Everything You Need To Know About Financial Planning

Many may wonder - "Do I really need a financial plan?"

Some feel that saving regularly in bank recurring deposits or Systematic Investment Plans (SIPs) in mutual funds is financial planning.

But allocating savings and investments in ad hoc manner is not enough to achieve your life goals. And such investments lead to inefficient utilisation of your financial resources.

To become rich or to achieve all your goals such as buying a house, car, dream vacation, child's education and so on you need to make money work for you. Besides salary or business income might not be sufficient enough.

This is where financial planning comes to your rescue.

A financial plan enables you to construct a road map to achieve all the financial goals. It also helps you build your contingency fund for any unforeseen needs that may arise.

Let us first begin with understanding what a financial plan is and what it can do for you.

Chapter 1: What is Financial Planning?

Financial planning is a holistic exercise to evaluate your current and future financial standing and thereby enabling you to achieve all your goals in a systematic manner.

As mentioned before, it creates a road-map and equips you to meet all your life's expenses – both the expected and unexpected.

Financial planning includes budgeting your expenses, investing in right assets, setting SMART goals, selecting right asset allocation, creating a retirement plan and more.

You would wonder why you need a financial plan when you have enough savings.

If you are earning, your monthly income you can cover your expenses, and whatever you save you will invest for your future needs. Hopefully, you will have enough set aside to live the rest of your life maintaining a good lifestyle.

But we all know that inflation can be the biggest bug. It has the power to eat away the value of your hard-earned money.

Inflation is general rise in price of goods and services over a period.

Something that costs you Rs. 100 today, could cost you Rs. 110 tomorrow. Imagine what it

would cost you when you retire in so many years.

An example to bring out the point:

Current Monthly Household Expense: Rs. 30,000

Years to Retirement: 15

Inflation Rate: 8% p.a.

Future Household Expense (post retirement): Rs. 95,165 per month

And to fight inflation you need a prudent investment plan.

Financial Planning involves planning for your life goals such as your own retirement, your child's

education and marriage, purchase of house, car, annual family vacations and any other goals.

While creating a financial plan your planner will first quantify all your goals. He/she will then asses your cash flows. And then the plan to allocate your funds towards these goals in a systematic manner so that they can be achieved.

After considering your personal financial requirements a Once a plan has been created by taking all your personal financial requirements into account, then you would begin investing towards the goals.

The recommendations for investments are the last piece to fit into the financial plan. These

recommendations may also include tax saving investments.

Before you start your financial planning journey with a financial planner you can learn some basics.

Let us look at some of the basics of Financial Planning:

-

Defining Financial Goals:

The primary objective of financial planning is to help you achieve your financial goals.

Start by listing them down into short term (up to 2 years), medium term (from 2 to 5 years), and long term (above 5 years).

Make sure your financial goals are: Specific, Measurable, Adjustable, Realistic and Time Bound (S.M.A.R.T).

-

Start with a budget:

Budgeting is the process of creating a balanced formula on how to make optimal use of your hard-earned money.

Simply put, a budget is an itemised summary of the anticipated income and expenses for a given period, say a month. It will help you keep your expenses in check and keep you out of debt.

Although there are plenty of free budgeting software and apps available online, you could just start with a pen and paper or an MS-Excel sheet to get a hang of the exercise.

-

Keep a contingency reserve:

An essential component of a solid financial plan is creating an emergency fund (also called a contingency fund).

As you know, life is uncertain and emergencies such as loss of job, hospitalisation of family member, loss of assets, etc. can occur at anytime.

Ideally a contingency fund is nothing, but 6 months of monthly living expenses saved. This includes everything from household expenses, to EMI payments, or any other expenses you may incur during a regular month.

Therefore, an intelligent approach would be to put away a portion of one's savings to counter these exigencies if/when they arise.

-

Asset Allocation is the key:

Asset allocation is the foundation of financial planning.

A right mix of equity and debt will help you achieve your financial goals in the time horizon you planned. As you may have read in earlier articles, a common rule of thumb used to decide the proportion of equity in an asset allocation is 100 minus your age (100 – x years).

The rationale behind this rule is: the older you get, less time you have to recover if the stock market tumbles and your risk appetite recedes as well.

At the same time investing too less in equities could slow down your portfolio growth. Making it incapable to keep pace with inflation.

Although this isn't the optimal approach to structure one's asset allocation, it could be a good starting point for beginners in the investment arena.

-

Review your financial plan regularly

A regular review of financial plan increases the possibility of fulfilling goals.

This helps you to incorporate personal or economic changes if any.

It helps keep a check on whether these investments will help you in achieving the targeted goals.

For example, if you have invested in equities, then it would be prudent to check the current standing from time to time. It could be possible that a stock or equity mutual fund may be underperforming.

Or in case of an equity mutual fund scheme, there could be a change in its investment objective or style, which no longer meets your purpose of investment.

Hence, review your plan regularly and weed out investments which no longer adds value to your portfolio.

Chapter 2: Who Needs A Financial Plan?

For your convenience, we have made a list of scenarios where financial planning might come to your aid. These points will help you determine whether you need to create a financial plan for yourself or not.

A financial plan is required if:

- You don't realise where and how your income is spent every month, then you definitely need to plan your finances better.

In today's era of consumerism, many fail to understand how their monthly salaries get extinguished. Leaving them with very little or absolutely nothing to save.

Impulsive buying and lack of budgeting for expenses, leads to problems in the long run. with not having saved for taking care of children's future needs or even one's retirement.

Thus, not keeping track of your expenses and being carefree leads you to bid a goodbye to your long term financial goals, while you may achieve all the fancies of life in the short run.

- When you have various liabilities and just don't know how to get out of the debt trap, it's time you put your personal finances in order.

In today's world, each of us want a better lifestyle than what we presently enjoy; a lifestyle that gives us more comfort and advantages.

And at times to fulfil these we end up borrowing money and taking loans. But mind you these easy finance options can result into damaging your financial health.

A financial plan will not only help you to come out of this mess but will also enable you to manage your cash flows better. And to live a debt free life as far as possible.

- If you don't have road map of how to achieve your dreams, a financial plan can be your blue print to meet all your financial goals.

Financial Plan gives a shape and form to your goals.

It is for those who have unclear ideas or plans of how they would achieve their dreams and wishes in life.

- If your investments are scattered and you are yourself unsure about where you have invested, then it's high time for you to put your portfolio in order.

Many often indulge in investing in a haphazard manner without conducting a proper need-based analysis or undertaking sufficient research on financial products.

Managing these scattered investment gets difficult to manage / track. The investment portfolios of such investors are extremely strewn with duplicating schemes.

Also, at times there are investments which do not provide any advantage of diversification. Such investment portfolios need to be consolidated and re-aligned as per your financial needs.

- You are not sure if you have made the right investments. Many people invest in the equity asset class through shares or mutual funds.

However more often than not, as mentioned earlier, such investments are done on recommendations from friends and relatives and without taking into consideration one's financial goals and risk appetite.

At times these unplanned and non-researched investments result in loss of the investors' money.

Hence it is extremely important that you invest only after considerable research has been undertaken on any investment proposition.

Constructing a financial plan will enable you or your financial planner to review your entire portfolio. And restructure the same if required to provide you with the best possible outcomes.

- If you want to plan for financial goals such as buying your dream home, a car, a vacation abroad, child's education and their marriage needs and your retirement amongst host of others; prudent financial planning can come to your recourse.

Through experience we can say that many vie for all the aforementioned goals, but do not have a plan to achieve them.

For many procrastination is their biggest enemy. So, it is imperative that a financial plan is made. And to make your dreams come true you also need to thoroughly follow the financial plan.

- If you don't have a habit of investing systematically and regularly. You see, to create wealth in the long-term, regular investing is the key.

Even a child needs discipline and regular monitoring to achieve his goal of being a good student.

Hence, as a grown up individual you definitely need to invest regularly to meet your financial goals.

Investing small amounts regularly will also prove to be light on your wallet. Thereby enabling you to comfortably meet all your financial goals.

It might be difficult for you to determine the amount that you would need to invest regularly to meet all your goals. But a financial planner can help you plan your investments in right investment instruments to achieve your goals.

- If you have multiple life insurance policies and don't know which policies to keep. Sometimes people land up taking multiple policies such as Endowment, Money Back, ULIPs, Pension Plans etc. due to the incomplete knowledge or mis-selling of products through agents.

Many a times, these policies do not solve the purpose of the insured and only result in filling the pockets of the agent who sold you that policy.

Some policies which promise you a life cover plus returns (market linked) may fail to do both. More often than not, these policies provide a very low cover and also low returns due to the number of charges involved.

A financial planner can help you understand which insurance policy suits you the best and which ones are best avoided.

- If your portfolio is skewed towards any particular asset class. Most people consider equity as the best investment option especially during a stock market rally.

However, it is never wise to put all eggs in the same basket.

It is vital for you to understand that not all assets move in the same direction at the same time.

If equities are witnessing a bear market, it is unlikely that other asset classes such as gold, debt instruments and real estate will also be witnessing a down-turn at the same time or vice-versa.

Hence it is best to invest in more than one type of instrument to improve your chances of achieving your long-term goals with minimal turbulence.

However, you must understand asset allocation need not be the same for all individuals. Asset Allocation is a subjective concept which differs on the basis of his / her risk appetite and risk tolerance.

Hence a suitable asset allocation for you can be devised through a financial plan which acts as a shield to protect your wealth during uncertain economic conditions and market volatility.

Chapter 3: Importance Of Financial Planning

Financial Planning is not meant only for someone who believes has lot of money or someone who has very little.

It is for anyone and everyone who is not in capacity to entirely mange one's finances. All of us have some or the other dream and aspirations. And to achieve these you need to plan your finances.

Hence, financial planning is important and crucial for everyone.

Watch this video to know the reasons why you would need financial planning:

Below are the two case studies on how a prudent financial plan can help you achieve dreams such as buying a house and building a retirement corpus.

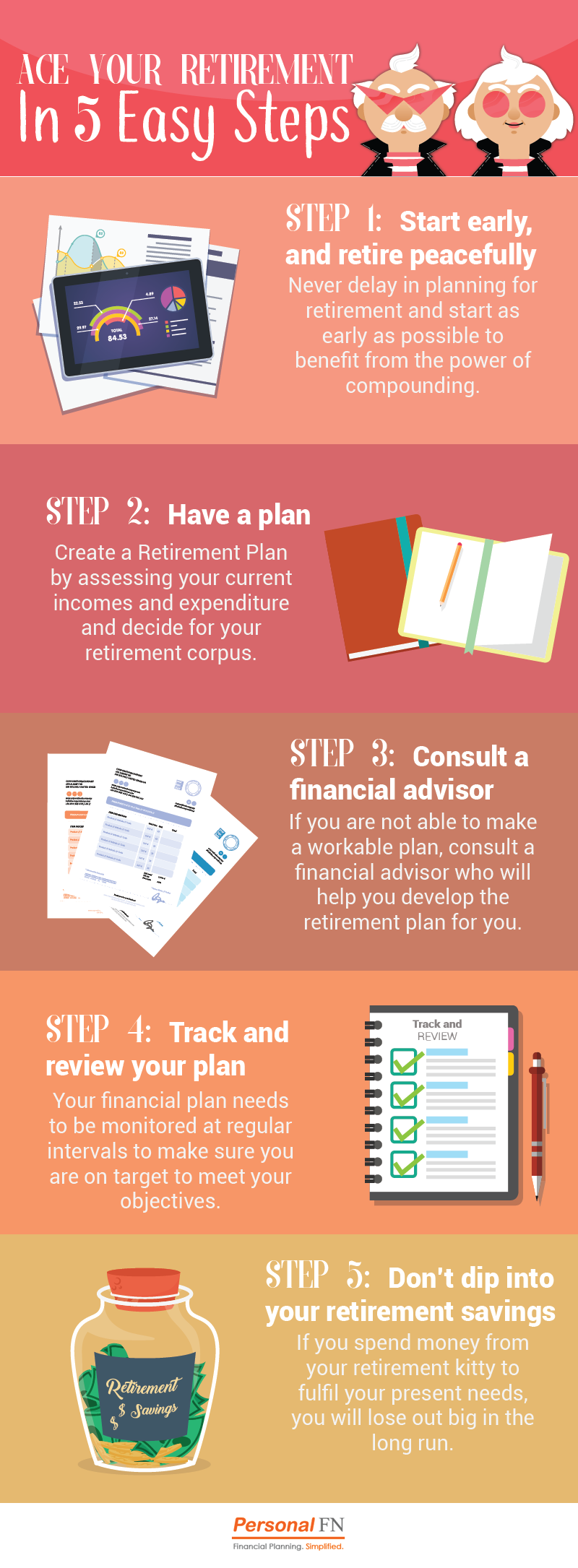

Financial Planning To Plan Your Retirement

When you are earning it's easier for you to manage your expenses through your monthly salary, but have you ever thought who will pay for your expenses once you stop earning. The answer to that is your savings and investment done in your earning period.

Investment done now will help you to live comfortably during your golden years i.e. retirement. So, it becomes inevitable for you to plan for your retirement in advance.

But we have often-heard excuse from people for delaying retirement planning such as "I have enough time to go before I retire, so why rush?" Unfortunately, most of you fail to realise that postponing is your biggest enemy when it comes to retirement.

Same was the case with one of our client who delayed planning for retirement till he turned 50. He later realized that he doesn't have much savings for his golden years.

Let's take his case to guide you how you can also plan for your golden years i.e. retirement.

Personal Details

Mr. Trivedi a 50 year old married individual wanted to retire at the age of 60 years. His spouse was the only member of his family dependent on him. He was earning Rs 87,000 per month, while his expenses were Rs 62,000 per month.

So, his monthly surplus was Rs 25,000 per month. Mr. Trivedi had a family history of living over 80 years so they were assumed to have life expectancy of 86 years.

| Personal Details |

| Name |

Mr. Trivedi |

| Age |

50 years |

| Retirement Age |

60 years |

| Dependents |

Only Spouse |

| Life Expectancy |

86 years |

| Income |

Rs 87,000 per month |

| Expenses |

Rs 62,000 per month |

Assets and Liabilities...

Mr. Trivedi had more than 70% of his total investment portfolio in illiquid assets such as Residential Flat and Land. Mr. Trivedi had taken a home loan (EMI = Rs 20,000) for the construction of residential flat in which he and his family was staying. 10% of his investment portfolio was invested in Equity via Equity Mutual Funds and Equity Shares.

He had opened a PPF account when he was 30 years old and extended it for 1 more block of 5 years, and now the PPF account will mature in next 2 months. He had also invested in Gold via Gold Mutual Funds. The Cash in Bank was mainly kept for contingency purpose.

| Assets |

| Sr. No. |

Type of Assets |

Amount (Rs) |

| 1 |

Equity Mutual Funds |

875,000 |

| 2 |

Equity Shares |

325,000 |

| 3 |

PPF |

1,000,000 |

| 4 |

Gold Mutual Funds |

700,000 |

| 5 |

Residential Flat (Self-Occupied) |

5,000,000 |

| 6 |

Land |

3,000,000 |

| 7 |

Cash in Bank |

270,000 |

| Total |

|

11,170,000 |

| Liabilities |

| Sr. No. |

Type of Liability |

Amount (Rs) |

| 1 |

Home Loan |

1,500,000 |

And here was Mr. Trivedi's Concern!

He was nearing retirement and he thought that his assets were not sufficient to fund all his expenses during his golden years i.e. post retirement period.

Retirement Corpus Required by Mr. Trivedi

Mr. Trivedi had current total expenses of Rs 62,000 per month and wanted to maintain the same lifestyle during post retirement period as well.

As he would have paid off his existing home loan by the time he retires, so his net total expenses required in current terms during the post retirement period is Rs 42,000 per month.

Assuming inflation of 7% and post retirement return of 8% he required a retirement corpus of Rs227lakh.

(Use our: Retirement Calculator to calculate your retirement corpus)

PersonalFN recommended him the following:

-

View on Land: His investment in land had grown for 5% per annum in last few years and not much growth was expected from the same going forward. Further land was giving him only price appreciation and no rental income. So, we advised him to sell land and invest the sale proceeds in constructed property which will give him some rental income and a higher expected growth rate in terms of capital appreciation to the property.

And he indeed put our advice to practice by investing in a new property and gave it on rent, which fetched him a rental income of Rs 4,000 per month and the property was expected to grow at 8% per annum.

This new property is estimated to command a value of Rs 64.76 lakh at his retirement.

-

View on Equity Mutual Funds: Most of the funds he had invested in were good diversified funds. We just consolidated his mutual fund portfolio as he had many duplicating schemes and they were not giving him any added advantage of diversification.

Equity Mutual Funds are expected to give him Rs 35.39 lakh at retirement assuming a 15% return on equity.

-

View on Equity Shares: He had invested in good stocks on the basis of researched based recommendations, so we advised him to continue holding it and use these stocks for retirement.

Equity Shares are expected to give him Rs 13.14 lakh at retirement assuming a 15% return on equity.

(Download our: Equity Guide for FREE to know how to build a stock portfolio)

-

Fresh Investment in Equity: We recommended him to start a SIP of Rs 19,000 per month in diversified equity mutual funds and increase it by 5% every year for 10 years.

He could increase his fresh investments by just 5% every year as his salary growth was not expected to be very high going forward.

Fresh investments in Equity are expected to give him Rs 62.79 lakh at retirement assuming a 15% return on equity.

-

PPF: PPF account which was about to mature was advised to be extended for 2 block of 5 years i.e. total of 10 years. He was also advised to invest Rs 7,000 per month before 5th day of every month till retirement. PPF account will give him Rs 34.27 lakh at retirement assuming 8% return on PPF.

(Download our PPF Guide for FREE to know all the details about PPF)

- View on Gold Mutual Funds: Gold mutual funds are good way of investing in gold so we advised him to hold it and invest further Rs 3,000 per month for 10 years. Gold Mutual Funds will give him Rs 19.29 lakh at retirement assuming a 7% return on Gold.

Accumulation until retirement

| Sr. No. |

Source of Investments |

Amount (Rs in lakhs) |

| 1 |

New Property |

64.76 |

| 2 |

Equity MFs |

35.39 |

| 3 |

Equity Shares |

13.14 |

| 4 |

Fresh Investments in Equity |

62.79 |

| 5 |

PPF |

34.27 |

| 6 |

Gold Mutual Funds |

19.29 |

| Total |

|

229.64 |

New property will have value of Rs. 64.76 lakh at the time of retirement which has contributed towards achieving Mr. Trivedi's retirement goal.

He doesn't need to sell this house at retirement but can continue getting rental income till the time he is about run out of his other investments and rental income is not sufficient to pay for his regular expenses.

Key learning's from this case study:

-

Start planning for retirement now! Even if you have just started earning, even a small contribution can make a huge difference.

-

Land is an illiquid investment and does not give any rental income; so invest only if you know the region in which it is located and is bound to deliver a high growth rate.

-

Post retirement expenses can increase significantly due to higher chances of falling ill; so make a provision for medical expenses while planning for retirement.

-

Due to medical advancement life expectancy has increased, so do not underestimate it.

Financial Planning To Make Your Dream Home A Reality

All of us have some or the other aspirations in life beginning from good education, a well-paid job, a successful career, a beautiful house to live in with best amenities, a car, travel abroad for leisure and a blissful retired life after having achieved all.

But amid all these aspirations, our experience shows that most individuals often put buying a dream home at priority, so that they can live in with their near and dear ones.

But very often, the way to own it prudently is not known to many.

You see, all of us do dream for a big house but rarely an action is taken to make it a reality. Remember, dreams do turn into a reality for those who really want to achieve it and strive hard for it.

We recognize that elevated property prices are making this aspiration of yours a distant dream, but prudent planning is the way to make your dream home a reality.

Let us explain you this with the help of a case study of one of our client who wanted to plan for his dream home but didn't know how to achieve it because of the limited surplus he had.

Personal Details

Mr. Ram a 40 year old married individual was staying with his wife and 2 kids in Mumbai.

Since most of his employment opportunities were available in Mumbai only, he wanted to settle down here for the rest of his life.

His salary income was Rs 1 lakh per month and he was also getting an annual bonus of Rs 2 lakh. Most of his monthly income was spent on his regular expenses which included a hefty Rental Expense of Rs 25,000 per month, and at the end of the month he was able to save just Rs 20,000 (Rs 1,00,000 Income - Rs 80,000 Expenses) for his future financial goals

| Personal Details |

| Name |

Ram (Name changed to protect privacy) |

| Age |

40 years |

| Marital Status |

Married |

| Kids |

2 Kids |

| City |

Mumbai |

| Income (post tax) |

|

| Salary |

Rs 1,00,000 per month |

| Bonus |

Rs 2,00,000 per annum |

| Expenses (per month) |

|

| Household |

Rs 20,000 |

| Lifestyle |

Rs 10,000 |

| Medical |

Rs 3,000 |

| Travel |

Rs 7,000 |

| Kids |

Rs 15,000 |

| Rent |

Rs 25,000 |

| Total |

Rs 80,000 |

He had the following assets as depicted in the table below.

Ram's Assets...

| Assets |

| Sr. No. |

Type of Assets |

Amount (Rs.) |

| 1 |

Equity Mutual Funds |

1,500,000 |

| 2 |

Equity Shares |

550,000 |

| 3 |

Debt Mutual Funds |

700,000 |

| 4 |

EPF |

650,000 |

| 5 |

PPF |

800,000 |

| 6 |

FD |

300,000 |

| 7 |

Car |

475,000 |

| 8 |

Residential Flat (Delhi) |

6,500,000 |

| 9 |

Physical Gold |

900,000 |

| 10 |

Cash in Bank |

450,000 |

| Total |

|

12,825,000 |

So, you can see that Mr. Ram had total assets worth Rs 1.28 crore, of which Residential Flat in Delhi comprises 50% of his total assets. His residential flat in Delhi was vacant and since it was inherited by him from his father he did not want to sell it.

He had some investments in Equity via Equity Mutual Funds and Equity Shares which he had accumulated over the years.

His investment in debt comprised of Debt Mutual Funds, EPF , PPF and FD. EPF was started when he started earning at the age of 25 years and PPF was started 10 years ago.

He also had a car which he used for commuting and some investment in physical gold, which were mostly gold ornaments of his wife. He was also maintaining some amount in cash for his contingency purpose.

He did not have any liabilities.

And here was Ram's Aspiration!

He wanted to buy his own flat in Mumbai worth Rs 1 crore but didn't knew how to fund it as he had surplus of just Rs 20,000 per month.

PersonalFN recommended him the following:

Self-funding vs. Home Loan: Buy a flat in Mumbai of the aforesaid value i.e. worth Rs 1 crore, with Rs 25 lakh self-funding and a home loan of Rs 75 lakh at 10% per annum rate of interest, with a loan tenure of 20 years; whereby the Equated Monthly Instalment (EMI) amounts to Rs 72,377

(Use our: EMI Calculator to calculate the EMI on your home loan)

A) The self-funding of Rs 25 lakhs was funded from following sources:

-

View on Equity Mutual Funds: Equity Mutual Funds worth Rs 5 lakh were asked to redeem as these were either non-performing funds or did not suit his risk appetite. Redemption proceeds to be utilized for funding the house purchase.

-

View on Equity Shares: You see, he had invested Rs 10 lakhs in Equity Shares on his friend's recommendation, but the current value of these was just Rs 5.50 lakh.

Since he did not have time to track these shares, PersonalFN recommended him to sell these, to fund his house purchase. We also recommended him not to invest in equity without any researched based recommendation.

-

View on Debt Mutual Funds: Long term income funds worth Rs 2.5 lakh were asked to redeem as these are interest rate sensitive funds and did not suit his risk appetite. Redemption proceeds to be utilized for funding the house purchase.

-

Withdrawal from EPF: He was working for last 15 years and had accumulated Rs 6,50,000 in EPF, so he was eligible to withdraw Rs 4 lakh from this account to buy a new house.

(Also Read: Can You Withdraw from Your EPF Account before Maturity?)

-

Withdrawal from PPF: He had opened a PPF account 10 years ago and was eligible to withdraw Rs 4 lakh from this account to buy a new house.

(Use our: PPF Calculator to calculate the maturity amount and withdrawal limit of PPF account)

-

Fixed Deposit: Existing fixed deposit worth Rs 3 lakh were asked to be utilized to buy a new house.

-

Bonus: He was eligible to get his annual bonus of at least Rs 2 lakh, in next 2 months; so he was asked to keep it to buy a new house.

| Self-funding (Rs) |

| Equity MF |

500,000 |

| Equity Shares |

550,000 |

| Debt MF |

250,000 |

| EPF |

400,000 |

| PPF |

300,000 |

| FD |

300,000 |

| Bonus |

200,000 |

| Total |

2,500,000 |

B) EMI of Rs 72,377 was funded from following sources:

-

Existing Rent: Buying a new house saved him Rs 25,000, which he was currently paying for a rented house. This amount was asked to be utilized for partially paying EMI on his new home loan.

-

Residential Flat (Delhi): Residential flat in Delhi was lying vacant, so we asked him to put it on rent. He did that, and it fetched him Rs 15,000 per month as rental income.

-

Second Source of Income: His wife had left job few years back but was ready to work in case of requirement. So, we asked her to start working for next few years till the time Mr. Ram salary was sufficient to fund EMI. This second source of income contributed Rs 22,377 per month.

-

Surplus: He had surplus of Rs 20,000 per month but all of it could not be utilized for payment of EMI as he had to invest for other financial goals as well. So, we advised him to divert Rs 10,000 from the surplus for the payment of EMI.

| EMI funding (Rs) |

| Rent |

25,000 |

| Rent from Residential Flat in Delhi |

15,000 |

| Wife |

22,377 |

| Surplus |

10,000 |

| Total |

72,377 |

So the dream home which looked impossible for Mr. Ram to achieve with a surplus of just Rs 20,000 became reality with prudently planning and some quality advice given to him.

Mr. Ram will struggle for few years as he will have very limited surplus, but the next few years will make sure that he has his own house in Mumbai. He also has an added benefit as EMI will not increase except in case of increase in interest rate on home loan; whereas his rent was growing at 10% every year.

Learning's from this case study and 5 Points to Remember:

-

If you buy your own house then you will save rental expense which will be available to fund your EMI.

-

Rental expense increases every year while EMI increase only in case of increase in interest rate which will always be less than increase in growth rate in expense.

-

If you have a vacant house, then consider giving it on rent for additional source of income.

-

If possible second source of income from spouse can help you fund for your goals.

-

Do not allocate your entire surplus for paying EMI as you have to plan for other financial goals as well.

You see achieving big dreams like buying a house and building retirement corpus is possible with the help of proper financial planning.

That's the magic of planning. And if you feel you cannot do it all by yourself, then do approach a professional financial planner. He/she would be in a better position to help you create an objective plan for you to achieve your dreams.

You may also like to read:

How Mr. Raghu restructured his liabilities?

How Mr & Mrs Raj planned for their Child Education & Marriage

Chapter 4: How To Select A Financial Planner?

Who is your financial planner?

Till now most investors used to focus purely on making investments into various instruments, like Mutual Funds, Insurance, Gold, etc. This was hardly ever backed by a thought on financial planning.

Now, however, a lot of them seek to create a financial plan which guides them on how much to save and helps them select the right investment instrument.

This is done after a detailed study of their existing investments, income, expenses and risk profile.

Today, almost everyone in the financial services industry claims to do financial planning.

In fact, major banks, brokers and distributors of financial products have opened departments or divisions which deal specifically with financial planning.

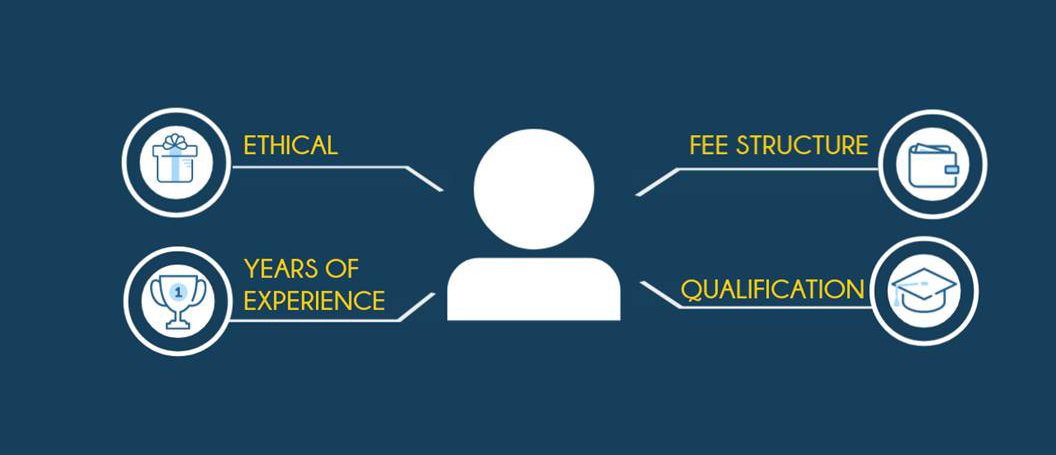

So, given the different type of players in the financial planning space a question which is bound to arise is - How should I select a financial planner? or how do I select a best financial planner?

The answer to this question is simple.

Check the capability of the individual or the organization that you wish to hire as your financial planner. Ask some few simple questions such as:

-

What is the business model of the company? How does it earn its revenues?

-

What is the process that they would follow in building the financial plan? Have a look at a sample plan.

-

What is the team size? Their experience and qualifications?

-

Are their recommendations based on solid research or driven by commissions?

-

How long has the individual or the organization been in business? How many clients have they made financial plans for?

-

Can they give references of existing clients with whom you can speak?

Do a detailed discussion with your prospective financial planner. Once you are satisfied on all these parameters, then go ahead and sign him up as your financial planner.

What all should a financial plan do for you?

A comprehensive financial plan should help you set the following things right:

-

Protection requirements and how to meet them

-

Emergency fund planning

-

Your goals (Retirement, asset purchase, children’s needs, etc) and the money that you would require to achieve them.

-

Detailed cash flows to help you understand the movement in your plan

-

View on your current investments

-

How should your investments be spread into various assets in line with your risk taking capacity

-

Investment Recommendations

What should be the cost of your plan?

There are various ways to pay for a financial plan (including in some cases where there is no charge).

Investors often tend to associate the cost that they are willing to pay for a plan with the amount that they are going to invest. That is not correct.

The price that you pay for getting your plan built is not just about the investment that you are going to make. You should look at the overall benefit that the exercise is going to bring to you in terms of how efficiently you would manage your personal finances with respect to all the points that have been mentioned above.

Word of caution:

Do not decide your financial planner purely based on who is going to charge you the least fees. Please understand there are no free lunches. And to build a financial plan which is comprehensive and considers all your requirements, a premium charge will have to be paid.

Also, while a CFP is a desirable qualification, the absence of it may not be the most appropriate reason to not select your planner. The approach and the expertise matter a lot.

Here are the 3 mistakes which you should clearly avoid while selecting your financial planner:

-

Not doing enough research:

What would you do if you were to get married? Will you marry the first lady/man who comes along? Or will you try to get to know him/her better?

The answer is a no brainer…

Of course, you would spend time with the individual to get to know him/her better. After all, it is your life’s happiness that is at stake and you wouldn’t like to tie the knot with an individual who doesn’t resonate with your views.

Right?

Now that’s exactly the kind of approach to follow while hiring a financial advisor!

It is weird that most individuals don’t have a set of questions to ask a financial advisor before associating with him/her. They prefer the “first come, first serve” approach when selecting a financial advisor.

But isn’t this approach completely absurd?

How can you just park your money with an individual you hardly know?

But then you may argue, “The financial advisor was referred by a close friend and my friend will always have my best interest in his mind”.

Maybe yes. But while a referral is the first step to building trust, it is important that you evaluate the advisor on your parameters before signing up with him/her. Questioning the advisor’s approach is a smart investor’s way of taking precaution and treading cautiously.

But then, how would you evaluate the financial advisor?

By asking him/her a series of questions, like a job interview that matter to you.

The second mistake to avoid is…

-

Not knowing how the financial advisor will be compensated?

Financial advisors in India follow any of the three revenue models:

-

Pure commission model — Here the financial advisor is compensated based on the commission he/she earns from the financial products that you invest.

-

Pure fee-based model — Here the financial advisor is compensated by the fees you pay for his advice and avail his/her services. He doesn’t earn any commissions on the financial products you invest.

-

Fee + Commission model— The financial advisor is compensated by the fees you pay for his advice and avail his/her service + the commissions he/she earns on the financial products you invest.

Now that you know the three models, have you ever wondered how most financial advisors in India are compensated?

The most common model in India is the Pure Commission model. Most investors unknowingly prefer to associate with an advisor who follows this model.

A naïve investor believes that since he/she isn’t paying any money from his/her pocket, there is no downside to associate with advisors practicing the pure commission model.

Do you really think that there is no downside? Think again…

It is in an advisor’s best interest that you purchase/ invest in financial products that earn him/her more commissions; at the cost of your financial goals.

These type of advisors (misrepresent themselves as ‘advisors’; in fact they are nothing but agents) mostly recommend traditional insurance products for all your financial goals. After all, insurance companies do offer some handsome commissions. This vested interest leads to mis-selling.

Now that you are aware, would you associate with an advisor who keeps his best interest ahead of yours?

No, isn’t it?

So, ideally, you should approach a financial advisor or a financial planner or a CFG practicing on pure fee-based model.

Since he charges professional fees (just as a doctor, chartered accountant, architect and lawyer etc.) for his/her services.

In most likely case he would put your interest at fore and handle your money with as much care as he would while managing his own money. Therefore, there are reduced chances of mis-selling.

Always consult a SEBI Registered Investment Advisor (RIA) who are subject to audit, legal compliances, and ethical code of conduct. If they are found in contravention of the provisions laid down by SEBI, they can even lose their licence to practice (just like any other professional). You can find a list of these RIAs here.

The third and the last mistake to avoid is…

-

Associating with a relative or a close friend as your financial advisor:

Yes, we recognise how controversial this statement sounds.

Like most individuals, you trust that a relative or a close friend would be the best person to act as a fiduciary.

After all, you know him/her since a long time and he/she wouldn’t take you for a ride.

But, that is exactly the problem while associating with a close friend or a relative!

You let your “smart investor” guard down and that is detrimental to a healthy professional relationship and your financial wellbeing.

When you work with a close friend or a relative, you tend to make decisions based on emotions rather than rationale. You trust blindly and don’t do the much needed due diligence before signing up with them.

Ask your childhood friend for his business history, experience and credentials etc. and he/she may take offence; fail to ask a full set of questions and you remain unsure you have the right expert.

There is more than money at stake when you do business with friends and family. If the decisions taken by the friend or the relative do not bear the kind of results you had hoped for, you will end up losing a close relationship too.

If you still want to go ahead with the relationship, make sure to factor in the extra value of your friendship into your decision making. Remember, you’ll lose a lot more than just money if a relationship with a friend or relative turns sour.

There is a lot more to traditional financial planning. Hence, choose a financial planner or a Certified Financial Guardian wisely.

The one who will not only chalk out a well-rounded personal financial plan, but patiently listen to what matters to you and handhold you to achieve your financial goals.

Chapter 5: Conclusion – Financial Planning

PersonalFN believes change is inevitable and procrastination is our enemy. Please recognise that, achieving financial nirvana isn't as tedious or nerve-wrecking as it is often made out to be. To get there, all one needs to do is:

- Construct a viable financial plan; and

- Be determined about achieving it.

And if you too want to plan your finances but don't know how to start with it, then do not hesitate to call us on 022-61361200.

You can also Schedule a Call with our investment consultant or even drop a mail at info@personalfn.com and we will get in touch with you. We would be happy to plan your finances prudently to help you achieve your life goals.

PersonalFN is a SEBI registered investment advisor. The fundamentals we firmly believe in are:

✔ Client first philosophy

✔ Confidentiality of your financial data

✔ Handhold you at every step in your financial freedom

✔ Provide unbiased recommendation backed by over a decade long research experience

✔ Disclose any kind of income we earn from recommendations

✔ Aim to establish a long-term relationship with you, not just a financial one

To achieve financial independence, there's no need to fight or struggle for it. All it requires is to have the right knowledge and patience.

Approach a financial planner and your money will be in safe hands.

Happy Planning!

Author: PersonalFN Content & Research Team