All You Need To Know About Robo-Investing

As a kid I always wished if my Robo - Shiro (toy) could carry my heavy school bag, do my home-work (especially the Art work).

And for very long time I wished for some wise, trustworthy and experienced personnel to help me in planning my finances.

Well, my wishes remained unfulfilled as a kid, but not anymore.

With the advent of technology and automated investing facilities available, I no longer worry about my money matters.

Wondering how?

Let me tell you, there are many Robo Advisors available in the market.

Read on this guide on robo investing to come out of fears as we will clarify all your doubts about it today:

Chapter 1:What Is Robo Investing All About?

Robo advisor is nothing but a financial adviser who provides automated investment solutions online. So, you no longer must appoint a financial planner in person to draw your investment plan.

To make it easier for you, robo advisory platforms are digital advisors who provides portfolio management and financial planning services online, without little or no human intervention.

Do you remember how internet banking was once dreaded? But now it is the most hassle free and favoured ways of banking.

You might have the same feeling for robo investing as well.

Wikipedia defines robo advisors as "a self-guided online wealth management service that provides automated investment advice at low costs and low account minimums, employing portfolio management algorithms."

Further it states that:

“They provide digital financial advice based on mathematical rules or algorithms. These algorithms are executed by software and thus financial advice do not require a human advisor.”

Simply put robo advisors are digital advisors available for you 24*7. They follow a set structure and are not influenced by any emotions.

To know the benefits of robo investing read the next chapter:

Chapter 2:Are There Any Benefits Of Investing Online?

There are many benefits of investing via a robo advisory platform. Some are highlighted below:

Devoid Of Behavioural Biases

It is quite possible that a human advisor would be biased in his/her recommendations.

Robo advisors on the other hand, act pragmatically and help you create a financial plan to achieve your goals.

Convenient and Time-saving

Robo-advisors offer a user-friendly interface and provide a world of convenience.

There is no need to set up an appointment with a financial planner each time you need to review your goals.

All you need is to share the correct information to get customised advice.

Additionally, you can track your investments over single platform. Which you can even access it at any time.

You can manage your mutual fund investments from the comfort of your home or even on the go through a mobile application.

Everything from KYC to redemption of mutual fund units is possible online.

Reach & Speed

Robo-advisors are likely to deliver plans, faster as they are based on mathematical algorithms.

If you have a high-speed internet connection and mid-range computer/laptop, you are halfway there.

Everything is possible just by one click.

Cost Efficient

When planning your finances or investments, you may tend to ignore costs. Especially, when costs are mentioned in percentage terms, it may seem small and insignificant.

However, it might cost you a big amount if you compound the benefit over the long-term.

Thanks to technology, robo-advisors can lower their costs. They are relatively cheaper than traditional financial planners.

Now that you know the benefits of online investing, let us look at how robo advisors are better than traditional planners in the next chapter.

Chapter 3: Robo Advisors vs Human Advisors

Surely, you must be wondering if you have a financial advisor why should you choose a robo. But read on and you will have an answer to this question.

Remember the good old days where you would receive a message over a pager? There was a time lag, high cost involved in this kind of communication.

Similarly, the basic difference between a robo and human advisor is their quick response, fee structure along with other points. Read on to know better:

Advisory Fees

If you are an investor who wants to save on cost of investing, then you must invest via a robo advisor.

For years, many have been saving and investing by following the advice of a friend or relative. Someone who they believe have sound financial knowledge. All that was just to save a financial planners fee.

Robo-advisors can lower costs, and therefore work out to be relatively cheaper than traditional financial planners.

As you would know financial planners usually charge hefty fees and deliver little results.

As mentioned before, robo advisors can save huge amount of costs due to little or no human intervention.

An ethical robo-advisor will be cost effective and offer you mutual fund direct plans as an investment option. Over time, this will help you conserve an immense amount of money.

Recommendations/ Advice

Human financial advisors are human first and investment advisers later.

A variety of events and developments affect them.

For example, if your advisor is risk averse, he/she will always discourage you from taking the risk, irrespective of your risk appetite.

Similarly, his/her response to your queries may differ depending on market conditions, business targets they may be working towards and your rapport with him/her.

Investment advisers may also give biased advice eyeing the high commissions.

Unlike this, robo-advisors offer you consistent and instant advice.

They might not look at the market indices and advise you on your investments. Similarly, they won't be driven by any sales targets. Hence, they won't alter their responses with some hidden motives.

Indiscriminately Provide Service

Robo advisors do not provide service according to the investor's net worth.

Investors with nominal capital often feel dejected.

It has been observed in the past that very few advisors are keen to offer their services to investors with small asset base.

And acquiring High-Net-worth Individual (HNI) clients is their primary objective.

Robos, on the other hand do not discriminate investors on their asset size. Many robo platforms let you even start a SIP of Rs 500.

Omnipresence

With robo advisors you receive investment advice instantly and consistently. Because they are omnipresent- present everywhere at same time.

Human advisors on the other hand might be available only during their working hours. Like you and me they too go for holidays and have their own calendar.

Hence your investment transactions are dependent on their availability.

Better Record Keeping

At present, not all human-advisors offer a digital record keeping option to their clients. They follow maybe spreadsheet or diary to keep a record.

But these are not secure ways of record keeping.

As a result, many a time, they as well as their clients lose the track of their own investments.

Robo-advisors make a significant difference here.

They help you retrieve even the minutest detail of your investments on your dashboard. Once you have created your investment plan, your robo-advisor will keep it on track.

Suitable For All

Robo advisory platforms can be used by investors as well as financial advisors.

As far as the investment advisories are concerned, they can use robo-advisory platforms as an additional tool that helps blend their offerings.

They can automate the simpler processes and retain the human-advisory model for more personalised and sophisticated advice. This helps them add more value to their services and may lead to greater client satisfaction.

Surely, robo advisory platforms are likely to change the dynamics of the financial services industry in future.

Does this mean investor is to trust machines more than humans?

Not quite. Let's not forget, behind any technology, there's always a human brain at work.

Undoubtedly, robo-investing is a significant development that's likely to work positively for investors.

Chapter 4: How Do I Choose Best Robo Advisor?

Now that you understand the meaning of a robo-advisor, and the flood of information has perhaps left you unsettled. If you've decided to take the plunge into the sea of financial automation, but don't know where to start?

We have outlined 4 steps to zero-in on the right robo-advisor.

Step 1: Identify your need

Financial planning services can vary from simple goal-based planning, to a more comprehensive service of managing your debt and cash flows. Most robo-advisors today are only equipped to handle the former.

So, before you get your expectations too high, remember that a robo-advisor may only be able to automate your investments towards new financial goals.

Therefore, if you have not started actively saving and investing towards any financial goals or if you are planning to add new investment goals, then robo-advisors are for you.

Here again, robo-advisory platforms come with different options – some may offer complete automation, while others may offer hybrid services that pair the computer algorithms with financial planners. You need to choose wisely.

If you are looking for simple goal-based planning, the former may help.

But, as your investment portfolio and financial needs grow, you may someday require the services of a human advisor.

Hence, it would be prudent to select a robo-advisor that offers advanced financial planning (with human interaction) as an add-on service.

Step 2: Take the free trial or free membership

Most robo-advisors allow you to create a free account to explore their services. Some offer the entire platform free, as they earn from commissions.

So, before you commit your money, either by subscribing to the service or making an investment, you can first take a test run of the platform.

Doing this, will ensure you get a feel of their platform – whether the user interface is friendly and easy to understand, and if it is free from technical glitches.

Though glitches may arise once you start transacting, it will be better if you confirm that the platform moves smoothly before any monetary commitment.

Step 3: Rate the robo-advisor on 4 important criteria

Once you have tried and tested the robo-advisors, it's time you evaluate them. PersonalFN has outlined four important criteria…

-

Service offerings

As mentioned earlier, some robo-platforms may offer you only transactional services, while others may provide you with a host of offline and online personal finance offerings.

In addition, some robo-advisors may offer advanced tracking and portfolio rebalancing services. Those that offer a mix of services should be worthy of your long-term financial commitment.

Also, the platform should be backed by a team of experienced customer service associates.

If you have any query related to the investments you make or if you are facing issues when transacting, your problem should be resolved quickly and professionally.

-

Unbiased and research-backed advice

A robo-advisor backed by strong research processes will help you select the right mutual fund schemes. Remember, fund performance should not be the only criteria.

There needs to be different qualitative and quantitative parameters that need to be considered before arriving at the top schemes suitable for your portfolio.

Robo-advisors that prudently pick the best schemes for your portfolio should rank high amongst those shortlisted.

-

Established and reputed company

There is no dearth of robo-advisory platforms as the barrier to entry is low. While the competition is immense, you need to choose wisely, entrust your money to best advisor!

With the immense competition, smaller robo-advisory firms may find business unviable, could shut shop, and leave you in the lurch. Therefore, opt for robo-advisors backed by established companies in the financial services space.

Sound and ethical research processes fully support their investment recommendations. They should be fee-based to ensure that the commissions they earn do not influence their advice.

-

Costs

Costs play a crucial role when you are planning your investments. Different robo-advisors may charge you through one of the methods below:

- An advisory or subscription fee (monthly, quarterly or yearly)

- A transaction fee (each time you execute a transaction through them, they charge you a fee)

- A percentage of the amount invested. (Popular in the US)

- A percentage of the amount invested. (Popular in the US)

- Commissions earned from fund houses of recommended funds

While the first three forms are upfront one-time costs, watch out for the last option, as the advice here may be biased.

You can always decide whether the subscription fee or transaction fee is worth your money depending on the quality of advice and services offered.

Also, if you have a high quantum of assets, you can avoid investing with robo-advisors that charge you a percentage of your investment value.

The costs may end up higher than the one-time fees you would pay otherwise.

Step 4: Make a decision and stick with it

As you have followed a stringent 3-step process to narrow down the list, you may feel there's little that can go wrong.

But let me tell you, selecting the right platform is just the first step to your financial independence.

Many a times, individuals avail of the services of a financial planner or investment advisor but are unable to stick with the plan through the entire investment horizon.

This can adversely affect their financial well-being.

So, remember, once you begin, make sure you stay on until the end. If there are genuine issues with the robo-advisor that warrants an exit, make sure you continue with another. This will ensure that your financial goals are not impacted.

If you have not yet zeroed in on a suitable robo-advisor, we suggest you wait, because the best robo-advisor is just around the corner.

Chapter 5: Wondering If You Should Opt For A Robo Advisor? Yes/No. Find Out…

Wondering, whether you should opt for a robo-advisory platform to invest in mutual funds, then read on this chapter and get an answer for yourself.

If you as an investor are looking for the below features in your ideal advisor then you must opt for a robo advisor:

Want To Save On Costs

If you are an investor who wants to save on cost of investing, then you must invest via a robo advisor.

As you read above robo advisors can cut down overhead expenses for you to a great scale.

Willing To Take Informed Decisions

Many a times, individuals avoid investing because of a lack of knowledge. They do not know how to start investing and hence, procrastinate.

But if you are an investor who wishes to make an informed decision, then start investing via robo-advisory platforms.

Everything is possible just by one click.

Wish To Avoid Behavioural Biases

To reiterate, robo-advisors are devoid of all the behavioural biases.

Looking For Convenience and Easy Investing

If you are looking for convenience in investing, then robo-advisors make that possible for you as well. Robo-advisors offer a user-friendly interface and a world of convenience.

You can manage your mutual fund investments from the comfort of your home or even on-the-go through a mobile application.

Wish To Have Quick Investment Procedures

If you have been procrastinating to save and invest, assuming that it is a time-consuming activity, then you must invest via a robo platform.

Robo-advisors are algorithm-based platforms; they are likely to deliver plans, solutions faster.

Alternatively, investing with a traditional advisor requires you to meet the advisors several times, before coming to a final plan.

Can Do It Yourself

Now, if you do not like being dependent on anyone, then robo-advisors are best suited for investors like you.

With some basic and self-knowledge, you can execute your investment plan yourself. You can initiate the end-to-end process of investing yourself.

Just like you purchase goods from an e-commerce platform, you can invest in mutual funds too with these robo platforms.

Chapter 6: Should I Select A Direct or Regular Mutual Fund Plan?

Robo-advisors are able to attract clients with their attractive low costs. Some even claim it to be a free service or virtually free.

But is it free?

Let’s face it… there are no free lunches in life. Businesses are established to earn money and generate profits. Look deeper before zeroing in on the best robo-advisory platform that may seem economical for you.

Maybe the advisory is pocketing huge commissions from the funds they recommend. And you may be surprised to know that the same is being deducted from the value of funds in your portfolio, in the form of high expense ratio. Yes, the regular plans recommended by most of the robo-advisors come with high expense ratio, due to which you might be losing a significant amount of money every year.

If your robo-advisor does not offer you direct plans, over the years, you will be losing out on generating significant wealth for yourself. How? Read ahead.

Direct plans of mutual fund schemes charge a lower daily fee (better known as expense ratio) as they eliminate distribution costs and commission paid to the distributor.

These plans are thereby able to generate a higher return over the long-term and save investors a huge amount of cost.

Both the plans have the same underlying portfolio, fund manager, and follow the same investment strategy, but different expense ratio and NAVs.

While ‘regular plan’ charges you a high expense ratio, a lower expense ratio for a ‘direct plan’, enables you to clock better returns than the regular plan.

Why should you prefer direct plans?

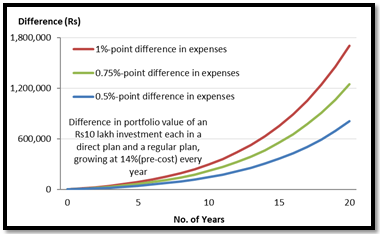

Mutual fund direct plans make a positive difference to your investments every year.

These plans generate roughly 0.5% to 1.0% additional returns every year, thanks to lower costs.

It may not seem much at first, but, if you sow seeds of these small savings, you may harvest rich rewards over 15- 20 years — thanks to the power of compounding.

(Source: PersonalFN Research)

As can be seen in the chart above, a small difference in costs can result in savings of anywhere between Rs8-17 lakh over 20 years, on a Rs10 lakh investment.

Yes, you can earn an additional amount of as much as Rs17 lakh, if the difference in costs is as much as 1% point.

The final portfolio value varies with the magnitude difference in expenses.

Every 0.25%-point difference in the expense ratio works out to an additional earning of Rs 4.50 lakh in 20 years’ time, for Rs 10 lakh of initial investment.

Hence, always choose a direct over regular plan while investing in mutual funds.

Chapter 7: What is PersonalFN Direct?

PersonalFN is happy to announce that we will soon launch our robo advisory platform – PersonalFN Direct.

PersonalFN Direct will be devoid of commissions. Our recommendations will be powered by our in-depth research process, and we will encourage (offer) only ‘Direct Plans’.

We have always believed in goal based financial planning and our platform is getting ready to provide you the same.

Further, we will perform an in-depth risk profiling for each client so that they can make an informed decision about their finances.

As you would know we at PersonalFN always follow high fiduciary standards.

We our investor’s, interest at fore. That’s been our DNA and shall always stay with us.

We stand for credibility, integrity, and transparency —we will never compromise on that. Never! Likewise, we respect the privacy of our clients.

Chapter 08: Conclusion – Robo Investing

Robo-advisors certainly may be a compelling alternative to many sources of traditional advice. And in many cases may be a step ahead of such sources of advice due to their lower costs, well-grounded investment methodology, and alignment with you financial interests.

At the same time, you need to acknowledge that not all robo-advisors are perfect.

Their advice may not be fully customisable. Hence, the robo-advisory service you choose needs to be well equipped to care for your investments and financial goals.

If you have not yet zeroed in on a suitable robo-advisor, we suggest you wait, because the best robo-advisor is just around the corner.

Author: PersonalFN Content & Research Team