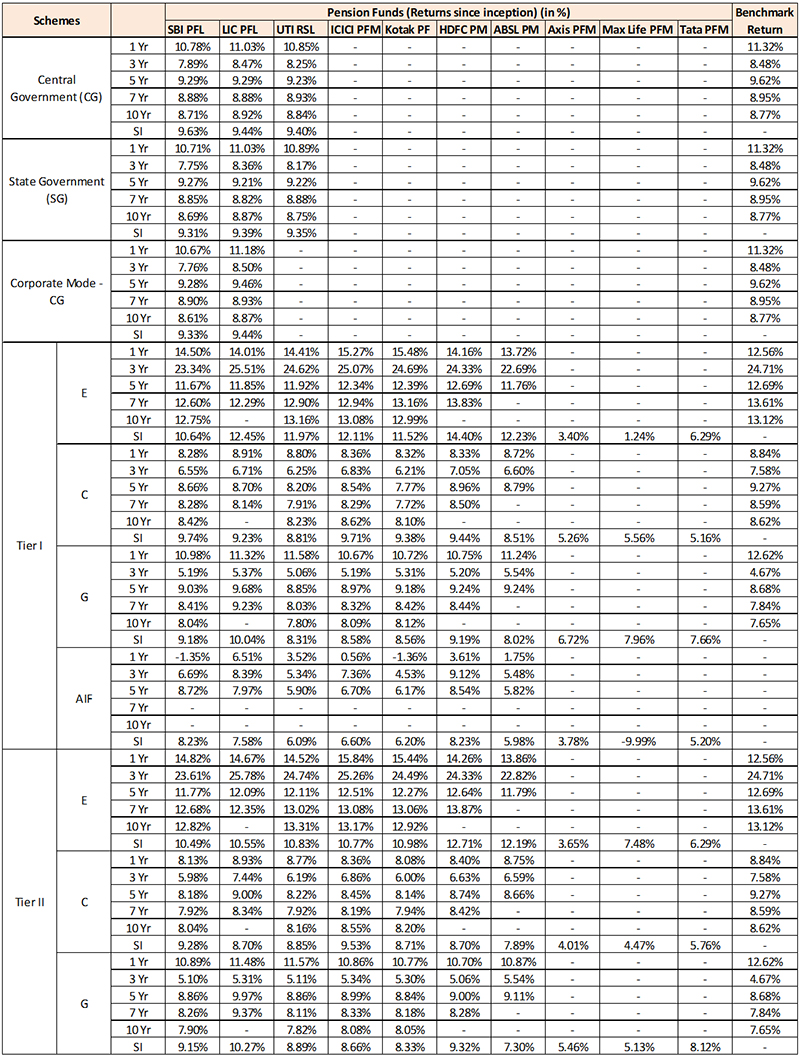

TABLE: Performance of individual NPS schemes across Pension Fund Managers (PFMs)

The table indicates returns as of June 2, 2023.

The table indicates returns as of June 2, 2023.

Past performance is not indicative of future returns.

(Source: www.npstrust.org.in)

The long-term market-linked returns clocked by the mandatory Tier I of the NPS have been impressive returns across categories -- Equities (E), Corporate Bonds (C), and Government Securities (G). The returns have been better than other comparable retirement avenues, such as the Public Provident Fund (PPF) and the Employees Provident Fund (EPF). This is, of course, abetted by the higher allocation to equities plus the fact the funds are invested dynamically between E, C, and G, as per one's age. But the NPS Trust has lived by its charter of working in the interest of its beneficiaries.

Over the years, many changes have been made in NPS seeking feedback and out of the concerns of the subscribers - be it the introduction of NPS lite, doing away with the practice of submitting a separate form to purchase an annuity, allowing partial withdrawals, the introduction of the online facility for withdrawals (with self-declaration) during the COVID-19 pandemic, to making NPS withdrawals (from Tier I account) tax-free up to 60% of the accumulated corpus and so on.

Among the recently proposed changes in the NPS is allowing the 'Systematic Lumpsum Withdrawal (SLW)' Option by the end of this quarter, according to PFRDA Chairman, Mr Deepak Mohanty who spoke to the media. The SLW Option for NPS subscribers who have attained 60 years of age, will make it possible for them to withdraw in a staggered manner monthly, quarterly, half-yearly, or annual withdrawals -- as per their choice -- until 75 years of age.

What Are the Benefits of the Proposed SLW Option?

Staggered SLWs shall provide flexibility to the NPS subscriber to withdraw out of the 60% accumulated corpus at 60 years, as per their liquidity needs, as opposed to a compulsory lumpsum as at present.

This proposal ensures that money for one's retirement continues to grow with market-linked returns (for a good 15 years after the usual retirement age) rather than applying brakes fully on the process of power of compounding (by withdrawing 60% of the corpus at one go).

With SLW, NPS subscribers could...

-

✔ Inculcate a disciplined approach to utilising the corpus built for your retirement.

-

✔ Benefit from rupee-cost averaging.

-

✔ Potentially grow their retirement nest egg.

-

✔ And may enable countering inflation.

In short, it shall help preserve wealth for retirement expenses and prove beneficial for one's long-term financial well-being.

[Read: How Retirees Can Use the SWP Option to Manage Their Cashflow Needs]

How to Avail of the SLW Option in NPS?

The NPS subscriber would be required to submit the request stating whether the SLWs will be monthly, quarterly, half-yearly or yearly, and the start date and the end date. And note, once the SLW is activated, the subscriber cannot contribute to the mandatory Tier I account.

(Image source: freepik.com; Image by Freepik)

(Image source: freepik.com; Image by Freepik)

Join Now: PersonalFN is now on Telegram. Join FREE Today to get 'Daily Wealth Letter' and Exclusive Updates on Mutual Funds

Other than the SLW Option, there are other options as well.

The subscriber could also opt to choose to defer the withdrawals (drawdowns as per one's choice) or continue to remain invested for the 60% component (as per one's financial circumstances and risk appetite). The remaining 40% component will be used to purchase the annuity, clarified Mr Mohanty speaking to the media. It should be noted that the NPS corpus that goes into buying an annuity is exempt from income tax. Moreover, Goods and Services Tax is (GST) not applicable on annuity plans purchased from the NPS corpus.

To sum up...

If you are okay with earning variable, i.e. market-linked returns taking a calculated risk, NPS is a worthy investment avenue for your retirement needs. While partial withdrawals (up to 25% of the self-contribution) are tax-free and the annuity purchased will be fully exempt from tax, the pension you receive out of the annuity purchased will be treated as an income and taxed appropriately. So, NPS does not enjoy an absolute Exempt-Exempt-Exempt (E-E-E) tax status like PPF or EPF.

If a thoughtful approach is followed (by saving and investing at an early age), one can retire rich and live the golden years in bliss.

Happy Investing!

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

Disclaimer: This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.