Will India’s Widening Fiscal Deficit Upset Indian Debt Market?

Listen to Will India’s Widening Fiscal Deficit Upset Indian Debt Market?

00:00

00:00

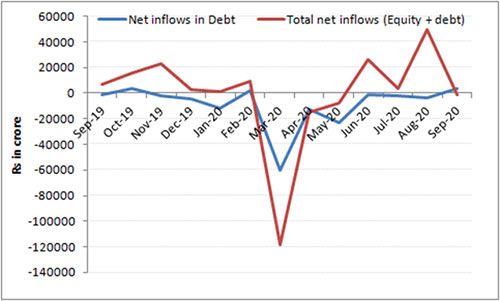

The Coronavirus pandemic has not augured well for Indian debt markets; they seem to have lost the appeal. Barring the month of September, the Foreign Portfolio Investors (FPIs) have been net sellers in the Indian debt market since November last year (see graph below).

Even domestic mutual funds haven't been positively or enthusiastically participating in the Indian debt market. In fact, underwriters had to intervene in the G-sec market in August this year to ensure that sovereign issuances sail through.

Graph: FPI don't look impressed with India debt markets

Data as of September 30, 2020

Data as of September 30, 2020

(Source: NSDL)

What are the possible reasons for poor participation in the Indian debt markets? Is it solely because interest rates are falling and now are at multi-year lows for sovereign and AAA-rated instruments?

Well, there are a variety of factors...

Debt markets are upset primarily because of five factors:

-

India's rising debt (currently nearly 70% of GDP)

-

The full-year borrowing program kept unchanged at Rs 12 lakh crore by the government (which could potentially push India's fiscal deficit over 8% of GDP as against the target of 3.5% outlined in the Union Budget)

-

The fiscal deficit has already widened in the first five months through the fiscal year (touched 109% of the full-year budgeted estimate of Rs 7.96 lakh cr)

-

CPI inflation moving beyond RBI upper tolerance limit for nine consecutive months

-

The worst GDP growth contraction reported by India in four decades

The COVID-19 pandemic, as we all know, has dented government finances.

(Image source: unsplash.com; photo courtesy- Ehud Neuhaus)

(Image source: unsplash.com; photo courtesy- Ehud Neuhaus)

Against the planned borrowings of Rs 7.66 lakh crore in H1FY21, the government's actual borrowings shot up to Rs 7.7 lakh crore in the H1FY21.

The government recently clarified that its full-year borrowing target stands unchanged at Rs 12 lakh crore. In other words, it means, it aims to borrow Rs 4.3 lakh core in H2FY21. This might offer some immediate relief to the bond markets, as can be seen in FIIs turning net buyers in September. But, the question is, can the government make much progress on its revenue targets to get anywhere near to its fiscal deficit target of 3.5%.

With phase-wise unlocking, although the tax collections are improving, on an aggregate basis for the period April to August 2020, GST collections are 30% lower (at Rs 3.6 lakh crore) when compared to the same period in the last fiscal year.

Direct tax collections have not been encouraging either. In Q1FY21 India's net direct tax collections fell 32% to Rs 92,681 crore vis-a-vis Rs 1.37 lakh crore recorded a year ago.

Speaking of disinvestments, the Department of Economic Affair Secretary, Mr Tarun Bajaj recently acknowledged that (the ambitious) disinvestment target of Rs 2.1 lakh crore will not be met in the current fiscal year, as the government has no plan to increase its borrowing (above Rs 12 lakh crore) or go for deficit monetisation. So far, the government has been able to raise only Rs 20,000 crore as disinvestment receipts. And looking at the sharp -23.9% GDP growth contraction in Q1FY21 and slower recovery in the ensuing quarter amid the pandemic, the government may not even reach the halfway mark of the disinvestment target.

With lower tax revenues (both direct and indirect) than last year and falling far short on disinvestments, controlling the fiscal deficit would be a herculean task for the Modi-led-NDA government. Some independent rating agencies have estimated India's fiscal deficit to settle in the range of 6%-8% by the end of FY21 vis-a-vis the target of 3.5% set in the Union Budget 2020.

Taking cognisance of a host of macroeconomic indicators, international credit rating agencies have downgraded India near the junk and have forecasted a negative outlook -- owing to structural issues that could impede economic progress and negatively affect government's fiscal position.

On this backdrop, fall in yields driven by RBI's unprecedented policy action in the wake of coronavirus pandemic has affected the demand for Indian debt papers.

At present, the proactive measures (conventional and unconventional) taken by the RBI to maintain the stability in the financial system via liquidity has kept the 5.79% 10-year G-Sec yield anchored around 6.00%.

The RBI appears reluctant to increase rates to contain CPI inflation, which has crawled over 6.00% for nine consecutive months. In the last bi-monthly monetary policy statement for 2020-21, a status quo was maintained on policy rates (after a 250 basis reduction since February 2019), but the stance of the policy was kept accommodative as long as it is necessary to revive growth and mitigate the impact of COVID-19 on the economy. The RBI preferred to adopt a wait-and-watch the incoming macroeconomic data.

How would debt mutual funds fare?

At present, the credit environment has turned hostile amid the pandemic. The chances of credit rating downgrades appear higher than the upgrades for FY21. The investment risk has certainly intensified.

Papers with high credit quality are quoting at yields which are unattractive to international as well as Indian investors. While certain debt fund managers have been engaging in yield hunting to clock a higher rate of return and lure investors, do keep in mind that this activity attracts high risk as well.

When you choose a debt mutual fund scheme for your portfolio, pay attention to your risk profile and investment time horizon.

Also, analyse debt mutual fund scheme on the following factors:

-

✓ The portfolio traits and sectoral allocations

-

✓ Maturity profile

-

✓ AUM and the expense ratio of the scheme

-

✓ Returns and risk ratios

-

✓ Interest rate cycle

-

✓ Track record of the fund house and processes and systems followed by it

Given the challenging credit environment prevailing at present, you may invest in debt funds that predominantly invest in securities issued by the Government of India or PSU debt papers.

For investment time horizons longer than a year, consider Banking & PSU Debt Funds that allocates 85-90% of its assets in instruments issued by major Banks and PSUs. In the current scenario, it would be imprudent to invest in debt mutual fund schemes whose underlying portfolios are compromised with low rated papers of private issuers.

For an investment horizon of less than a year, a liquid fund would be a befitting choice for the safety and liquidity of your principal. Considering that the interest rate cycle has almost bottomed out, shorter duration funds look better from a risk-return standpoint.

Our friends at Quantum Mutual Fund have highlighted the secret behind their debt management strategy, which has helped them provide safety and liquidity to investors when it comes to investing in Quantum funds. Don't Worry, Quantum Liquid Fund always aims for Safety and Liquidity.

Alternatively, if you prefer to keep your capital safe, opt for bank fixed deposits, but choose the bank carefully.

Happy Investing!

Warm Regards,

Rounaq Neroy

Editor, Daily Wealth Letter

PS: If you wish to select worthy mutual fund schemes, I recommend subscribing to PersonalFN's unbiased premium research service, FundSelect.

Additionally, as a bonus, you get access to PersonalFN's popular debt mutual fund service, DebtSelect.

Each fund recommended under FundSelect goes through our stringent process, where they are tested on both quantitative as well as qualitative parameters.

Every month, PersonalFN's FundSelect service will provide you with insightful and practical guidance on equity mutual funds and debt schemes - the ones to Buy, Hold, or Sell.

If you are serious about investing in a rewarding mutual fund scheme, Subscribe now!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds